Executive Summary

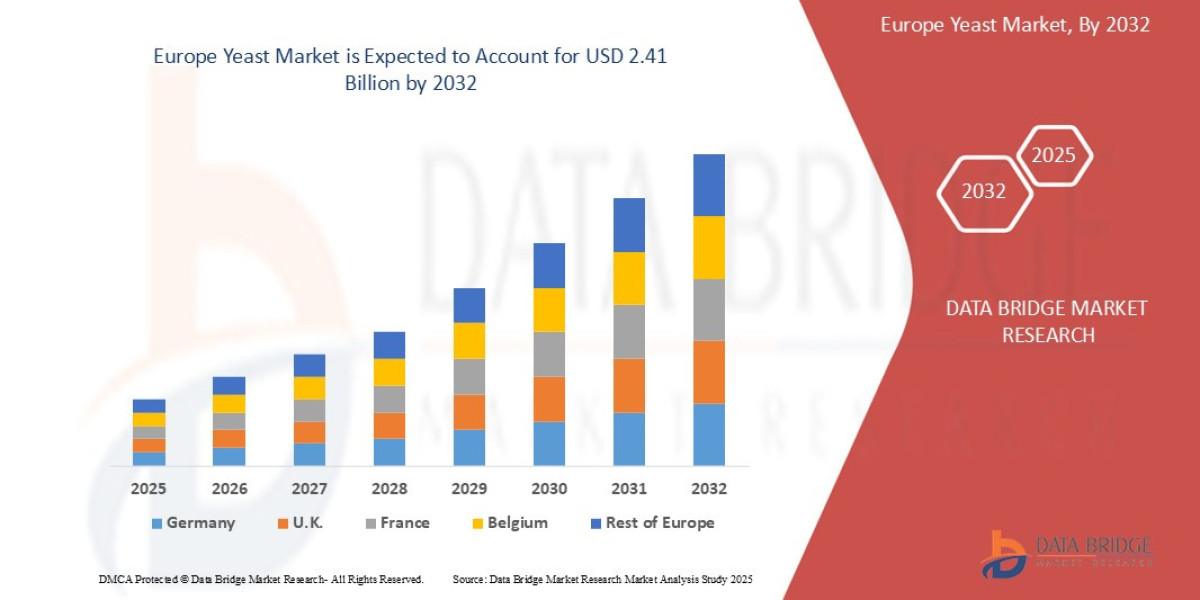

- The Europe Yeast market size was valued at USD 1.67 billion in 2024 and is expected to reach USD 2.41 billion by 2032, at a CAGR of 4.70% during the forecast period

Market Overview

The Europe Yeast Market comprises all products derived from or utilizing yeast microorganisms. It is a critical supply sector, supporting core industries from artisan bakeries to large-scale bio-refineries. The market is highly influenced by agricultural commodity prices (especially molasses, the primary feedstock) and consumer shifts in diet and lifestyle.

Key Segments

By Type (Product Form):

Baker’s Yeast (Largest Volume): Used in bread, pizza, and pastry production, sold in compressed, instant dry, and active dry forms. Demand is stable, driven by artisan and home baking trends.

Brewer’s Yeast: Used for fermentation in beer production. Also reclaimed as a byproduct for nutritional/feed use.

Feed Yeast: Used as a nutritional supplement in animal and aquaculture feed, improving gut health and performance.

Nutritional and Food Yeast (Fastest Growth): Includes yeast extracts (umami flavor enhancers), yeast autolysates, and inactive yeast flakes (high in B vitamins and protein). This segment is driven by the clean label and vegan trends.

By Application:

Food and Beverages (Dominant Revenue): Baking, brewing, wine/spirits, and flavor enhancement.

Feed: Poultry, swine, and aquaculture.

Industrial/Biofuel: Ethanol production.

Drivers and Current Dynamics

Clean Label and Natural Fermentation: European consumers strongly favor products with minimal, recognizable ingredients. Yeast is inherently accepted as a natural ingredient, boosting the demand for baker's yeast and yeast extracts as natural flavor enhancers, replacing artificial MSG.

Plant-Based Revolution: The dramatic increase in vegan and vegetarian diets across Western Europe has made nutritional yeast an essential, high-demand product as a non-animal source of complete protein and Vitamin B12.

Biofuel Mandates: EU renewable energy directives support the production of bioethanol as a fuel additive, maintaining a steady, large-scale industrial demand for specific high-performance yeast strains.

Gut Health and Immunity: Consumer health consciousness post-pandemic has increased interest in functional foods. Yeast β-glucans and specialized prebiotic strains are gaining traction in the functional food and nutraceutical sectors for immune and gut support.

Market Size & Forecast

- The Europe Yeast market size was valued at USD 1.67 billion in 2024 and is expected to reach USD 2.41 billion by 2032, at a CAGR of 4.70% during the forecast period

For More Information Visit https://www.databridgemarketresearch.com/reports/europe-yeast-market

Key Trends & Innovations

Innovation in the European yeast market is focused on functional optimization, sustainability, and technological precision.

Non-GMO and Non-Saccharomyces Strains: There is a heightened focus on developing and commercializing non-GMO yeast strains (a key concern for European consumers) and specialized non-Saccharomyces yeast (e.g., Torulaspora delbrueckii, Kluyveromyces lactis). These strains offer unique functionalities like reduced alcohol content in beverages, improved shelf life, and distinct flavor profiles.

Yeast-Based Alternative Proteins: Beyond nutritional flakes, companies are exploring large-scale production of high-quality yeast protein isolate for texturization and use in hybrid meat and dairy alternatives. This taps into the sustainable protein trend without the land use issues associated with traditional agriculture.

Waste-to-Value Streamlining (Circular Economy): European manufacturers are increasingly investing in technologies to utilize agricultural waste (e.g., spent grain from brewing, fruit pomace) as fermentation feedstock instead of traditional molasses. This reduces cost volatility and improves the product's environmental footprint.

Precision Fermentation for Bio-Chemicals: Advanced fermentation techniques are being used to engineer yeast to produce high-value bio-chemicals, flavors, and vitamins (e.g., carotenoids, vitamins K2 and D2), positioning yeast as a versatile bioreactor platform.

Competitive Landscape

The Europe Yeast Market is highly consolidated, dominated by a few multinational giants that control technology, global supply chains, and extensive product portfolios.

Major Players:

Lesaffre Group (France): A global leader and European powerhouse with vast production capacity across baking, nutritional, and industrial yeast segments. Its strategy emphasizes geographic expansion (especially in CEE) and high-tech fermentation R&D.

Angel Yeast Co., Ltd. (China - Strong European Presence): A rapidly expanding global competitor, challenging incumbents through competitive pricing and significant investment in new EU production and distribution centers.

Lallemand Inc. (Canada - Global Specialist): Strong focus on specialized industrial, brewing, and functional/health yeast segments, competing on technical expertise and customized solutions rather than commodity volume.

Associated British Foods plc (ABF): Significant presence through its baking ingredients division, primarily focused on the industrial baking sector in the UK and parts of Western Europe.

Competitive Strategies:

Vertical Integration: Dominant players maintain control over the entire supply chain, from sourcing molasses and building fermentation vessels to final distribution, hedging against commodity price risks.

Acquisition of Niche Expertise: Larger firms actively acquire small, specialized companies focused on unique non-Saccharomyces strains or specific nutritional applications (β-glucans, probiotics) to rapidly expand their high-value portfolio.

Technical Support and Formulation: For industrial clients (bakeries, breweries), competition often centers on providing superior technical support and customized yeast blends that optimize client production lines (e.g., faster proofing, greater alcohol yield, enhanced flavor stability).

Sustainability Reporting: Leading companies compete by transparently reporting on ESG metrics, particularly water usage, CO2 emissions, and feedstock sustainability, a crucial factor for major EU food corporations.

Regional Insights

Demand and application maturity vary significantly across the European sub-regions.

Western Europe (France, Germany, Benelux):

Focus: High demand for high-quality baker's yeast (reflecting artisan bread tradition), premium brewer's yeast (craft beer boom), and the largest market for high-value nutritional yeast and functional extracts due to affluent, health-conscious consumers.

Dynamics: Highly consolidated retail sector and demanding B2B industrial segments.

Southern Europe (Italy, Spain):

Focus: Significant use of baker's yeast in pizza and pastry production; strong industrial demand for yeast in wine/spirits production (fermentation starters). Emerging nutritional yeast market.

Central and Eastern Europe (CEE):

Focus: Price sensitivity is higher, leading to strong demand for cost-effective commodity baker’s yeast and feed yeast. The region also serves as a major manufacturing hub for global players due to lower operating costs, supplying the entire EU market.

UK and Nordics:

Focus: Strong penetration of yeast extracts (e.g., Marmite), high adoption of nutritional yeast aligned with strong vegan/plant-based trends, and stable demand for industrial yeast.

Challenges & Risks

The mature nature of the European market, combined with external commodity pressures, poses several risks.

Raw Material Price Volatility: The reliance on molasses (a sugar beet/cane byproduct) ties yeast production costs directly to volatile global sugar markets, making stable long-term pricing difficult.

Intense Price Competition in Commodity Segments: Despite consolidation, the industrial and commodity baker’s yeast sectors face continuous pressure on margins, especially from low-cost imports, forcing manufacturers to focus on automation and efficiency.

Regulatory Hurdles for New Strains: Gaining EFSA (European Food Safety Authority) approval for novel or genetically modified (even non-GMO engineered) yeast strains for food applications can be a lengthy, costly, and restrictive process.

Shifts in Alcohol Consumption: Changing consumer habits, including a trend toward low- and non-alcoholic beer, require yeast manufacturers to rapidly innovate and supply specialized strains that can produce complex flavors without generating high ethanol levels.

Opportunities & Strategic Recommendations

Strategic success in the European market lies in shifting resources from commodity production towards high-value, functional, and sustainable solutions.

For Manufacturers:

Acquire Functional Expertise: Prioritize the acquisition of smaller biotech firms specializing in proprietary non-Saccharomyces or engineered Saccharomyces strains for nutraceutical and bio-chemical production, securing a path to high-margin revenue streams.

Build Closed-Loop Supply Chains: Invest in local CEE or Western European facilities that utilize regional agricultural waste streams as feedstock (e.g., brewery effluent, whey permeate), reducing import reliance and creating a superior sustainability narrative.

For Startups and Innovators:

Target B2B Alternative Protein: Focus on scalable production of highly purified yeast protein isolates and texturizers designed specifically to meet the taste and texture requirements of European meat alternative manufacturers.

Digitalize Technical Services: Offer AI-driven digital tools to optimize fermentation processes for small and medium-sized breweries and distilleries, leveraging expertise to guarantee consistent quality and yield.

For Investors:

Fund Bio-Chemical Platforms: Invest in companies using precision fermentation to produce high-value, sustainable ingredients (e.g., vitamins, specialty lipids) currently synthesized using traditional chemical methods, tapping into the broader bio-economy.

Support CEE Expansion: Fund the build-out or modernization of production facilities in Central and Eastern Europe to capitalize on lower operational costs and better access the large, growing markets of the East while remaining compliant for the West.

Browse More Reports:

Global Mastitis Market

Global Glucocorticoid Agonist Market

Global Ultra-High Barrier Shrink Films Market

North America Sustainable Aviation Fuel Market

North America Lung Cancer Diagnostics Market

Global Cannabidiol (CBD) Infused Edible Market

Global Garage and Service Station Market

Global Physiotherapy Examination Tables Market

Global Composite Bearings Market

Europe Ostomy Devices Market

U.S. Diet and Nutrition Apps Market

Asia- Pacific Plant Based Protein Market

Global Atomic Force Microscope (AFM) Market

Global Sailing Jackets Market

U.S. Electric Enclosure Market

Global Long Fiber Thermoplastics Market

Global Cocoa Processing Equipment Market

Global Medical Tuning Fork Market

Global Modified Bitumen Market

Global Medical Device Cleaning Market

Global Biodetectors and Accessories Market

Global Heavy Metals Testing Market

Global Glucaric Acid Market

Global Ruminant Feed Antibiotics Market

Global Aircraft Thrust Reverser Market

Asia-Pacific Frozen Ready Meals Market

Middle East and Africa Laminated Busbar Market

Global Train Signalling System Market

Global Heat Stabilizers Market

Asia-Pacific Surgical Power Tools Market

North America Frozen Ready Meals Market

Asia-Pacific Algaecides Market

About Data Bridge Market Research:

An absolute way to forecast what the future holds is to comprehend the trend today!

Data Bridge Market Research set forth itself as an unconventional and neoteric market research and consulting firm with an unparalleled level of resilience and integrated approaches. We are determined to unearth the best market opportunities and foster efficient information for your business to thrive in the market. Data Bridge endeavors to provide appropriate solutions to the complex business challenges and initiates an effortless decision-making process. Data Bridge is an aftermath of sheer wisdom and experience which was formulated and framed in the year 2015 in Pune.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email:- corporatesales@databridgemarketresearch.com