Executive Summary

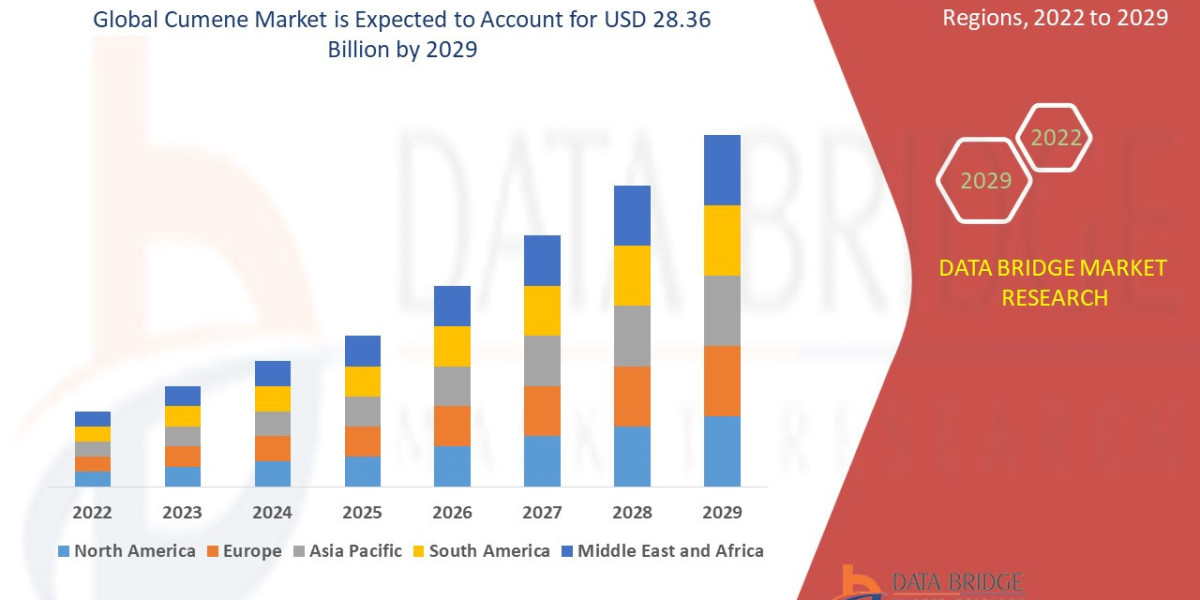

Global cumene market size was valued at USD 22.43 billion in 2024 and is projected to reach USD 32.64 billion by 2032, with a CAGR of 4.80% during the forecast period of 2025 to 2032.

Market Overview

The Cumene Market is defined by the production and trade of isopropylbenzene, a critical chemical compound synthesized via the alkylation of benzene with propylene. Cumene itself has limited direct end-use; its market dynamics are overwhelmingly determined by the demand for its two primary derivatives, produced through the highly industrialized cumene hydroperoxide process.

Key Segments and Derivatives

The market segmentation is best understood through its downstream applications, as nearly 98% of global cumene supply is channeled into the following areas:

Phenol Production (Major Segment): This is the largest consumer of cumene. Phenol is vital for:

Bisphenol A (BPA): The precursor for polycarbonate plastics (used in automotive parts, compact discs, medical devices) and epoxy resins (used in protective coatings, adhesives, and electrical laminates).

Caprolactam: Used to manufacture Nylon 6 fibers and engineering plastics.

Phenolic Resins: Essential in construction materials, abrasives, insulation, and adhesives.

Acetone Production: Produced as a co-product of phenol (in a ratio of roughly 1:0.6). Acetone’s uses include:

Methyl Methacrylate (MMA): The monomer for Plexiglass (PMMA), used extensively in construction, lighting, and automotive glazing.

Solvents: Used in coatings, paints, and specialty cleaning applications.

Other Applications (Minor Segment): Includes the production of alpha-methylstyrene and specialty solvents.

Drivers and Current Dynamics

Automotive Sector Growth: The sustained global demand for vehicles, especially in APAC, directly drives the need for polycarbonate (PC) (for lightweight car parts and lighting) and MMA (for interior and exterior components).

Construction and Infrastructure Spending: Significant infrastructure projects worldwide rely heavily on epoxy resins and phenolic resins for protective coatings, high-performance adhesives, and insulation materials.

Electronics Manufacturing: The proliferation of electronic devices increases demand for high-purity phenol derivatives used in laminates for printed circuit boards (PCBs) and specialty resins.

Supply Chain Integration: The current dynamic is heavily focused on vertical integration. Major players seek to control the full value chain, from securing feedstocks (benzene and propylene) to producing the final derivatives (phenol/acetone), which helps mitigate price volatility and secure downstream margins.

Market Size & Forecast

Global cumene market size was valued at USD 22.43 billion in 2024 and is projected to reach USD 32.64 billion by 2032, with a CAGR of 4.80% during the forecast period of 2025 to 2032.

For More Information Visit https://www.databridgemarketresearch.com/reports/global-cumene-market

APAC Phenol/Acetone Capacity: The massive and ongoing capacity expansion for phenol and acetone production in China and Southeast Asia remains the primary engine of cumene demand. These expansions are aimed at satisfying domestic manufacturing and reducing reliance on imports.

Lightweighting in Automotive: The shift toward electric vehicles (EVs) and stricter fuel efficiency standards boost demand for lighter materials like polycarbonate, which requires phenol, thus bolstering cumene consumption.

Stabilizing Feedstock Costs: While volatile, improved crude oil market stability in the mid-term is expected to provide more predictable operating costs for cumene producers, stabilizing pricing and investment confidence.

Key Trends & Innovations

The innovation landscape in the Cumene Market focuses almost entirely on efficiency, selectivity, and process sustainability.

Zeolite Catalyst Technology: The industry-standard is shifting towards the latest generation of Zeolite-based catalysts (specifically MCM−22 family). These heterogeneous catalysts offer several critical advantages over older solid phosphoric acid (SPA) and aluminum chloride catalysts:

Higher Selectivity: Maximizing the conversion of benzene and propylene directly into cumene, reducing by-product formation.

Lower Operating Temperatures: Significantly cutting energy consumption during the exothermic alkylation reaction.

Longer Catalyst Life: Reducing turnaround time and operational costs.

Energy Efficiency in Distillation: Due to the energy-intensive nature of purifying cumene from unreacted feedstocks and by-products, advanced heat integration techniques, heat pumps, and complex distillation column designs are being adopted to minimize thermal energy use.

BPA Alternatives and Sustainability: The growing public and regulatory concern over BPA (an endocrine disruptor) is a major trend. Manufacturers are investing in the research and development of non-phenol-based BPA alternatives (e.g., isosorbide, TCD-diol) or seeking new, essential applications for phenol and acetone to offset potential demand loss in consumer-facing products.

Integrated On-Demand Production: New facilities are increasingly built adjacent to both feedstock suppliers (refineries/cracking facilities for propylene/benzene) and downstream consumers (phenol/acetone plants). This direct-pipeline integration minimizes transportation costs and volatility exposure.

Competitive Landscape

The Cumene Market is characterized by high barriers to entry due to the capital-intensive nature of petrochemical plant construction, the need for integrated feedstock supply, and the necessity of proprietary process technology.

Major Players:

The market is dominated by global chemical and oil & gas majors, who often produce cumene for captive consumption in their own downstream phenol/acetone facilities. Key players include:

INEOS Group Holdings S.A. (Europe/Global)

ExxonMobil Chemical Company (US/Global)

Dow Chemical Company (US/Global)

BASF SE (Europe/Global)

Mitsui Chemicals, Inc. (Japan/Asia)

Shell Chemical L.P. (Global)

Competitive Strategies:

Vertical Integration: The most common strategy is backward integration into feedstocks (propylene and benzene) and forward integration into derivatives (Phenol, Acetone, BPA, MMA). This minimizes margin erosion from feedstock volatility.

Scale and Optimization: Operating world-scale facilities to capitalize on economies of scale and continuously investing in proprietary, highly selective catalyst technologies to achieve the lowest cost of production.

Geographical Proximity: Strategic capacity expansion in high-growth regions like APAC to reduce logistics costs and capture local demand directly.

Specialty Grades: Focusing on high-purity cumene for specific applications where quality tolerance is extremely tight (e.g., aerospace composites, high-end electronics).

Regional Insights

The geographical distribution of production and consumption reflects the global shift in manufacturing and industrial activity.

Asia-Pacific (APAC): The dominant region in both production capacity and consumption. China is the largest consumer, driven by its massive construction, electronics, and automotive industries. This region's growth is rapidly outpacing mature markets, making it the primary target for new capacity additions. The increasing number of domestic producers in China is intensifying intra-regional competition.

North America: A mature market characterized by integrated production facilities utilizing cheap natural gas-derived feedstocks. While consumption growth is moderate, the region remains a key global exporter of cumene and its derivatives, prioritizing technological innovation and specialty grades.

Europe: A highly developed but slower-growth market, heavily influenced by stringent environmental regulations, particularly regarding BPA. Production here is highly optimized, focusing on niche, high-value applications and advanced sustainability practices.

Middle East & Africa (MEA): An emerging region for production. MEA countries, particularly in the Persian Gulf, are leveraging abundant, low-cost oil and gas resources to establish large-scale integrated petrochemical complexes. Their output is primarily aimed at export to APAC and Europe.

Challenges & Risks

The capital-intensive nature of the Cumene Market exposes it to several significant risks that affect margins and investment planning.

Feedstock Price Volatility: Benzene and propylene are direct derivatives of crude oil and natural gas. Their price fluctuations are the single largest variable cost, directly impacting the profitability of cumene and its downstream products.

Regulatory Scrutiny on BPA: The greatest long-term structural risk is the potential phase-out of Bisphenol A (BPA) in consumer products due to health concerns. Since BPA accounts for a large portion of phenol demand, a significant global ban would necessitate complex re-alignment of cumene-phenol capacity and require immediate investment in alternative phenol uses.

Risk of Oversupply: Capacity additions, often occurring in large, integrated projects (especially in China), can quickly lead to market oversupply, temporarily suppressing margins and profitability across the entire value chain.

Technological Obsolescence: Reliance on older, less selective catalyst technology can quickly render a plant non-competitive against newer facilities equipped with advanced Zeolite systems, requiring costly retrofits.

Opportunities & Strategic Recommendations

Despite the cyclical nature and regulatory hurdles, the Cumene Market offers robust opportunities driven by necessity and industrial growth.

For Manufacturers and Producers:

Focus on Process Efficiency: Immediate adoption of the latest generation Zeolite catalysts and heat integration technology is mandatory to maintain a top-quartile cost position. Operational efficiency is the primary hedge against feedstock volatility.

Geographical Investment: Target investment and capacity expansion in strategic locations within the APAC region to capture domestic growth, but ensure flexibility to export when regional dynamics change.

Phenol Derivative Diversification: While BPA alternatives are emerging, focus on securing growth in the non-BPA phenol segments, such as phenolic resins for high-performance adhesives, electronic components, and composite materials (e.g., wind turbine blades).

For Investors:

Target Integrated Players: Favor companies that are vertically integrated, controlling both propylene/benzene inputs and the downstream BPA/MMA outputs, as they are better insulated from chemical spread volatility.

Evaluate BPA Risk Readiness: Invest in firms actively developing and scaling BPA alternatives or those with a high proportion of phenol/acetone sales destined for applications with low regulatory risk (e.g., MMA).

For Technology Suppliers:

Develop BPA-Free Phenol Pathways: Investigate R&D into highly specialized, sustainable phenol derivatives that offer superior performance without the health risk profile of BPA, creating new, high-margin markets for cumene derivatives.

Modular and Efficient Plant Design: Offer modular, rapidly deployable cumene plant designs that minimize construction time and allow producers to quickly react to regional demand shifts.

Browse More Reports:

Global Ring Pull Caps Market

Middle East and Africa Fuse Market

Global Automotive Cluster Market

Global Aerospace and Defense C Class Parts Market

Global Ostomy Devices Market

Global Disconnector Market

Middle East and Africa Rice Husk Ash Market

Europe Retail Analytics Market

Global D-Malic Acid Market

Global Hereditary Breast and Ovarian Cancer Syndrome Treatment Market

Global High Intensity Discharge (HID) Light Market

Global Visual Electrophysiology Testing Devices Market

Global Next-Generation Sequencing (NGS) Services Market

Global Spark Plug Market

Global Agriculture Biological Control Agents Market

Europe Fuse Market

Global Abatacept Market

Global Whole Genome Bisulfite Sequencing (WGBS) Market

Global Cervical Intraepithelial Neoplasia Drugs Market

Global Facial Tissue Paper Market

Global Wrist Replacement Orthopedic Devices Market

Global Frozen Ready Meals Market

Global Medical Device Interface Market

Global Mass Notification Systems Market

Global Chondrodermatitis Nodularis Helicis Market

Global Indium Market

Global Winged Bean Seeds Market

Global Porcine Vaccines Market

Global Metal Trauma Implants Market

Global Maple Syrup Urine Disease Treatment Market

Global Performance Analytics Market

Global Off-Grid Controller Market

About Data Bridge Market Research:

An absolute way to forecast what the future holds is to comprehend the trend today!

Data Bridge Market Research set forth itself as an unconventional and neoteric market research and consulting firm with an unparalleled level of resilience and integrated approaches. We are determined to unearth the best market opportunities and foster efficient information for your business to thrive in the market. Data Bridge endeavors to provide appropriate solutions to the complex business challenges and initiates an effortless decision-making process. Data Bridge is an aftermath of sheer wisdom and experience which was formulated and framed in the year 2015 in Pune.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email:- corporatesales@databridgemarketresearch.com