Executive Summary

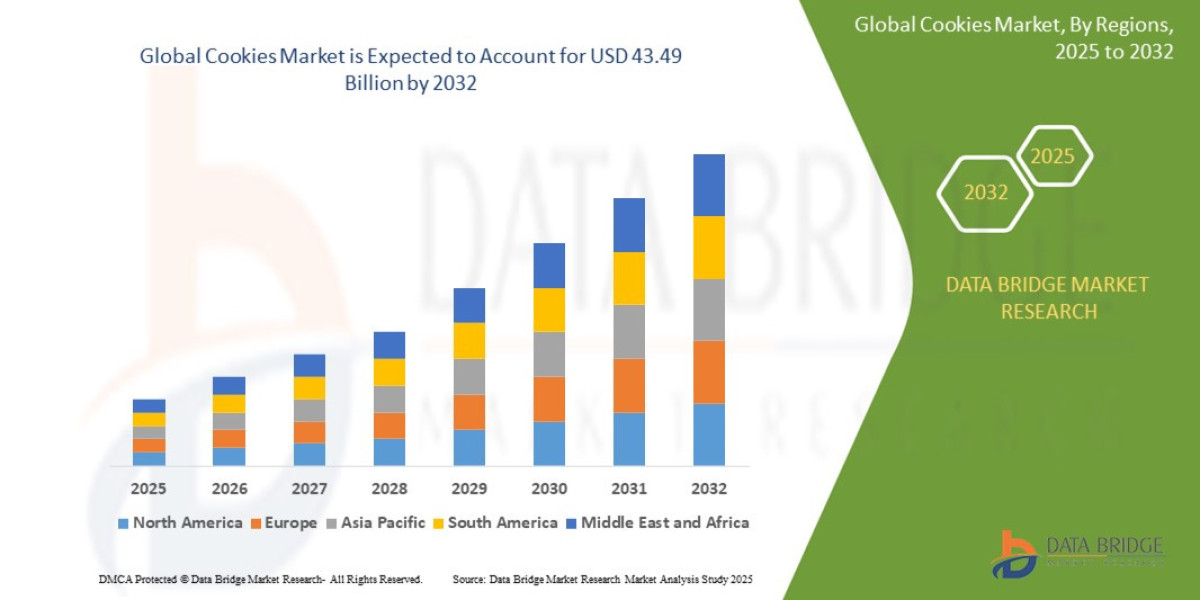

- The global cookies market size was valued at USD 26.90 billion in 2024 and is expected to reach USD 43.49 billion by 2032, at a CAGR of 6.19% during the forecast period

Market Overview

The Cookies Market encompasses all commercially produced baked goods, including packaged, unpackaged (freshly baked), and frozen dough formats. As a staple snack, cookies span the spectrum from affordable, mass-produced varieties to high-end, artisanal offerings.

Key Segments

By Product Type:

Packaged Cookies (The Largest Segment): Dominated by mass-market brands, including sandwich cookies (creams), chocolate chip, shortbread, and wafers. This segment benefits heavily from grocery and convenience store distribution networks.

Freshly Baked/Artisanal: Includes cookies sold in in-store bakeries, specialized cookie shops, and cafes. This segment commands a higher price point and is driven by experiential retail and perceived freshness.

Cookie Dough: A high-growth segment, benefiting from the trend toward home baking and convenience.

By Ingredient/Claim:

Conventional: Cookies using standard wheat, sugar, and dairy.

Health & Wellness/Functional: Includes gluten-free, sugar-free, high-protein, high-fiber, and plant-based/vegan cookies. This is the fastest-growing sub-segment.

By Distribution Channel:

Supermarkets/Hypermarkets: Dominant channel for packaged cookies.

Convenience Stores: Critical for impulse purchasing.

Online Retail (E-commerce): Fastest-growing channel, enabling D2C (Direct-to-Consumer) specialty brands to reach niche consumer groups (e.g., keto, specialized allergens).

Drivers and Current Dynamics

Convenience and On-the-Go Snacking: Modern lifestyles drive demand for ready-to-eat, portion-controlled snacks. Cookies are intrinsically linked to convenience and immediate indulgence.

Product Proliferation and Innovation: Continuous introduction of new flavors (e.g., global cuisines, spicy variants), textures, and functional ingredients keeps consumer interest high and encourages repeat purchases.

Rise of Health-Conscious Indulgence: Consumers still seek treats but demand reduced guilt. This fuels the dynamic of "better-for-you" cookies that substitute ingredients (e.g., non-nutritive sweeteners, almond flour) while maintaining taste.

E-commerce and D2C Growth: Digital platforms allow artisanal and niche producers to bypass the high entry costs of traditional retail, leading to greater market fragmentation and diversity in specialized offerings (e.g., keto, personalized allergy-friendly boxes).

Market Size & Forecast

- The global cookies market size was valued at USD 26.90 billion in 2024 and is expected to reach USD 43.49 billion by 2032, at a CAGR of 6.19% during the forecast period

For More Information Visit https://www.databridgemarketresearch.com/reports/global-cookies-market

Key Trends & Innovations

The modern cookies market is defined by a dichotomy: the pursuit of extreme indulgence versus the demand for dietary precision and functional benefits.

The "Permissible Indulgence" Trend: This is the most defining trend. Manufacturers are formulating cookies that satisfy the craving for sweets but mitigate perceived negative effects through attributes like "low-sugar," "high-protein," or "gluten-free." This allows consumers to justify the purchase as a balanced snack rather than pure dessert.

Plant-Based and Vegan Cookies: Driven by ethical consumption and environmental concerns, the demand for entirely plant-based cookies has surged, moving beyond simple dairy replacement to incorporate complex textures using ingredients like chickpea flour, potato protein, and specialized vegan fats.

Global Flavor Fusion: Beyond the classic chocolate chip, brands are experimenting with flavor profiles borrowed from global dessert traditions (e.g., Miso caramel, matcha, turmeric, spicy chili variants) to appeal to adventurous, diverse consumer palates.

Focus on Fiber and Gut Health: Cookies are increasingly positioned as carriers for gut-friendly ingredients, utilizing high-fiber flours (oat, barley) and inulin to appeal to the functional food space.

Automated Baking and AI Quality Control: In large manufacturing facilities, AI and machine learning are being deployed to monitor dough consistency, oven temperature, and product color in real-time, ensuring zero-defect rates and maintaining the exact "perfect" chewiness or crunch that consumers expect.

Competitive Landscape

The Cookies Market features a dual competitive structure: a highly consolidated mass-market segment and a highly fragmented, innovative specialty segment.

Major Players:

Mondelez International (Oreo, Chips Ahoy!): The undisputed global leader, controlling vast shelf space and benefiting from iconic, globally recognized brands. Strategy focuses on flavor extensions, limited editions, and aggressive emerging market expansion.

PepsiCo (Quaker Oats, Frito-Lay snacks): A major player, particularly with brands that bridge health and indulgence, leveraging massive distribution capabilities across retail channels.

Kellogg’s, Nestleˊ, General Mills: Large FMCG conglomerates that compete through strategic brand presence and continuous innovation across their portfolios.

Competitive Strategies:

Acquisition of Niche Brands: Large conglomerates actively acquire smaller, successful specialty brands (e.g., gluten-free, high-protein) to quickly gain market share in the high-growth functional segment without lengthy R&D cycles.

Ingredient Transparency and Clean Labeling: A major competitive battleground, with brands increasingly competing on the length and simplicity of their ingredient lists. Using non-GMO certifications and clearly communicating the source of ingredients is now mandatory for premium appeal.

Channel Optimization: Leveraging D2C sales for new product testing and personalized offerings, while simultaneously relying on mass retail for volume and promotional sales.

Personalization through Formulation: Catering to highly specific dietary needs (e.g., certified Paleo, specific nut-free claims) to capture high-value, niche consumer loyalty often inaccessible to mass-market brands.

Regional Insights

Market maturity and growth vary significantly across key geographical regions.

North America: A mature and dominant market, characterized by high per capita consumption and an accelerated shift toward functional and free-from cookies. The US leads in ingredient innovation (keto, protein, low-sugar), driven by consumer health trends and extensive product labeling.

Europe: A value-driven market with strong demand for artisanal and sustainable products. Clean-label ingredients, reduced sugar, and ethical sourcing are paramount, driven by stringent EU food safety and environmental regulations. The UK and Germany lead in plant-based adoption.

Asia-Pacific (APAC): The fastest-growing region globally. Growth is powered by rising disposable incomes in India, China, and Southeast Asia, leading to the adoption of westernized packaged snacks. Market potential is immense, though it requires adaptation to local palates (e.g., less sweet formulations) and localized distribution challenges.

Latin America (LATAM): A high-growth region driven by population growth and urbanization. The demand focuses primarily on value and volume, though a premium segment is rapidly emerging in major cities, fueled by foreign FMCG investments.

Challenges & Risks

While stable, the Cookies Market faces significant headwinds that challenge profitability and product development.

Rising Commodity Prices: Volatility in the global pricing of key inputs—sugar, wheat flour, dairy, and cocoa—puts constant pressure on manufacturing margins, especially for mass-market products where pricing elasticity is low.

Regulatory Scrutiny on Sugar Content: Governments worldwide (particularly in Europe and North America) are implementing or considering sugar taxes and strict advertising regulations for products marketed to children, forcing costly recipe reformulations.

Supply Chain Complexity for Niche Ingredients: The shift to specialty ingredients (e.g., coconut flour, Monk fruit sweetener, specialized proteins) introduces complexity, higher sourcing costs, and risk of supply shortages compared to sourcing mass commodities.

Packaging Sustainability Mandates: Consumer and regulatory demands for eliminating single-use plastic and non-recyclable materials require heavy R&D investment in new, food-safe, and shelf-stable packaging formats.

Opportunities & Strategic Recommendations

The future success of the Cookies Market lies in harmonizing the universal desire for indulgence with the modern consumer's demand for health, ethics, and transparency.

For Manufacturers and FMCG Conglomerates:

Accelerate Ingredient Substitution: Aggressively fund R&D into alternative sweeteners (allulose, stevia blends) and fiber-rich flours to stay ahead of regulatory changes while preserving taste and texture. Sugar reduction is the single most critical investment area.

Target Functional Snacking: Develop clear product lines focused on functional benefits (e.g., energy, gut health, recovery) that allow for premium pricing and attract a loyal, health-focused consumer base, particularly in the North American and European markets.

Optimize Nearshoring for Freshness: For artisanal or premium lines, explore nearshoring or localized production models to emphasize freshness, quality perception, and reduce logistics carbon footprint.

For Startups and Innovators:

Solve the Allergen Gap: Focus on highly niche, underserved allergen markets (e.g., dedicated sesame-free, chickpea-free) that demand high trust, leveraging D2C channels for distribution.

Create Sustainable Packaging Solutions: Develop innovative, cost-effective packaging that maintains the necessary shelf life and food safety standards while achieving certified home compostability or high recyclability rates.

For Investors:

Acquire D2C Clean Label Brands: Target successful niche brands with proven product-market fit in the keto, vegan, or gluten-free space. These acquisitions offer high growth rates and access to valuable consumer data.

Invest in Ingredient Tech: Fund companies developing high-performance, cost-effective substitutes for core commodities like cocoa (sustainable alternatives) and sugar.

Browse More Reports:

North America Data Integration Market

Middle East and Africa Small Molecule Sterile Injectable Drugs Market

Global Rail Fasteners Market

Global Monoterpenes Market

Global Point of Care Infectious Disease Market

Global Canned Berries Market

Global Immunomodulators Market

Global Cancer Gene Therapy Market

Global Solar Thermal Collector Market

Global Freeze-Dried Fruits Market

Global Network Security Software Market

Asia-Pacific Mass Notification Systems Market

Europe Dental Practice Management Software Market

Global Fractional Flow Reserve Market

Global Angiographic Catheter Market

Europe Heavy Metals Testing Market

North America Hand Holes Market

North America Indium Market

Global Skin Packaging Market

Global 3D Cell Culture Market

Global Micro Battery Market

Global Chitosan Market

Global Form-Fill-Seal (FFS) Films Market

Europe Surgical Power Tools Market

Middle East and Africa Flight Data Recorder Market

Global Transthyretin Amyloidosis Treatment Market

Global Flexographic Inks Market

Asia-Pacific Composite Bearings Market

Europe Feed Flavors and Sweeteners Market

Global Interventional Oncology Devices Market

Middle East and Africa Methylene Diphenyl Diisocyanate (MDI) Toluene Diisocyanate (TDI) and Polyurethane MarketNorth America Clinical Microscopes Market

About Data Bridge Market Research:

An absolute way to forecast what the future holds is to comprehend the trend today!

Data Bridge Market Research set forth itself as an unconventional and neoteric market research and consulting firm with an unparalleled level of resilience and integrated approaches. We are determined to unearth the best market opportunities and foster efficient information for your business to thrive in the market. Data Bridge endeavors to provide appropriate solutions to the complex business challenges and initiates an effortless decision-making process. Data Bridge is an aftermath of sheer wisdom and experience which was formulated and framed in the year 2015 in Pune.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email:- corporatesales@databridgemarketresearch.com