Executive Summary

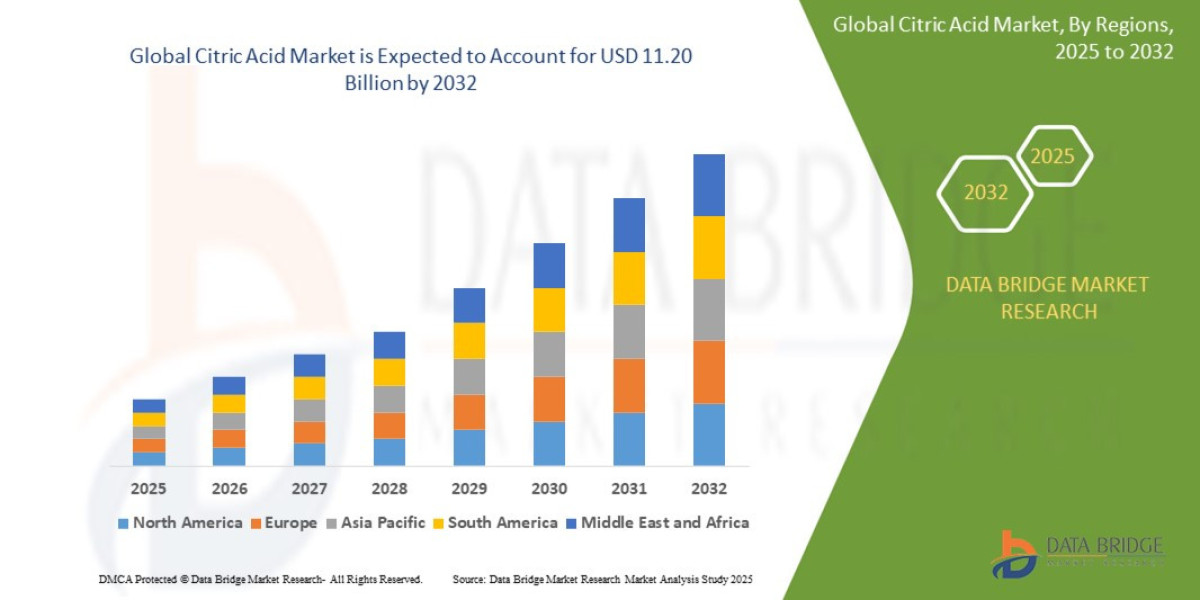

- The global citric acid market size was valued at USD 7.07 billion in 2024 and is expected to reach USD 11.20 billion by 2032, at a CAGR of 5.92% during the forecast period

Market Overview

Defining Citric Acid and Its Production

Citric Acid (CA) is a weak organic acid naturally found in citrus fruits. Commercially, nearly all CA is produced through the fermentation of carbohydrate substrates (typically corn starch, molasses, or sugar beet syrup) by the fungus Aspergillus niger. The resulting product is available in two main forms: Citric Acid Anhydrous (water-free) and Citric Acid Monohydrate (containing one molecule of water).

Key Application Segments

The versatility of CA ensures its extensive use across multiple industries, with the F&B sector accounting for approximately 70-75% of total consumption volume.

Food and Beverages (F&B): The largest segment, where CA acts as:

Acidulant: Imparts a sharp, sour flavor, essential in soft drinks, confectionery, and fruit-flavored products.

Preservative: Lowers pH to inhibit microbial growth, extending the shelf life of jams, jellies, and packaged foods.

Emulsifier/Stabilizer: Used in dairy and cheese products.

Pharmaceuticals and Nutraceuticals: Used in effervescent tablets, as an anticoagulant, as a buffering agent, and to enhance the solubility and bioavailability of drugs.

Industrial and Household Cleaners: Functions as an excellent chelating agent (binds metal ions) in detergents, descaling agents, and environmental water treatment solutions, prized for its biodegradability.

Cosmetics and Personal Care: Employed as an alpha-hydroxy acid (AHA) in skin care products for pH adjustment and exfoliation.

Drivers and Current Market Dynamics

Dominant Driver: Beverage Consumption: The relentless growth in demand for carbonated soft drinks, ready-to-drink (RTD) teas, flavored water, and fruit juices globally is the primary engine for CA volume.

Shifting Supply Chain: The market has historically experienced volatility due to high concentration of production capacity, particularly in China. Current dynamics include global efforts to diversify sourcing geographically following geopolitical and trade friction.

The Chelating Advantage: The rising global focus on environmental regulations is accelerating the displacement of less biodegradable chelating agents (like phosphates) with CA in cleaning and water treatment applications.

Market Size & Forecast

- The global citric acid market size was valued at USD 7.07 billion in 2024 and is expected to reach USD 11.20 billion by 2032, at a CAGR of 5.92% during the forecast period

For More Information Visit https://www.databridgemarketresearch.com/reports/global-citric-acid-market

Key Trends & Innovations

The Citric Acid industry is undergoing subtle but important technological and consumer-driven shifts, focusing on sustainability, purity, and functional application expansion.

1. Sustainable Sourcing and Non-GMO Certification

Consumer and corporate procurement pressure, especially in North America and Europe, demands greater transparency regarding the fermentation feedstock.

Non-GMO Mandate: There is increasing demand for CA produced from Non-GMO (Genetically Modified Organism) corn or alternative substrates like cassava and beet molasses. This premium requirement allows manufacturers to differentiate their product and command a higher price point in developed markets.

Waste-to-Acid: Innovation focuses on using industrial byproducts or agricultural waste (e.g., potato peel, brewery waste) as sustainable and low-cost substrates for Aspergillus niger fermentation, addressing both cost and environmental footprint.

2. Functional Expansion in Pharmaceutical and Nutraceuticals

CA is moving beyond its traditional role as a simple pH adjuster in pharmaceuticals.

Effervescence Technology: The demand for effervescent dosage forms (tablets, powders) is surging in the nutraceutical space (e.g., vitamin supplements, rehydration salts), where CA reacts with bicarbonate to release carbon dioxide, enhancing delivery and patient compliance.

Controlled Release: CA and its esters are being incorporated into drug formulations to control the dissolution rate and stability of active pharmaceutical ingredients ($\text{API}$s).

3. The Shift to Bio-Chelation

In industrial cleaning, water treatment, and textile processing, CA is capitalizing on its superior environmental profile.

Phosphate Substitution: Regulations banning or restricting phosphates in detergents and cleaning agents have created a stable, high-volume substitution opportunity for CA derivatives, which are readily biodegradable and highly effective at softening water and binding metal ions. This trend provides structural, long-term demand stability outside the cyclical F&B sector.

4. Continuous Process Optimization

Manufacturers are adopting advanced fermentation technology and data analytics to optimize the Aspergillus niger bioprocess. This includes the use of AI and machine learning to monitor fermentation tank conditions (temperature, pH, nutrient feed rate) in real-time, improving yields, reducing contamination risk, and lowering overall energy consumption per unit of CA produced.

Competitive Landscape

The Citric Acid Market is characterized as an oligopoly, dominated by a few global players who control significant production capacity and possess the necessary technical expertise for fermentation and purification.

Major Global Players

Cofco Biochemical (China): A massive, state-backed enterprise that leverages vast, cost-effective raw material supply (corn) and scale to be a global price setter and the largest producer

by volume.

Jungbunzlauer Suisse AG (Switzerland/Austria): Known for its high-quality, specialized CA and citrate derivatives, particularly targeting the European and North American F&B and pharmaceutical markets. Competes on quality, non-GMO sourcing, and vertical integration.

Archer Daniels Midland (ADM) (USA): A major agricultural processing giant that utilizes its vast corn and sweetener business to maintain a strong position, primarily serving the North American beverage and food industries.

RZBC Group (China): Another large Chinese producer contributing significantly to global supply, focusing on mass production and competitive pricing.

Competitive Strategies and Market Share

Cost Leadership (Chinese Producers): The primary strategy for Asian giants is leveraging economies of scale, low-cost labor, and government support to offer the lowest ex-factory prices, often leading to global oversupply and margin pressure.

Product Differentiation (Western Producers): Companies like Jungbunzlauer compete by prioritizing security of supply, specialized grades (e.g., highly purified FCC grade for pharma), and certifications (e.g., Non-GMO, Halal, Kosher), allowing them to operate in premium, less price-sensitive niches.

Vertical Integration: Successful players, particularly those with an agricultural base (ADM, Cofco), benefit from owning the raw material supply chain, providing a hedge against input price volatility—a critical strategic advantage.

Regional Insights

Market demand and supply dynamics are geographically distinct, with production heavily centralized but consumption globally dispersed.

Asia-Pacific (APAC) – The Production Hub and Growth Driver

Market Share: APAC hosts the majority of global production capacity and is simultaneously the fastest-growing consumption market.

Dynamics: Driven by rising disposable incomes, rapid urbanization, and the corresponding boom in packaged foods and soft drinks across India, China, and Southeast Asia. The region dictates global CA price benchmarks.

Opportunity: High-growth investment in non-food sectors, particularly detergents and institutional cleaning, as regulatory standards improve in emerging APAC nations.

North America (NA) and Europe (EU) – Mature and Quality-Focused

Market Share: Mature consumption markets with stable, but slower, volume growth.

Dynamics: Characterized by strict regulatory requirements, high demand for CA derivatives (e.g., triethyl citrate, sodium citrate), and a pronounced preference for Non-GMO certified and sustainably produced ingredients. Pricing power is higher here for specialized grades.

Opportunity: Significant demand for CA as a pharmaceutical excipient and for use in regulated cleaning products (chelation).

Latin America (LATAM) and Middle East & Africa (MEA)

Dynamics: These are high-potential emerging markets, heavily driven by the beverage industry (juice, soft drinks). LATAM, leveraging its sugar production, could see localized production increases. MEA growth is linked to population expansion and infrastructure development, boosting demand for both F&B and industrial cleaners.

Challenges & Risks

The stability of the CA market is constantly tested by supply-side volatility and trade complexities.

1. Raw Material Price Volatility

Since carbohydrate substrates (corn, molasses) account for a significant portion of the production cost, global shifts in agricultural commodity markets—driven by weather, biofuel demand, and government subsidies—directly impact CA profitability. Manufacturers with poor hedging strategies face persistent margin compression risk.

2. Trade Tariffs and Anti-Dumping Duties

The concentration of production capacity in China has led to frequent trade disputes, with countries like the US and the EU periodically imposing anti-dumping duties on imported Chinese CA. These tariffs disrupt global trade flows, forcing buyers to seek higher-priced, alternative suppliers and injecting uncertainty into long-term procurement planning.

3. Energy Intensity of Production

The fermentation, crystallization, and purification processes are highly energy-intensive. Fluctuations in global oil and gas prices (which affect manufacturing energy and logistics costs) can sharply increase operating expenses, especially for facilities reliant on fossil fuels, posing a challenge to sustainability targets.

4. Threat from Alternatives

While CA is highly versatile, it faces competition from other organic acids in specific applications: malic and fumaric acid in fruit-flavored products (due to their unique flavor profiles) and lactic acid in dairy. Consistent quality and competitive pricing are essential to prevent substitution.

Opportunities & Strategic Recommendations

1. Optimize Non-Food Segment Penetration

Recommendation: Aggressively target and invest in the high-growth, high-margin pharmaceutical and industrial sectors.

Action: Develop specialty, ultra-pure CA and citrate derivatives (e.g., high-purity triethyl citrate for plasticizers; USP/FCC grades) that command a 20-40% price premium over food-grade commodity CA. Focus R&D on applications in bio-polymers and advanced API stabilization.

2. Secure and Diversify Feedstock Supply

Recommendation: Mitigate raw material and geopolitical risk by securing multi-source, long-term contracts for alternative, non-GMO feedstocks.

Action: Establish production partnerships or facilities in regions with stable, locally sourced sugar or molasses (e.g., Brazil, India, Thailand). This strategy insulates the supply chain from corn-driven commodity spikes and reduces exposure to single-country trade policies.

3. Embrace Sustainability and Traceability

Recommendation: Use environmental credentials as a competitive differentiator in developed markets.

Action: Invest in ISO 50001 energy management systems and transition to lower-emission production methods. Obtain and actively market Non-GMO, Organic, and sustainability certifications (e.g., using waste-derived substrates) to meet sophisticated corporate procurement mandates in Europe and North America.

4. Digitalize the Supply Chain

Recommendation: Implement real-time data analytics and integrated supply chain software to manage global inventory and procurement efficiently.

Action: Use predictive modeling to anticipate raw material price fluctuations (corn/sugar futures) and optimize production schedules, reducing the need for costly, reactive stock management and ensuring consistent delivery quality globally.

Browse More Reports:

Global Small Molecule Sterile Injectable Drugs Market

Europe IoT Node and Gateway Market

Global Ophthalmic Anesthetic Drugs Market

Global Sustainable Aviation Fuel Market

North America Acute Lymphocytic/Lymphoblastic Leukemia (ALL) Diagnostics Market

Global Polymeric Nanoparticles Market

Global Acrylic Adhesives Market

Global Washing Appliances Market

Global Public Key Infrastructure (PKI) Market

Global GPS (Global Positioning System) Tracking System Market

North America Unmanned Ground Vehicle Market

North America Biometrics in Government Market

Global Gas Turbine Services Market

Global Energy Efficient Motor Market

Global Two Terminal Impact (Impact Ionization Avalanche Transit-Time) Diode Market

Global Antivirus Software Market

Middle East and Africa Polyimide films Market

Global Gene Expression Analysis Market

Global Genetic Testing Market

Global Food Ingredient Market

Global Ultra Soft Exoskeleton Market

Global Supercapacitor Market

Global Industrial Nitrogen Market

Global Mono-Material Packaging Market

Global Hematology Drugs Market

Global Polyethylene Implants Market

Global Dental Devices and Consumables Market

Global Ear Plugs and Bands Market

North America Commercial Cleaning Equipment Market

Global Rice Husk Ash Market

Global Data Integration Market

About Data Bridge Market Research:

An absolute way to forecast what the future holds is to comprehend the trend today!

Data Bridge Market Research set forth itself as an unconventional and neoteric market research and consulting firm with an unparalleled level of resilience and integrated approaches. We are determined to unearth the best market opportunities and foster efficient information for your business to thrive in the market. Data Bridge endeavors to provide appropriate solutions to the complex business challenges and initiates an effortless decision-making process. Data Bridge is an aftermath of sheer wisdom and experience which was formulated and framed in the year 2015 in Pune.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email:- corporatesales@databridgemarketresearch.com