Executive Summary

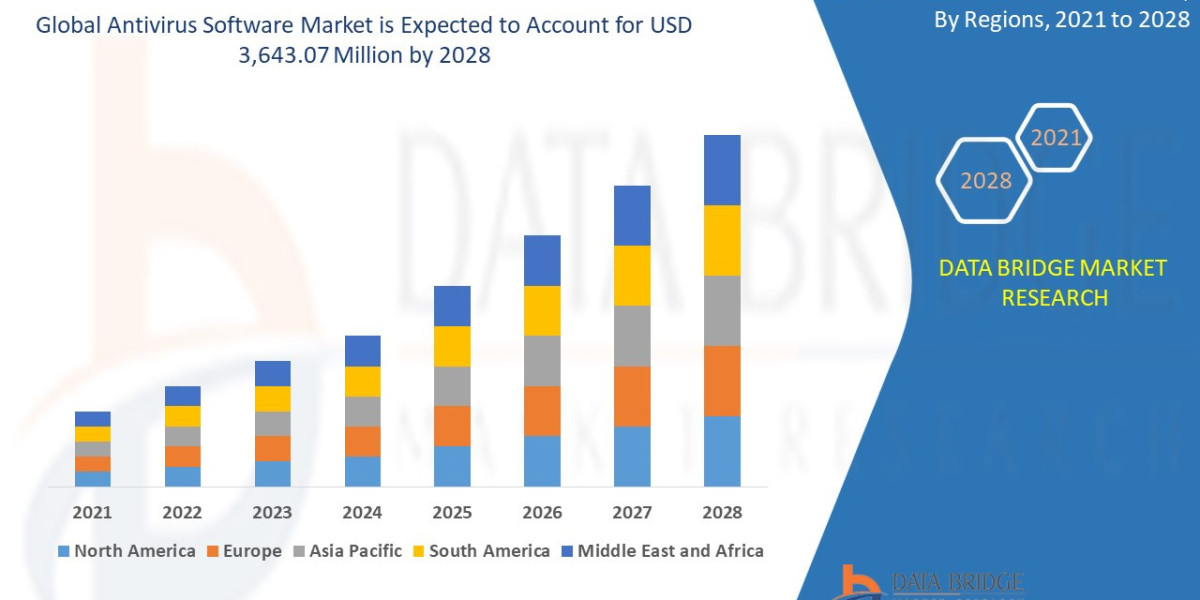

Antivirus software market size is valued at USD 3,643.07 million by 2028 is expected to grow at a compound annual growth rate of 1.6% in the forecast period of 2021 to 2028.

Market Overview

The Antivirus Software Market has evolved from its historical function—identifying and removing known malware via signature files—into a sophisticated segment of the broader cybersecurity industry. Today, the focus is squarely on Endpoint Protection Platforms (EPP) for preventative security and Endpoint Detection and Response (EDR) for post-breach analysis and remediation.

Key Segments:

Solution Type: The market is segmented into EPP (baseline protection), EDR (advanced threat visibility and hunting), and XDR (integrated security across email, cloud, and endpoints). EDR and XDR represent the high-growth, high-value segments.

Deployment Model: Cloud-based (SaaS) and On-premise. Cloud deployment is accelerating rapidly due to scalability and the need to secure distributed, mobile workforces.

End-User: Large Enterprises (dominant revenue share), Small and Medium Enterprises (SMEs, fastest-growing segment), and Consumers. SMEs are rapidly adopting managed EDR services due to a lack of in-house security expertise.

Market Drivers:

Ransomware and Zero-Day Attack Sophistication: The increasing frequency and financial impact of targeted attacks necessitate machine learning-based protection that can detect anomalous behavior rather than just known malware.

The Hybrid Work Model: The permanent shift to distributed work has fragmented the corporate perimeter, making the endpoint (laptop, mobile device) the primary security control point.

Regulatory Compliance: Global data privacy regulations (e.g., GDPR, HIPAA, CCPA) mandate robust data protection and immediate breach reporting, making advanced EDR capabilities essential for compliance.

IoT and OT Security: The proliferation of Internet of Things (IoT) and Operational Technology (OT) devices requires specialized endpoint security agents capable of operating on low-resource hardware.

Current Dynamics: The market is characterized by intense M&A activity and feature convergence. Traditional AV firms are scrambling to acquire or develop EDR and cloud capabilities, while pure-play EDR vendors are expanding into broader XDR suites. Pricing models are shifting from perpetual licensing to subscription-based, per-endpoint pricing, favoring flexibility and scalability.

Market Size & Forecast

Antivirus software market size is valued at USD 3,643.07 million by 2028 is expected to grow at a compound annual growth rate of 1.6% in the forecast period of 2021 to 2028.

For More Information Visit https://www.databridgemarketresearch.com/reports/global-antivirus-software-market

Key Trends & Innovations

The market is currently being reshaped by technological leaps and strategic integrations that prioritize preemptive defense and centralized visibility.

1. The Rise of Extended Detection and Response (XDR)

XDR is the evolution of EDR, moving beyond the endpoint to correlate security data across endpoints, cloud workloads, email, network infrastructure, and identity services. This integration provides a unified, contextual view of an attack, significantly reducing time-to-detect (TTD) and time-to-respond (TTR). XDR is becoming the required architecture for large enterprises to combat the growing problem of security team alert fatigue.

2. AI and Behavioral Analytics as Core Defense

Traditional signature matching is obsolete against polymorphic malware. The industry has shifted entirely to Artificial Intelligence (AI) and Machine Learning (ML) models. These models analyze granular behavioral characteristics (e.g., changes in file execution sequences, memory access patterns) to detect malicious intent before code execution, representing true next-generation protection.

3. Cloud-Native and Agent Consolidation

New platforms are architected to be lightweight, consume minimal resources, and operate entirely from the cloud. This trend facilitates agent consolidation, where a single, unified agent manages EPP, EDR, Vulnerability Management, and Cloud Workload Protection (CWPP), simplifying deployment and reducing endpoint performance drag.

4. Identity as the New Perimeter

As traditional network perimeters dissolve, security focus is shifting to user identity and access. EDR tools are increasingly integrating with Identity and Access Management (IAM) systems to detect lateral movement or privilege escalation immediately following a compromised account login, ensuring the endpoint and the user’s identity are treated as inseparable security vectors.

Competitive Landscape

The Antivirus and Endpoint Security market is highly dynamic, witnessing a clear division between heritage players and disruptive, cloud-native innovators.

Major Players and Market Share Dynamics: The market features three tiers of competition:

Cloud-Native Disruptors (High Growth): Firms like CrowdStrike, SentinelOne, and Cybereason dominate the EDR/XDR space. They benefit from platform agility, AI-first architecture, and a strong presence in the enterprise and MSSP (Managed Security Service Provider) channels.

Legacy/Consolidated Giants (Revenue Leaders): Companies like Gen Digital (NortonLifeLock, Avast, AVG), McAfee, and Trend Micro maintain massive market share, particularly in the consumer and small business EPP segments. Their strategy revolves around bundling identity protection, VPN, and legacy AV solutions.

Ecosystem Integrators (Strategic Threat): Microsoft Defender for Endpoint is rapidly gaining enterprise traction. By leveraging its vast install base (Windows, Azure, Office 365), Microsoft offers integrated security solutions that reduce friction and cost for existing customers, posing a substantial competitive challenge to dedicated third-party vendors.

Competitive Strategies:

Platform Ecosystems: Vendors are competing not just on features but on API integration, positioning their EDR/XDR platforms as the central nervous system for a client's entire security stack.

Pricing Innovation: The adoption of consumption-based or outcome-based pricing models (charging based on metrics like breach prevention success or low TTR) to challenge traditional per-seat licensing.

Targeting SMEs with MDR: Using channel partners (MSPs) to deliver advanced EDR/XDR capabilities to SMEs, effectively democratizing enterprise-grade security.

Regional Insights

While cybersecurity demand is universal, regional growth rates and solution preferences vary based on regulatory maturity, cloud adoption rates, and threat exposure.

Region | Market Dynamics | Key Opportunities |

|---|---|---|

North America | Largest revenue share; highly mature market. Leadership in XDR adoption. Driven by financial services, healthcare, and defense sectors. | Advanced threat hunting services; industrial control system (ICS) security integration; vertical-specific compliance tools. |

Asia Pacific (APAC) | Fastest growing region (CAGR > 13%). Driven by massive digitalization in India, China, and Southeast Asia. Strong governmental interest in local data sovereignty. | Cloud-native EDR for rapidly scaling mid-market firms; mobile device endpoint security (MDM/UEM integration); localized language support. |

Europe | Mature, but constrained by fragmented regulatory landscape (individual national rules supplementing GDPR). Strong preference for vendors adhering to strict data localization standards. | Emphasis on data sovereignty and EU-cloud providers; MDR services for organizations navigating complex cross-border compliance. |

Latin America (LATAM) | Emerging market with high risk exposure due to rapid digital adoption and reliance on legacy IT infrastructure. Price sensitivity is high. | Entry-level cloud EPP subscriptions; focus on educational outreach; leveraging mobile endpoints as the primary compute device. |

Challenges & Risks

The Antivirus Software Market faces several critical challenges that can impede growth and adoption, requiring strategic mitigation.

1. The Cybersecurity Skills Gap

The increasing complexity of EDR and XDR platforms outstrips the ability of many organizations to hire, train, and retain security analysts (SOC staff). This lack of skilled personnel leads to underutilized platform capabilities and reliance on expensive third-party MDR services, increasing the total cost of ownership (TCO).

2. Fragmentation and Vendor Sprawl

Despite the push for XDR consolidation, many large enterprises suffer from vendor sprawl, running multiple overlapping security solutions. This complexity leads to configuration errors, blind spots, and integration challenges that undermine security efficacy.

3. Evasion Techniques and AI Arms Race

Threat actors are constantly innovating to bypass ML models using techniques like obfuscation, fileless attacks, and steganography. This requires vendors to continually invest massive capital in R&D to maintain model accuracy and stay ahead in the predictive security arms race, raising the barrier to market entry for new players.

Opportunities & Strategic Recommendations

The shifting market dynamics present clear opportunities for vendors, investors, and security professionals.

1. Democratization via Managed Services (MDR)

Recommendation for Vendors: Prioritize channel sales and robust partner programs for Managed Detection and Response (MDR). This is the key to unlocking the lucrative SME segment, which lacks the resources for in-house EDR management. MDR providers should focus on vertical expertise (e.g., legal, manufacturing) to offer tailored, compliant security outcomes.

2. Hyper-Focus on Identity-Centric Security

Recommendation for Product Teams: Move beyond device-centric visibility. The next wave of innovation must seamlessly integrate EDR with key Identity Providers (IdPs) like Okta and Azure AD. Products that can instantly freeze an endpoint or revoke session tokens based on behavioral indicators of compromise tied to the user identity (not just the device) will command a premium.

3. Investment in Cloud Workload Protection (CWPP) Integration

Recommendation for Investors: Target startups specializing in Cloud Workload Protection Platforms (CWPP) that offer specialized EDR capabilities for containerized and serverless environments (Kubernetes, AWS Lambda). As enterprise application workloads shift fully to the cloud, the need for endpoint security designed specifically for ephemeral cloud infrastructure will outpace traditional device-centric EDR growth.

4. Simplification of User Interfaces (UI) and Automation

Recommendation for Manufacturers: Reduce the complexity of the Security Operations Center (SOC) analyst experience. Develop playbooks and low-code/no-code Security Orchestration, Automation, and Response (SOAR) capabilities natively within the EDR/XDR console. Success will be measured not just by detection rate, but by the level of automated remediation (mean-time-to-remediate) achieved without human intervention, thereby mitigating the ongoing effects of the skills gap.

Browse More Reports:

Global Tularemia Market

Global Esthetic Dental Restoration Products Market

Global Pine-Derived Chemicals Market

Global MLOPs Market

Global Delivery Robots Market

Global Mobile Money Market

Global Personal Emergency Response System Market

Global Laminated Busbar Market

Global Temperature Sensor Market

Global Smart Payment Systems Market

Middle East and Africa Feed Flavors Sweeteners Market

Global Aromatherapy Market

Global Mouth Freshener Market

Global Automotive Human-Machine Interfaces (HMI)Market

Global Payment Wallet Market

Global Polyimide Films Market

Asia-Pacific Wind Turbine Pitch System Market

Global Reflective Films Packaging Market

Global Tumor Infiltrating Lymphocytes Market

North Americal Heavy Metals Testing Market

Asia-Pacific Intensive Care Unit (ICU) Ventilators Market

Global Pet Diaper Market

Global Tonometers Market

Global Monorail Market

Global Meat Stabilizer Market

Global Photophobia Drug Market

Global Medicated Feed Additives Market

North America Specialty Gas Market

Global Perrault Syndrome Treatment Market

Asia-Pacific Topical Corticosteroids Market

Global Electric Kick Scooters Market

Global Diagnostic Imaging Disposables Market

About Data Bridge Market Research:

An absolute way to forecast what the future holds is to comprehend the trend today!

Data Bridge Market Research set forth itself as an unconventional and neoteric market research and consulting firm with an unparalleled level of resilience and integrated approaches. We are determined to unearth the best market opportunities and foster efficient information for your business to thrive in the market. Data Bridge endeavors to provide appropriate solutions to the complex business challenges and initiates an effortless decision-making process. Data Bridge is an aftermath of sheer wisdom and experience which was formulated and framed in the year 2015 in Pune.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email:- corporatesales@databridgemarketresearch.com