The global waste management industry is transitioning from a traditional disposal model to a sophisticated, technology-driven resource recovery ecosystem. Driven by aggressive circular economy mandates, exponential urbanization, and unprecedented digital innovation, the market presents a high-growth trajectory and a compelling landscape for strategic investment. This report provides a detailed analysis of the market dynamics, technological shifts, and strategic pathways for stakeholders looking to capitalize on this essential global sector.

Executive Summary

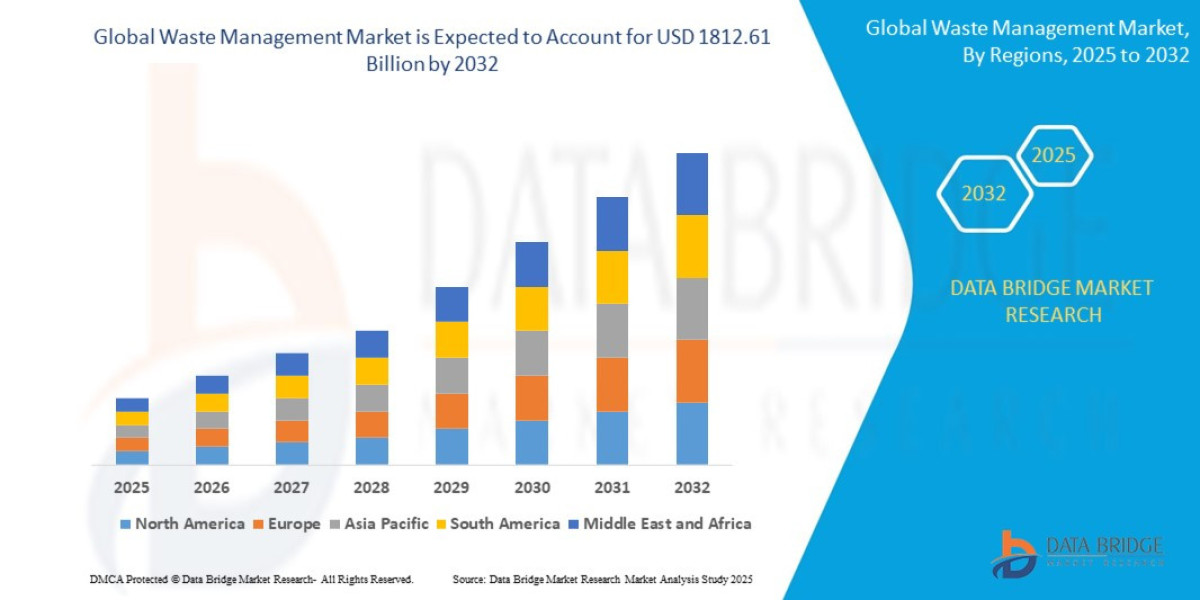

- The global waste management market was valued at USD 1163.33 billion in 2024 and is expected to reach USD 1812.61 billion by 2032

- During the forecast period of 2025 to 2032 the market is likely to grow at a CAGR of 5.70%,

This growth is fueled by key strategic shifts: the integration of IoT and Artificial Intelligence (AI) into sorting and routing processes, the rise of advanced recycling technologies (chemical recycling), and a powerful legislative push towards decarbonization and material recovery. While Asia-Pacific leads in market size due to rapid urbanization, North America and Europe drive innovation through stringent compliance and high investment in circular models. Investors and industry players must focus on digital integration and resource optimization to unlock long-term value in this evolving sector.

Market Overview

The Waste Management Market is defined by the services and technologies required to handle waste materials from their point of generation through to final disposal or recovery. It operates on a hierarchical structure: reduction, reuse, recycling, recovery, and disposal (landfilling or incineration).

Key Segments

The market is typically segmented across three dimensions:

Service Type:

Collection and Transportation: Dominant segment, often accounting for over 60% of the revenue, driven by essential logistical needs.

Disposal: Historically the largest revenue generator (primarily landfills), but facing regulatory pressure.

Recycling and Resource Recovery: The fastest-growing segment, fueled by circular economy goals.

Waste Type:

Municipal Solid Waste (MSW): The highest volume segment, driven by residential and commercial sources.

Industrial Waste: The largest revenue contributor, requiring specialized and often hazardous material handling.

E-Waste: The fastest-growing sub-segment (projected CAGR exceeding 10%), posing a severe environmental risk but offering high material recovery value.

Source: Residential, Commercial, and Industrial (the fastest growing source due to rising manufacturing and construction activity).

Core Market Drivers

The primary drivers of market expansion are multifaceted:

Urbanization and Population Growth: Global population expansion and the concentration of people in urban centers are exponentially increasing the sheer volume of MSW, demanding scalable infrastructure.

Stringent Regulatory Compliance: Governments globally are adopting stricter regulations (e.g., EU waste directives, U.S. EPA guidelines, and EPR schemes) that mandate higher diversion rates and place the onus of post-consumer waste management onto product manufacturers.

Decarbonization Goals: The waste sector is a major source of methane emissions from landfills. This drives investment into Waste-to-Energy (WtE) and Anaerobic Digestion (AD) facilities to convert waste into recoverable energy or fuel, aligning with global climate targets.

Circular Economy Mandates: The shift from a linear 'take-make-waste' model to a circular one elevates the value proposition of recycling, reuse, and closed-loop systems, forcing capital expenditure into material recovery facilities (MRFs) and advanced processing.

Market Size & Forecast

- The global waste management market was valued at USD 1163.33 billion in 2024 and is expected to reach USD 1812.61 billion by 2032

- During the forecast period of 2025 to 2032 the market is likely to grow at a CAGR of 5.70%,,

For More Information Visit https://www.databridgemarketresearch.com/reports/global-waste-management-market

Key Trends & Innovations

The industry is undergoing a digital and chemical revolution, moving beyond mechanical sorting and simple disposal. Four core trends define the near-term strategic roadmap:

1. The Digitalization of Collection and Logistics (IoT and AI)

The integration of Internet of Things (IoT) sensors and Artificial Intelligence (AI) is optimizing the historically inefficient collection process.

Smart Bins and Sensors: IoT sensors installed in commercial and residential bins monitor fill levels in real-time. This data feeds into central platforms to enable dynamic route optimization, moving away from fixed collection schedules. This cuts fuel consumption (up to 20%), reduces labor costs, and lowers the carbon footprint of fleets.

AI-Powered Sorting: In Material Recovery Facilities (MRFs), robotic arms equipped with AI computer vision systems can identify and sort materials (including hard-to-distinguish polymer types) at speeds and accuracy levels far exceeding human capacity. This significantly reduces contamination rates and boosts the value of recovered recyclates.

2. Advanced Recycling and Chemical Processing

To meet ambitious recycling targets, particularly for plastics, the industry is investing heavily in technologies that break down materials to their molecular level.

Chemical Recycling: Unlike mechanical recycling, which degrades plastic quality, chemical recycling (e.g., pyrolysis and gasification) breaks down waste polymers into their original monomers or valuable petrochemical feedstocks. This enables the creation of "virgin-equivalent" plastic, making a truly closed-loop system possible for hard-to-recycle and contaminated plastics.

Waste-to-Energy (WtE) and Anaerobic Digestion (AD): While incineration is controversial, modern WtE plants are critical for dealing with non-recyclable residual waste, converting it into heat and electricity. AD, focusing on organic waste, produces biogas (a renewable natural gas) and digestate (a soil improver), essential for reducing potent methane emissions from landfills.

3. Extended Producer Responsibility (EPR) Schemes

EPR is rapidly transforming the financial structure of the industry. This regulatory mechanism mandates that producers are responsible for the entire life cycle of their products, including collection, recycling, and final disposal.

Shifting Cost Burden: EPR shifts the financial burden from taxpayers/municipalities to the product manufacturers, creating a multi-billion dollar compliance market.

Investment Trigger: This directly incentivizes manufacturers to design products for recyclability (Design for Environment) and forces the waste management sector to invest in the advanced infrastructure needed to fulfill manufacturer obligations. The recent expansion of EPR to new streams, such as textiles and construction materials, indicates its growing global influence.

4. Circular Economy Platforms and Digital Product Passports

The shift toward circularity requires robust tracking. New software platforms and the concept of Digital Product Passports (DPPs) use technologies like Blockchain to track materials, components, and products through their lifecycle. This transparency is crucial for verifying recycled content claims, ensuring compliance with EPR regulations, and establishing trust in secondary material markets.

Competitive Landscape

The global waste management market exhibits a moderately fragmented structure, characterized by a few multinational giants dominating developed markets and a host of thousands of smaller regional and local operators.

Major Global Players

The competitive dynamics are defined by integrated service providers who manage the entire value chain from collection to disposal/recovery. Key players include:

Waste Management, Inc. (WM): Dominant in North America, with a focus on comprehensive service, landfill management, and renewable energy from landfill gas.

Veolia Environnement S.A. & Suez: European giants with vast international footprints, specializing in water, waste, and energy optimization services, driven heavily by circular economy contracts in Europe and Asia.

Republic Services: Another North American leader, known for strategic acquisitions and operational efficiency.

Competitive Strategies

Vertical Integration and Consolidation: Major players focus on acquiring regional service providers to expand geographical reach and consolidate market share. Integration allows for economies of scale, especially in collection and transport logistics.

Technology-as-a-Service: Increasing focus on offering specialized, high-margin services, particularly for complex streams like hazardous, medical, and e-waste, utilizing advanced treatment technologies.

Circular Economy Partnerships: Strategic alliances with manufacturers (OEMs) and major retailers to manage their specific waste streams (EPR compliance), guaranteeing a supply of high-quality feedstock for recycling operations.

Decarbonization Investment: Investing in infrastructure that reduces carbon emissions (e.g., RNG from landfills, WtE, fleet electrification) to secure long-term municipal and government contracts that prioritize environmental performance.

Regional Insights

Market maturity, regulatory stringency, and waste generation volume vary significantly across major geographies, creating unique market opportunities.

Asia Pacific (APAC)

APAC is universally recognized as the largest market by volume and is the fastest-growing region (CAGR estimated above 6.5%).

Drivers: Rapid industrialization, massive urbanization (especially in China, India, and Indonesia), and a burgeoning middle class driving consumption.

Opportunity: The immense volumes of MSW and industrial waste require colossal investment in formal infrastructure. Currently, large portions of waste are managed informally or end up in uncontrolled dumpsites. This offers a significant greenfield opportunity for private and public-private partnerships (PPPs) in advanced recycling, formalizing collection, and developing WtE facilities.

North America (NA)

North America currently holds the largest revenue share in the global market, characterized by a highly mature and consolidated service industry.

Drivers: High per-capita waste generation rates (the U.S. being among the world leaders), strict regulations from the EPA on hazardous waste, and strong private sector investment in innovative technologies (AI sorting, RNG from landfills).

Focus: The focus is on optimization—improving landfill safety and capacity, investing in fleet technology, and adopting smart city solutions for collection efficiency.

Europe

Europe is the global regulatory and innovation leader, driven by the ambitious goals of the European Union’s Circular Economy Action Plan.

Drivers: Aggressive targets (e.g., 65% recycling of municipal waste by 2035; limiting landfilling to 10%), mandatory EPR implementation across various product streams, and high public environmental awareness.

Focus: Due to limited landfill space and high penalties for disposal, the market is structurally biased towards high-value recovery, WtE, and chemical recycling capacity building. This region is a prime testing ground for novel resource-recovery technologies.

Challenges & Risks

While the market's trajectory is positive, several structural and financial hurdles must be navigated:

Volatile Commodity Pricing: The profitability of recycling and resource recovery services is highly dependent on global spot market prices for recovered materials (plastics, metals, paper). Price volatility complicates long-term investment payback calculations for advanced recycling facilities.

Infrastructural Lag in Developing Nations: Rapid urbanization in APAC and Africa often outpaces the development of formal collection and processing infrastructure. This results in reliance on informal sectors and uncontrolled disposal, which poses significant public health and environmental risks.

High Capital Expenditure for Innovation: Implementing smart systems, AI sorting robotics, and advanced chemical recycling requires substantial initial capital investment and specialized expertise, creating high barriers to entry for smaller firms.

Regulatory Uncertainty: While regulations drive growth, inconsistency in enforcement or sudden shifts in policy (e.g., bans on certain WtE technologies or cross-border waste shipment restrictions) can quickly destabilize business models.

Opportunities & Strategic Recommendations

For investors, startups, and established players, the future of waste management lies in leveraging technology to close the loop between waste generation and material reuse.

Strategic Recommendations

Stakeholder Group | Strategic Focus Area | Actionable Recommendation |

|---|---|---|

Investors & Private Equity | High-Growth Technology & Resource Recovery | Target investments in specialized e-waste and hazardous waste processing firms, and finance companies focused on chemical recycling and biogas infrastructure. These offer premium margins and protection from commodity price swings. |

Established Service Providers | Digital Transformation & Integration | Prioritize the integration of AI-powered sorting systems in MRFs and deploy end-to-end IoT/data platforms for route optimization. Use data analytics to predict waste volumes and optimize asset utilization across the fleet. |

Startups & Innovators | EPR and Data Compliance Solutions | Develop software and data platforms that help producers comply with complex EPR schemes globally. Focus on traceable resource tracking (e.g., using blockchain) to provide verified environmental data to manufacturers. |

Manufacturers (Waste Generators) | Decarbonization and Circular Sourcing | Engage in long-term contracts with waste firms that guarantee material recovery and low-carbon disposal. Invest in 'Design for Environment' principles to reduce waste at the source and lower future EPR obligations. |

Browse More Reports:

Middle East and Africa Microgrid Market

Global Febuxostat Market

Global Carbon Steel Market

Global Consumer Chemical Packaging Market

Global Plasmonic Solar Cell Market

Global Electro-medical and Electrotherapeutic Apparatus Market

Global Network Test Lab Automation Market

Global Reclaimed Rubber Market

Global Personal Care Ingredients Market

Global Protein Ingredients in Infant Nutrition Market

Middle East and Africa Frozen Ready Meals Market

Global Surgical Gown Market

Global Navigation Satellite System (NSS) Chip Market

Saudi Arabia q-PCR Reagents Market

Global Aluminum Pigments Market

Global Bearing Isolators Market

Asia-Pacific Ostomy Devices Market

North America Digital Farming Software Market

Global Reconstituted Juice Market

Global Organic Emulsifier Market

Global Metal Cans Market

Asia-Pacific Healthcare Logistics Market

Global Protein Ingredients Market

Global Regulatory Affairs Outsourcing Market

Global Self-Service Kiosks Market

Global Specialty Gas Market

Global Bathroom - Toilet Assist Devices Market

Global Benzenecarboxylic Acid Market

Global Aerospace Fasteners Market

Global Phenol Derivatives Market

Global Mucosal Atomization Devices Market

Europe After Market Combustion Engine Repairs Market

About Data Bridge Market Research:

An absolute way to forecast what the future holds is to comprehend the trend today!

Data Bridge Market Research set forth itself as an unconventional and neoteric market research and consulting firm with an unparalleled level of resilience and integrated approaches. We are determined to unearth the best market opportunities and foster efficient information for your business to thrive in the market. Data Bridge endeavors to provide appropriate solutions to the complex business challenges and initiates an effortless decision-making process. Data Bridge is an aftermath of sheer wisdom and experience which was formulated and framed in the year 2015 in Pune.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email:- corporatesales@databridgemarketresearch.com