Executive Summary

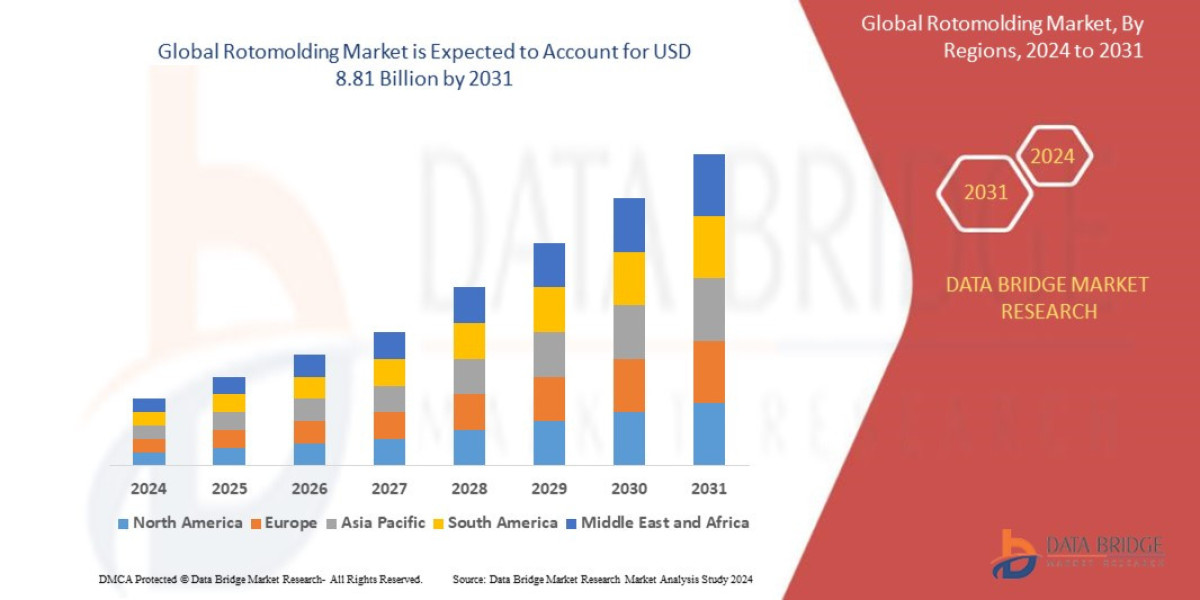

Global rotomolding market size was valued at USD 1.90 billion in 2024 and is projected to reach USD 3.03 billion by 2032, growing with a CAGR of 6.1% during the forecast period of 2025 to 2032.

Market Overview

The Rotomolding Market involves the process of rotational molding, where powdered polymer resin is placed into a hollow mold, heated while being rotated biaxially, and then cooled. This process results in seamless, uniform, and hollow plastic products. This technology is particularly well-suited for manufacturing large, complex shapes and parts where strength and low weight are critical.

Key Segments

The market can be segmented by the core material used and the application industry:

By Material:

Polyethylene (PE): Dominates the market (over 80% share) due to its excellent impact strength, chemical resistance, affordability, and easy processability. High-density polyethylene (HDPE) and Linear Low-density polyethylene (LLDPE) are the most common variants.

Polypropylene (PP): Used where higher temperature resistance and rigidity are required, though less common than PE.

Polyvinyl Chloride (PVC) Plastisols: Used primarily for smaller, flexible parts like boots or bellows.

Other Polymers: Includes Nylon, Polycarbonate, and various specialized resins for high-performance applications.

By Application:

Tanks and Containers: The largest segment, including chemical storage tanks, water tanks, septic tanks, and industrial bins.

Automotive: Growing segment, focused on fuel tanks, truck bed liners, air ducts, and complex interior/exterior components where weight reduction is crucial.

Construction and Infrastructure: Includes portable sanitation units, road barriers, and drainage products.

Consumer Goods: Includes kayaks, playground equipment, toys, and specialized furniture.

Drivers and Dynamics

Low Tooling Costs: Compared to injection molding, rotomolding tools are simpler and significantly cheaper, making it economically viable for short production runs or very large components.

Product Design Freedom: The process allows for excellent design flexibility, including molded-in inserts, complex geometries, double walls, and internal graphics, which is a major advantage for product developers.

Substitution of Traditional Materials: The strong push for vehicle lightweighting and improved fuel efficiency in the automotive sector is driving the replacement of metal components with high-performance rotomolded plastics.

Growth in Water Management: Increasing global necessity for efficient water storage, agriculture, and chemical handling systems is fueling demand for large, durable polyethylene tanks.

The current dynamic involves intense material science innovation aimed at improving scratch resistance, UV stability, and barrier properties for specialized fluid storage.

Market Size & Forecast

Global rotomolding market size was valued at USD 1.90 billion in 2024 and is projected to reach USD 3.03 billion by 2032, growing with a CAGR of 6.1% during the forecast period of 2025 to 2032.

For More Information Visit https://www.databridgemarketresearch.com/reports/global-rotomolding-market

Key Trends & Innovations

Innovation in the rotomolding sector focuses heavily on material science, process efficiency, and improving part complexity.

Enhanced Material Performance: There is a major trend towards specialty polymer grades. This includes cross-linked polyethylene (XLPE) for superior chemical resistance and durability, and new micro-pellet formulations that improve flow and reduce pinholes, resulting in higher-quality finishes.

Compound Molding and Multi-layer Products: Manufacturers are moving beyond single-layer products to create multi-layer parts. This allows for:

Foam Cores: Adding a layer of foam for insulation (e.g., cooler boxes) or structural rigidity without adding significant weight.

Barrier Layers: Incorporating specialized resins to prevent fuel or chemical permeation (critical for automotive fuel tanks).

Smart Rotomolding: The integration of Industry 4.0 technologies is critical. This includes:

Real-time Monitoring: Using IoT sensors embedded in molds to monitor internal air temperature and pressure, allowing for precise control over the heating and cooling cycles.

Predictive Maintenance: Leveraging data analytics to predict when molds require maintenance or replacement, minimizing unplanned downtime.

Surface Aesthetics and Finishing: Innovations in mold release agents and surface textures allow for high-gloss, textured, or even graphic finishes directly in the mold, reducing the need for post-molding painting or finishing steps, thus cutting costs.

Competitive Landscape

The Rotomolding Market is characterized by a fragmented structure dominated by regional and local custom molders, but with several large international players who command material supply and high-volume industrial segments. Competition is primarily based on tooling expertise, material sourcing capabilities, and proximity to end-use markets.

Major Players and Market Dynamics:

Custom Molders (Global): Companies like Tricel, Rotomoulding S.p.A., and The Roto-Group offer highly specialized contract manufacturing services, leveraging expertise in complex design and large-part production.

Resin Suppliers: Global chemical giants like Dow, ExxonMobil, LyondellBasell, and SABIC play a crucial role, as the quality and availability of specialized PE powder directly impact the molders' competitiveness.

Equipment Manufacturers: Companies like FSP Machinery and Persico Group are leaders in providing advanced, automated rotomolding machines and tooling solutions.

Competitive Strategies:

Vertical Integration: Larger players are increasingly integrating resin compounding and finishing services to ensure quality control and capture more margin across the value chain.

Niche Specialization: Companies focus on mastering specific, high-regulation applications, such as medical device enclosures or specialized ADR approved tanks, which require stringent quality control and certification.

Design-for-Rotomolding Consulting: Molders are moving up the value chain by offering engineering and design consulting to clients, helping them convert parts originally intended for other processes (like metal fabrication) into rotomolded solutions.

Regional Insights

Market demand and application focus vary across major geographical regions.

North America: A mature market with high capital investment in the automotive, industrial tank, and construction sectors. Demand here is high for complex, durable, and highly specified components, driven by strong environmental regulations concerning fluid storage.

Europe: Focused heavily on sustainability and precision. European molders are leaders in using recycled polymers and implementing strict quality standards for marine, agricultural, and industrial applications. Demand is steady, driven by the replacement cycle for existing infrastructure.

Asia-Pacific (APAC): The fastest-growing market globally. Driven by massive infrastructure projects (water management, sanitation), rapid industrialization, and strong growth in the region's automotive manufacturing base (especially China and India). The sheer volume of demand for water and chemical storage tanks makes this a major growth engine.

Latin America, Middle East, and Africa (LAMEA): Emerging regions with strong demand for basic, high-volume products like water storage tanks, agricultural bins, and road barriers, reflecting high investment in foundational public services and infrastructure.

Challenges & Risks

Despite the market's advantages, rotomolding faces unique technical and commercial barriers.

Long Cycle Times: Rotomolding is inherently a slower process compared to injection molding (cycle times can be 1-3 hours). This limits high-volume production of small parts and can impact capacity utilization.

Material Limitations: The process is heavily reliant on polyethylene. While innovation is occurring, the material selection is still more limited than for injection molding, posing a challenge for applications requiring extremely high stiffness or high heat deflection temperatures.

Wall Thickness Control: Achieving consistent wall thickness, especially in corners or complex mold geometries, remains a technical challenge that requires high levels of operator skill and advanced machinery calibration.

Environmental Concerns over Waste: While the process itself generates less material waste than others, the end-of-life disposal of large plastic products (tanks, kayaks) remains an environmental challenge that requires robust recycling programs.

Opportunities & Strategic Recommendations

The unique capabilities of rotomolding present clear avenues for specialized growth and market dominance.

For Manufacturers and Molders:

Embrace Automation and IoT: Invest in automated loading/unloading systems and, critically, mold IoT sensor technology to reduce cycle times and minimize scrap rates. Automation is the key to closing the competitiveness gap with injection molding.

Target Lightweighting: Aggressively pursue opportunities in the automotive, aerospace, and defense sectors by showcasing the cost-benefit analysis of replacing metal tanks and ducts with advanced, multi-layer, rotomolded plastic components.

Develop Barrier Solutions: Focus R&D on creating specialized barrier-layer technologies for EV battery cooling fluid tanks and highly corrosive industrial chemicals to capture high-margin, regulatory-intensive markets.

For Resin Suppliers:

Commercialize Sustainable Resins: Accelerate the development and commercial availability of consistent, high-flow, post-consumer recycled (PCR) PE powder grades and bio-based polymers to support the industry's sustainability goals.

Performance Polymers: Invest in rotomolding-compatible grades of Nylon and cross-linked materials that can handle higher operating temperatures, thus broadening the market application base.

For Investors:

Target investment in equipment manufacturers specializing in automated, multi-station shuttle machines, which address the cycle time constraints inherent in the process.

Look for opportunities in custom molders that hold proprietary certifications (e.g., FDA, NSF) for medical, food, or chemical contact applications, ensuring a strong competitive moat.

Browse More Reports:

Europe Flotation Reagents Market

Global Wearable Fitness Trackers Market

Global Industrial Hearable Market

Global Micro Tube Box Market

Global Perimeter Defence System Market

Global Printed Textile Market

Italy Dental Practice Management Software Market

Global Smart Factory Market

India Food Ingredients Market

Europe q-PCR Reagents Market

Global NAND Flash Memory Market

Europe Food Bags Market

Global Wax and Wax Esters Market

Global Micro-Electromechanical Systems (MEMS) Gyroscopes Market

Middle East and Africa Probe Card Market

Global Injection Trays Market

Global Cord Blood and Cell Banking Market

Europe Protein Hydrolysates Market

Global Laminated Veneer Lumber Market

Middle East and Africa Wind Turbine Pitch System Market

Global Commercial Cleaning Equipment Market

North America Protein Hydrolysates Market

Middle East and Africa Rotomolding Market

Global (GPS) Global Positioning Systems Market

Global Sever’s Disease Treatment Market

Australia Specialty Gas Market

Global Below Grade Waterproofing Membrane Market

Middle East and Africa Intensive Care Unit (ICU) Ventilators Market

Global Beeswax Market

Europe Commercial Cleaning Equipment Market

Global Flooring and Carpets Market

Asia-Pacific Liver Fibrosis Treatment Market

About Data Bridge Market Research:

An absolute way to forecast what the future holds is to comprehend the trend today!

Data Bridge Market Research set forth itself as an unconventional and neoteric market research and consulting firm with an unparalleled level of resilience and integrated approaches. We are determined to unearth the best market opportunities and foster efficient information for your business to thrive in the market. Data Bridge endeavors to provide appropriate solutions to the complex business challenges and initiates an effortless decision-making process. Data Bridge is an aftermath of sheer wisdom and experience which was formulated and framed in the year 2015 in Pune.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email:- corporatesales@databridgemarketresearch.com