Executive Summary

The global payment gateway market is experiencing an unprecedented surge, driven by the structural shifts in global commerce toward digital platforms, the proliferation of mobile connectivity, and the integration of financial services directly into business software. Payment gateways—the critical technological infrastructure enabling secure online transaction authorization—are transitioning from simple utility providers to strategic facilitators of digital business transformation.

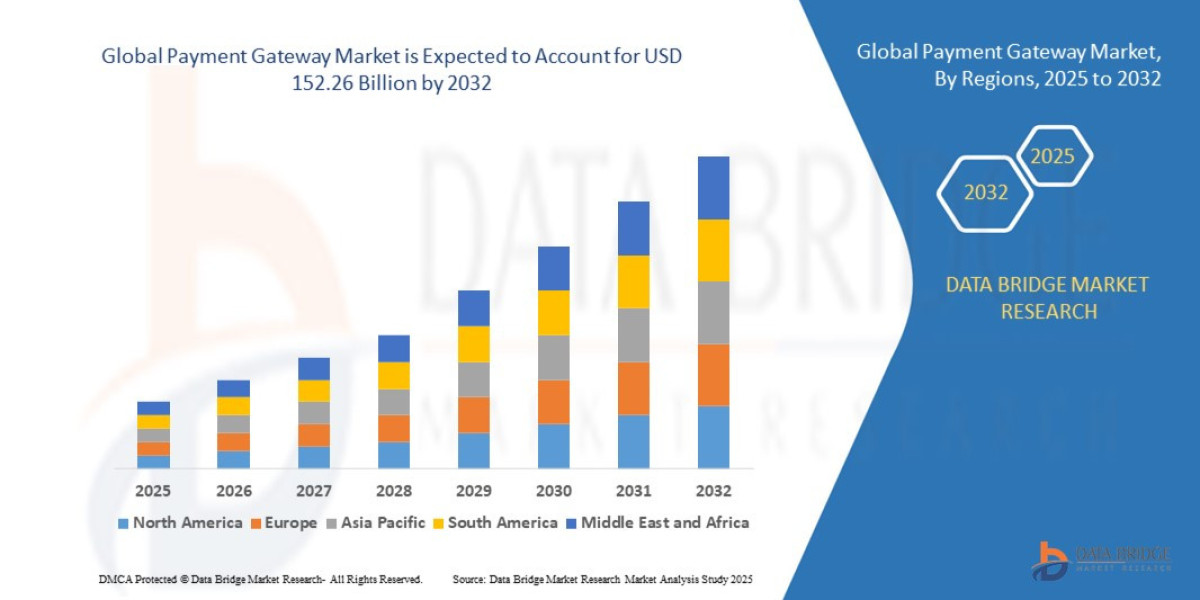

- The global payment gateway market size was valued at USD 35.17 billion in 2024 and is expected to reach USD 152.26 billion by 2032, at a CAGR of 20.10% during the forecast period

Market Overview

Defining the Payment Gateway Market

A payment gateway is a merchant service provided by an e-commerce application service provider that authorizes card-not-present (CNP) payments for e-businesses, online retailers, and brick-and-mortar stores. It serves as the secure conduit between a merchant's website and the acquiring bank or payment processor. The market scope encompasses the full spectrum of solutions that facilitate the encryption, transmission, and settlement of digital transactions.

Key Segmentation and Drivers

The market is commonly segmented by type, enterprise size, and end-use vertical:

By Type:

Hosted Gateways: (Currently dominant, >57% share) Redirects customers to the gateway's page for payment. Popular among smaller merchants due to ease of setup and reduced Payment Card Industry Data Security Standard (PCI DSS) compliance liability.

Non-Hosted (API-Based) Gateways: Provides full customization, embedding the payment form directly into the merchant’s checkout page via Application Programming Interfaces (APIs). This segment is experiencing the fastest growth as large enterprises prioritize seamless user experience and data control.

Local Bank Integration Gateways: Solutions tailored for specific domestic banking systems.

By Enterprise Size: Dominated by Large Enterprises (>56% share), which require sophisticated, cross-border, and multi-currency processing capabilities. However, the Small and Medium-sized Enterprises (SMEs) segment is growing rapidly, driven by integrated solutions from platforms like Shopify and Square.

By End-Use: Retail and E-commerce remains the leading vertical, accounting for over 26% of the market revenue, followed by Banking, Financial Services, and Insurance (BFSI), Travel & Hospitality, and Media & Entertainment (subscription models).

Core Market Dynamics

The current market is characterized by three fundamental dynamics:

E-commerce Acceleration: Sustained growth in global online retail sales, reinforced by post-pandemic consumer behavior shifts, necessitates robust and high-capacity gateway services.

The Mobile-First Mandate: The majority of global digital commerce originates from mobile devices, increasing demand for highly optimized, single-click, and biometric-enabled payment flows.

Regulatory Scrutiny: Evolving global data sovereignty laws (like GDPR in Europe and data localization rules in India) require gateways to maintain complex, geo-specific compliance frameworks, elevating the barrier to entry for smaller players.

Market Size & Forecast

- The global payment gateway market size was valued at USD 35.17 billion in 2024 and is expected to reach USD 152.26 billion by 2032, at a CAGR of 20.10% during the forecast period

For More Information Visit https://www.databridgemarketresearch.com/reports/global-payment-gateway-market

Key Trends & Innovations

The current transformation of the payment gateway market is defined by several technological and behavioral innovations, moving the ecosystem toward instantaneity, intelligence, and integration.

1. The Global Expansion of Real-Time Payments (RTP)

RTP systems are rapidly becoming the global standard. Initiatives such as the U.S.'s FedNow, Europe's SEPA Instant Payments, and India’s Unified Payments Interface (UPI) are transforming liquidity management and settlement times. Payment gateways are adapting their platforms to become "multi-rail" orchestrators, connecting merchants not only to card networks but also directly to these instant account-to-account (A2A) payment rails. By 2027, RTPs are projected to constitute nearly 27.8% of all global electronic payments.

2. AI/ML in Intelligent Security and Optimization

Artificial Intelligence and Machine Learning (AI/ML) are moving from supplemental tools to core infrastructure within payment gateways. Beyond enhancing transaction monitoring and reducing false positives in fraud detection by an estimated 20%-30%, AI is being used for:

Intelligent Routing: Automatically selecting the most cost-effective and highest-approval-rate payment processor in real-time.

Conversion Optimization: Personalizing the checkout experience based on customer behavior and location to maximize successful transactions.

3. The Rise of Embedded Finance

This trend is perhaps the most disruptive. Embedded finance integrates financial tools—including payments, lending, and insurance—directly into the non-financial software platforms that businesses use daily (e.g., vertical SaaS solutions, ERPs, POS systems). Payment gateways are shifting to become Platform Payment Facilitators (PayFacs), offering white-labeled payment solutions to Integrated Software Vendors (ISVs). The global embedded finance market is expected to reach 7.2 trillion by 2030, creating a massive new distribution channel for gateway services.

4. Alternative Payment Methods (APMs)

The dominance of traditional card networks is being challenged by the increasing preference for APMs, particularly digital wallets. Mobile wallets (e.g., Apple Pay, Google Pay, Alipay, WeChat Pay) currently account for approximately 54% of global e-commerce transactions. Furthermore, the market is preparing for the eventual mass adoption of:

Central Bank Digital Currencies (CBDCs): Government-backed digital currencies offering new rails for low-cost, secure transactions.

Tokenization and Biometrics: Using tokens to replace sensitive card data and biometric authentication (facial, fingerprint) to deliver frictionless security and enhance user convenience.

Competitive Landscape

The competitive landscape is a high-stakes arena marked by consolidation, fierce price competition, and diversification beyond core processing.

Major Players and Market Strategies

The market is bifurcated between global giants that span both acquiring and gateway services, and nimble fintechs specializing in API-first technology:

Company Type | Key Players | Strategic Focus |

|---|---|---|

Traditional Giants | PayPal, Visa, Mastercard, FISERV, Global Payments | Expanding beyond card processing into B2B cross-border (e.g., Visa B2B Connect), treasury management, and integrated services for financial institutions. |

Fintech Innovators | Stripe, Adyen, Block (Square) | Focusing on best-in-class developer experience, API scalability, and global reach for complex enterprise needs. They are leading the charge in embedded finance and local payment method coverage. |

E-commerce & Tech Platforms | Amazon Payments, Apple Pay, Google Pay | Leveraging massive user bases and closed-loop ecosystems to build proprietary, highly convenient checkout experiences, thereby challenging external gateway dominance. |

Competitive Dynamics

The central competitive vector is the race to become the "full-stack" payment partner, offering not just authorization but also value-added services (VAS) like fraud management, currency conversion, subscription billing, and tax compliance. Integrated Software Vendors (ISVs) are now key partners, and often competitors, as they embed payments directly, cutting out third-party vendors. The transition to cloud-native platforms, particularly the migration to the ISO 20022 messaging standard, is a critical battleground for legacy providers looking to match the agility of newer entrants.

Regional Insights

Market growth rates vary significantly based on regulatory maturity, internet penetration, and e-commerce readiness.

North America (NA)

Market Position: Dominant market leader (approx. 36% share) due to a highly mature financial infrastructure, advanced e-commerce penetration, and the presence of global headquarters for major players (Stripe, PayPal).

Opportunity: The primary focus is infrastructure modernization (FedNow adoption) and further expansion of the embedded finance model across vertical SaaS sectors.

Asia Pacific (APAC)

Market Position: Fastest-growing region, with countries like India and China registering some of the highest CAGRs (e.g., India projected at 26.5%).

Growth Drivers: Exponential growth in mobile connectivity, favorable government policies promoting cashless societies (India's UPI, China's digital yuan exploration), and a rapidly expanding middle class driving new e-commerce consumption, particularly in Tier-2 and Tier-3 cities. The sheer volume of mobile wallet usage makes this region critical.

Europe

Market Position: Highly dynamic, driven primarily by strong regulatory initiatives.

Growth Drivers: Open Banking mandates (PSD2/PSD3) driving account-to-account payment innovation, and the rollout of SEPA Instant Payments across the Eurozone. Gateways need to excel at compliance and leveraging open banking APIs for new payment methods.

Challenges & Risks

Despite the buoyant outlook, significant challenges persist, demanding proactive risk mitigation strategies from market participants.

1. Escalating Fraud and Cybersecurity Threats

The rapid digitization of payments offers a larger attack surface. Sophisticated cybercrime, including synthetic identity fraud and account takeovers, requires continuous, heavy investment in next-generation security measures. The risk of data breaches remains the foremost concern for merchants and consumers, necessitating strict adherence to global standards like PCI DSS.

2. Regulatory Fragmentation and Compliance Burden

Operating across diverse geographies demands compliance with numerous, often conflicting, regulatory frameworks—from anti-money laundering (AML) and know-your-customer (KYC) rules to data localization requirements. This complexity increases operational costs and hinders rapid international expansion, particularly for smaller fintechs.

3. Interoperability and Legacy System Integration

Many large banks and enterprises still rely on fragmented, legacy payment infrastructure. Integrating modern, API-first payment gateways with these decades-old systems is technically challenging, costly, and time-consuming, creating friction in end-to-end payment processing.

4. Pricing Pressure and Commoditization

The core function of payment authorization is increasingly commoditized, forcing down transaction fees. New entrants (especially ISVs and open-source payment modules) introduce intense pricing pressure, compelling established providers to justify their margins by offering high-value, non-core services like advanced analytics, treasury services, and fraud guarantee models.

Opportunities & Strategic Recommendations

To capitalize on the market's explosive growth, stakeholders—from established financial institutions to venture-backed startups—must adopt forward-looking strategies centered on integration and intelligence.

Strategic Recommendations for Stakeholders

1. Prioritize Investment in API-First, Cloud-Native Architecture

Recommendation: Traditional providers must accelerate the migration of their core processing stacks to modern cloud infrastructure, prioritizing API-centric design. This ensures scalability, reduces latency, and facilitates immediate adoption of new payment rails (RTP, CBDCs) without requiring cumbersome, multi-year legacy system overhauls.

2. Embrace the Embedded Finance Ecosystem

Recommendation: Instead of only competing with ISVs, payment gateways should actively partner with them. Offering Banking-as-a-Service (BaaS) and white-labeled payment facilitator solutions allows gateways to capture transaction volume at the source, transforming the software platform into a new revenue-generating distribution channel.

3. Focus on Cross-Border B2B Modernization

Recommendation: While B2C has seen immense innovation, B2B cross-border payments remain slow and expensive. Gateways should target this friction point by leveraging new technologies like ISO 20022 for rich data exchange and adopting blockchain-based settlement solutions to reduce fees and transaction times from days to near-real-time.

4. Transform Data into Revenue with AI

Recommendation: Utilize AI/ML not just for defense, but for offense. Gateways sit on vast amounts of transaction data. Developing data monetization services—such as offering anonymized competitive intelligence, customized risk scoring, or sophisticated loyalty program management tools to merchants—can open high-margin, value-added revenue streams far beyond simple transaction fees.

5. Localize for the APAC Growth Wave

Recommendation: Strategic expansion in APAC requires deep localization, not just translation. This means supporting key domestic payment methods (e.g., UPI, PromptPay, Alipay), securing local regulatory licenses, and building infrastructure to comply with regional data localization laws, recognizing that mobile-first and QR code payments dominate consumer preferences.

The Payment Gateway Market stands at the nexus of technology, regulation, and consumer behavior. Success in the next decade will belong to organizations that can seamlessly weave their infrastructure into the digital fabric of global commerce, making payments invisible, intelligent, and instantaneous.

Browse More Reports:

Global Algae Fertilizers Market

Global Construction Film Market

Global Antimicrobial Agent Market

Global Benchtop Laboratory Water Purifier Market

Asia-Pacific Feed Flavours and Sweeteners Market

Global Catenary Infrastructure Market

Global Bus Public Transport Market

Latin America Point of Care Infectious Disease Market

Global Innovation Management Market

Middle East and Africa Indium Market

Global Antibiotics Market

Global Potassium Humate Biostimulants Market

Africa MDI, TDI, Polyurethane Market

Global Dental Diode Lasers Market

Middle East and Africa Artificial Turf Market

Global Hematologic Malignancies Market

Latin America Ostomy Devices Market

Asia-Pacific Rotomolding Market

Philippines Microgrid Market

Global Automated Beverage Carton Packaging Machinery Market

Global Surgical Power Tools Market

Europe Intensive Care Unit (ICU) Ventilators Market

Global Vasodilators Market

Global Methylene Diphenyl Diisocyanate (MDI), Toluene Diisocyanate (TDI) and Polyurethane Market

Global Constrictive Pericarditis Market

Middle East and Africa q-PCR Reagents Market

Global Artificial Turf Market

Global Styrene Butadiene Latex Market

Global Digital Farming Software Market

Global Alpha Linolenic Acid Market

Global Head and Neck Cancer Drug Market

Europe Liver Fibrosis Treatment Market

About Data Bridge Market Research:

An absolute way to forecast what the future holds is to comprehend the trend today!

Data Bridge Market Research set forth itself as an unconventional and neoteric market research and consulting firm with an unparalleled level of resilience and integrated approaches. We are determined to unearth the best market opportunities and foster efficient information for your business to thrive in the market. Data Bridge endeavors to provide appropriate solutions to the complex business challenges and initiates an effortless decision-making process. Data Bridge is an aftermath of sheer wisdom and experience which was formulated and framed in the year 2015 in Pune.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email:- corporatesales@databridgemarketresearch.com