Executive Summary

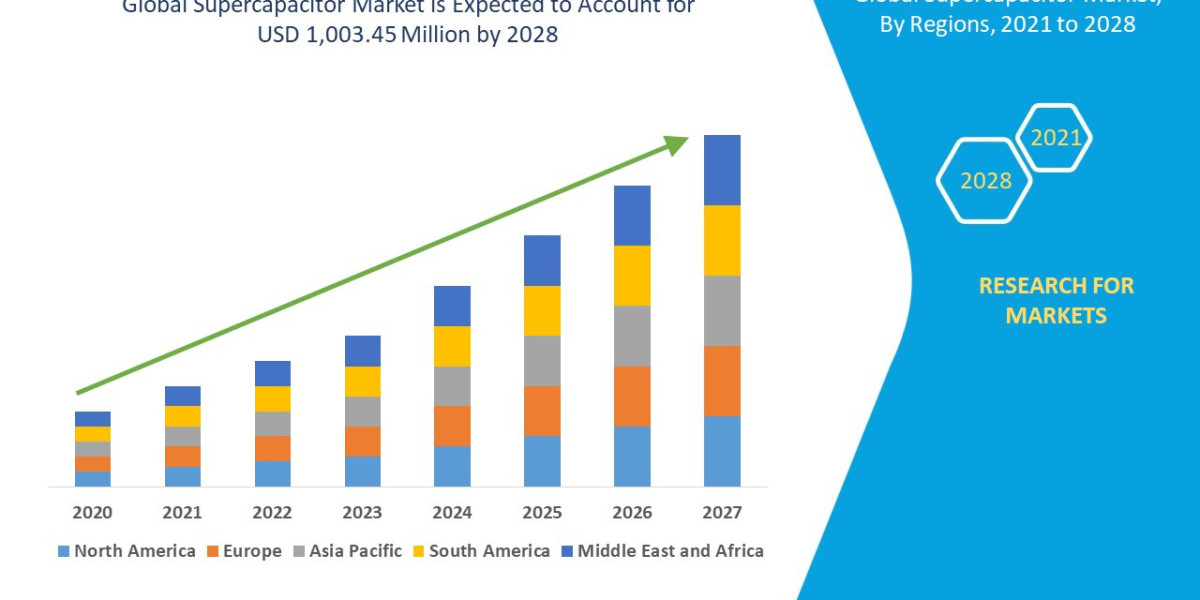

The global supercapacitor market size was valued at USD 642.37 million in 2024 and is projected to reach USD 1556.72 million by 2032, with a CAGR of 11.70% during the forecast period of 2025 to 2032.

Market Overview

Definition and Core Technology

A supercapacitor is an electrochemical capacitor that stores energy through the reversible adsorption of ions onto the surface of a highly porous, high-surface-area electrode material (usually activated carbon). Unlike batteries, which store energy through chemical reactions, supercapacitors store electrostatic charge, enabling extremely fast charge/discharge rates and cycles often exceeding one million.

Key Market Segments by Type

Electric Double-Layer Capacitors (EDLCs) (Dominant Segment): Rely purely on electrostatic charge separation at the electrode-electrolyte interface. They offer the highest power density and cycle life.

Pseudocapacitors: Utilize faradaic (redox) reactions on the electrode surface, typically involving metal oxides or conducting polymers, to store charge. They provide higher energy density than EDLCs but sometimes at the cost of cycle life.

Hybrid Capacitors (Fastest Growing): Combine a battery-type electrode (often Li-ion) with a capacitor-type electrode. This merger aims to significantly boost energy density while retaining much of the supercapacitor’s high power and cycle life characteristics (e.g., Lithium-Ion Capacitors or LICs).

Key Market Segments by End-Use Application

Automotive and Transportation (Largest Share): Used in kinetic energy recovery systems (KERS) in hybrid electric vehicles (HEVs), regenerative braking in trams and rail systems, and peak power assist for heavy-duty electric trucks and buses.

Energy and Utility: Critical for load leveling, instantaneous power quality enhancement, and pitch control in wind turbines. Also utilized for smoothing the intermittent power flow from solar and wind farms onto the grid.

Industrial: Employed in momentary power bridging (UPS/backup), industrial power tools, automation systems, and heavy machinery (e.g., harbor cranes, forklift trucks) requiring fast acceleration and deceleration.

Consumer Electronics: Used for flash photography power, memory backup, and quick-charging features in portable devices.

Drivers and Current Dynamics

Electrification Mandates: Global regulatory pushes (e.g., EU, China) requiring lower carbon emissions are accelerating the adoption of HEVs and full EVs, where supercapacitors complement batteries by handling high-power, short-duration demands.

Demand for Grid Modernization: The intermittent nature of renewable energy sources necessitates fast-response storage to maintain grid stability and power quality, a role perfectly suited to supercapacitors.

Longevity and Durability: In heavy-duty and industrial environments, the cycle life of supercapacitors (often 10-15 years) significantly reduces the total cost of ownership compared to chemical batteries, making them a preferred choice.

Miniaturization: Innovations in electrode materials are allowing manufacturers to shrink component size while maintaining power output, opening doors for integration into smaller electronics and IoT devices.

Market Size & Forecast

The global supercapacitor market size was valued at USD 642.37 million in 2024 and is projected to reach USD 1556.72 million by 2032, with a CAGR of 11.70% during the forecast period of 2025 to 2032.

For More information Visit https://www.databridgemarketresearch.com/reports/global-supercapacitor-market

Key Trends & Innovations

Innovation in the supercapacitor space is centered on materials science and system integration to challenge the energy density dominance of lithium-ion batteries.

1. Advanced Nanomaterial Electrodes

The pursuit of higher surface area and better ion conductivity is driving research into next-generation electrode materials:

Graphene and Carbon Nanotubes (CNTs): These materials offer theoretical surface areas significantly higher than traditional activated carbon. When successfully integrated, they promise substantial increases in both energy and power density, but scalable, cost-effective manufacturing remains a challenge.

Metal Oxides and Sulfides: Used extensively in Pseudocapacitors, materials like ruthenium oxide (RuO2) and manganese dioxide (MnO2) are being paired with carbon substrates to maximize the synergistic effects of electrostatic and faradaic storage.

2. Hybridization (Lithium-Ion Capacitors - LICs)

The most critical commercial innovation is the rise of LICs. These devices utilize a pre-lithiated carbon electrode (like a Li-ion battery anode) combined with a supercapacitor cathode.

Impact: LICs offer 2-3 times the energy density of traditional EDLCs, bringing them closer to low-power Li-ion batteries while maintaining a 5-10 times greater cycle life. This makes them ideal for intermediate applications where both high energy and long life are necessary, such as HEV acceleration boosts.

3. Module Integration and Voltage Stacking

Individual supercapacitor cells have low operating voltages (typically 2.5V to 3.0V). The trend is to integrate hundreds of cells into standardized, high-voltage modules (48V,125V,750V) complete with integrated Battery Management Systems (BMS) equivalents.

Advantage: These modular systems simplify integration for OEMs (Original Equipment Manufacturers), providing a ready-to-use, rugged power source for large-scale applications like grid storage and commercial vehicles.

4. Solid-State and Flexible Supercapacitors

For consumer electronics and wearables, R&D is focused on eliminating liquid electrolytes to create solid-state devices. Additionally, flexible, thin-film supercapacitors are being developed to be woven into fabrics or applied to curved surfaces for wearable tech and smart packaging.

Competitive Landscape

The market exhibits a competitive dichotomy: strong dominance by specialized Asian firms in the EDLC segment, and fierce competition among established Western companies in the system-level and hybrid component markets.

Major Players and Competitive Strategies

Maxwell Technologies (now part of Tesla/Panasonic): Historically a dominant player, particularly in the US automotive segment. Strategy is deeply integrated with electric vehicle development, focusing on high-volume, low-cost cell production and module standardization.

Nippon Chemi-Con (Japan): A legacy capacitor giant, leveraging its robust, established supply chain and manufacturing scale to dominate the industrial and electronic backup segments with reliable EDLC products.

Skeleton Technologies (Estonia/Germany): A European leader distinguished by its proprietary "Curved Graphene" electrode material, which promises industry-leading power and energy density. Their strategy targets high-performance, niche segments like aerospace, motorsport, and defense.

KEMET (now part of Yageo) and CAP-XX (Australia): Focus on the small-form-factor and consumer electronics market, competing on size, thinness, and integration capacity for devices like flash power and small IoT sensors.

Key Competitive Strategies

Cost Parity with Lead-Acid Batteries: Aggressive scaling of production (Gigafactories for capacitors) and optimizing activated carbon synthesis to drive down the cost per Farad (F), making supercapacitors an economically justifiable alternative to traditional batteries in many industrial roles.

Vertical Integration: Securing the supply of high-purity carbon materials and electrolytes to control quality and cost, particularly prevalent among large Asian manufacturers.

Intellectual Property (IP) Protection: Investing in patents for novel electrode materials (e.g., graphene composites) and electrolyte formulations to create proprietary advantages in energy density and lifespan.

Regional Insights

Asia-Pacific (APAC)

The Manufacturing and Consumption Hub. APAC, particularly China, Japan, and South Korea, dominates the global supercapacitor manufacturing base due to favorable access to raw materials and established electronics supply chains. China is also the largest consumer, driven by extensive investment in electric buses, trams, and high-speed rail infrastructure, where supercapacitors are essential for regenerative braking. The region accounts for over 50% of the global market.

North America (NA)

Technology Adoption and Grid Focus. NA is a key region for application development, particularly in renewable energy integration and defense. Investment is concentrated in developing sophisticated hybrid capacitor systems and large-scale utility-grade energy storage modules to enhance grid resilience and manage peak demand.

Europe

High-Performance and Clean Mobility. Europe leads in the adoption of supercapacitors for high-performance applications like motorsport (KERS) and advanced heavy industrial machinery. Strict EU emissions standards also drive their integration into HEVs and micro-hybrid vehicles (Start-Stop systems). R&D, led by companies like Skeleton, focuses heavily on cutting-edge materials.

Challenges & Risks

1. Energy Density Limitation

Despite advancements, the energy density of supercapacitors (typically <10 Wh/kg) is still 10-20 times lower than that of commercial lithium-ion batteries (∼150−250 Wh/kg). This limits their use as primary long-duration energy sources for pure EVs or utility-scale bulk storage.

2. High Initial Cost

While the cost per cycle is low, the initial capital expenditure (CapEx) for a supercapacitor module remains significantly higher per watt-hour (W⋅h) than a battery. This cost barrier is the primary deterrent for mass-market consumer applications.

3. Voltage Limitations and Self-Discharge

The low operating voltage per cell requires complex cell-stacking and balancing circuitry, adding complexity and cost. Furthermore, supercapacitors suffer from a higher self-discharge rate than batteries, making them unsuitable for long-term, low-power storage applications.

4. Raw Material Dependence

The quality and consistency of raw materials, especially high-purity activated carbon and specialized electrolytes, are critical. Supply chain risks related to these materials can impact cost and large-scale deployment efforts.

Opportunities & Strategic Recommendations

Stakeholder Group | Strategic Recommendation | Rationale |

|---|---|---|

Component Manufacturers | Prioritize Hybrid (LIC) Development. Shift R&D focus from pure EDLCs to Lithium-Ion Capacitors (LICs) to achieve energy density closer to batteries while retaining high power/cycle life. | This opens up the lucrative, high-volume HEV and light-duty commercial vehicle market, which requires a blend of high energy and power. |

Automotive OEMs | Mandate Supercapacitors in 48V Micro-Hybrid Systems. Integrate supercapacitor modules into all 48V mild-hybrid vehicle platforms for efficient regenerative braking and peak power assist during acceleration. | Maximizes fuel efficiency gains and drastically extends the life of the 48V battery, justifying the component cost through long-term TCO reduction. |

Utility and Grid Operators | Deploy Modular Supercapacitor Banks for Power Quality. Use supercapacitor storage specifically for frequency regulation, voltage support, and short-duration power bridging in critical substation infrastructure. | Supercapacitors' millisecond-response time is unmatched by batteries for power quality stabilization, enhancing grid reliability in high-renewable energy environments. |

Investors & Venture Capital | Target Graphene-based Electrode Scale-Up. Invest in startups that have moved past laboratory proof-of-concept and have a clear, scalable roadmap for mass-producing high-quality, cost-effective graphene and CNT electrodes. | This is the technology that offers the potential leap in energy density required to truly challenge Li-ion in certain segments, representing a high-reward investment. |

Industrial/Heavy-Duty Equipment Makers | Standardize on Supercapacitor Systems for Cyclic Loads. Integrate standardized 750V supercapacitor modules for all lifting, propulsion, and braking systems in equipment like cranes, port machinery, and mining trucks. | Capitalizes on the supercapacitors' key strength: millions of deep-discharge cycles, drastically reducing maintenance and replacement costs in heavy industrial operations. |

Browse More Reports:

North America Plant Based Protein Market

Global Radiotheranostics Market

Europe Small Molecule Sterile Injectable Drugs Market

Global Tachycardia Drugs Market

Global Terminal Automation Market

Global Pipeline Transportation Market

North America Polyimide Films Market

Global Propylene Glycol Market

Global Electric Heat Tracing (EHT) Market

Global Digital Assistant Market

Europe Molded Plastics Market

Global Individual Quick Freezing (IQF) Meat and Poultry Market

Global Internet of Things (IoT) Node and Gateway Market

Global Idiopathic Intracranial Hypertension Treatment Market

Global Blast Chillers Market

North America Testing, Inspection, and Certification (TIC) Market for Building and Construction – Industry Trends and Forecast to 2028

Middle East and Africa Food Bags Market

Latin America Rotomolding Market

Global Automotive Energy Absorption (EA) Pads Market

Europe Methylene Diphenyl Diisocyanate (MDI) Toluene Diisocyanate (TDI) and Polyurethane Market

Global Doors Market

Global Insulation Coating Materials Market

Europe Acute Lymphocytic/Lymphoblastic Leukemia (ALL) Diagnostics Market

Global Cercarial Dermatitis Market

Global X-Ray Fluorescence Analyser Market

Middle East and Africa IoT Node and Gateway Market

Global Blood Meal Market

Global Two Part Adhesive Market

Middle East and Africa Potato Processing Market

Europe Indium Market

North America Probe Card Market

Europe Molecular Diagnostics Services Market

About Data Bridge Market Research:

An absolute way to forecast what the future holds is to comprehend the trend today!

Data Bridge Market Research set forth itself as an unconventional and neoteric market research and consulting firm with an unparalleled level of resilience and integrated approaches. We are determined to unearth the best market opportunities and foster efficient information for your business to thrive in the market. Data Bridge endeavors to provide appropriate solutions to the complex business challenges and initiates an effortless decision-making process. Data Bridge is an aftermath of sheer wisdom and experience which was formulated and framed in the year 2015 in Pune.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email:- corporatesales@databridgemarketresearch.com