Executive Summary

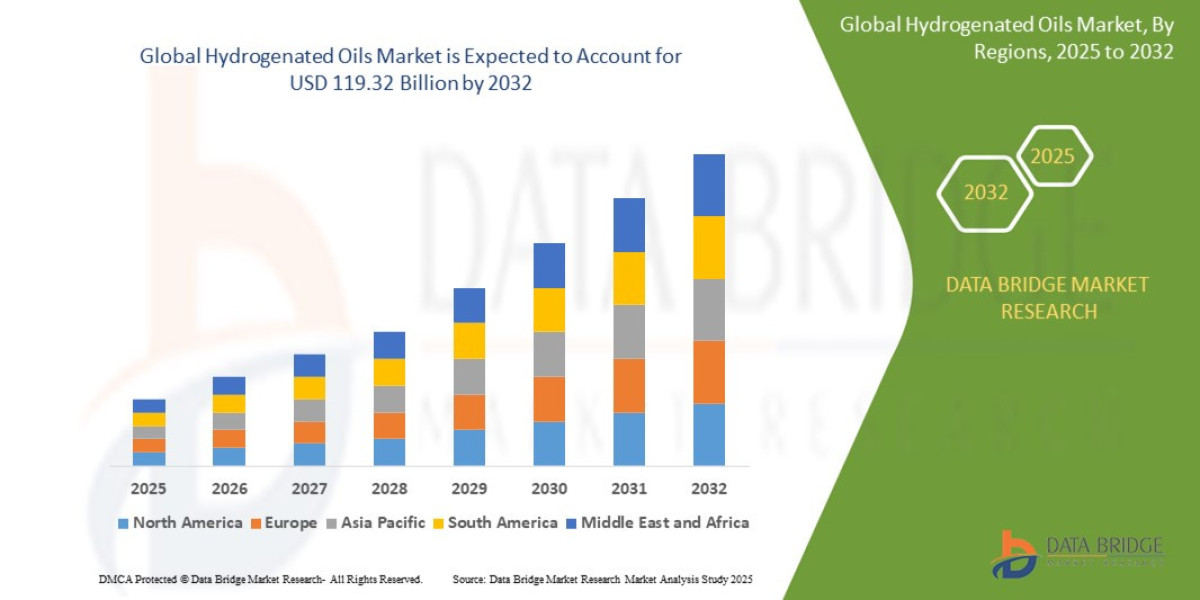

- The global hydrogenated oils market was valued at USD 85.20 billion in 2024 and is expected to reach USD 119.32 billion by 2032

- During the forecast period of 2025 to 2032 the market is likely to grow at a CAGR of 4.30%,

Market Overview

Hydrogenated oils are fats derived primarily from vegetable oils (soybean, palm, rapeseed, sunflower) or, less commonly, animal fats, which undergo a chemical process called hydrogenation. This process adds hydrogen atoms to unsaturated fatty acids, increasing the melting point, oxidative stability, and plasticity of the oil, converting it from liquid to semi-solid or solid fat.

The market is broadly defined by its primary end-use segments:

Food & Beverage (Traditional HO): Used extensively in bakery (shortening, dough conditioning), confectionery, frying fats, and margarine to improve texture, mouthfeel, and extend shelf life.

Industrial & Biofuel (Hydrotreated Vegetable Oil - HVO): A rapidly emerging segment where hydrogenated oils are hydrotreated to produce high-quality, renewable diesel fuel and Sustainable Aviation Fuel (SAF).

Personal Care & Cosmetics: Utilized as emollients, thickening agents, and structuring components in products like lip balms, lotions, and creams, driven by the clean-label and natural ingredients movement.

The current market dynamic is characterized by a dichotomy: the decline of PHOs (due to trans fat bans) is offset by the surging popularity of FHOs (Fully Hydrogenated Oils), which contain negligible trans fats and serve as feedstock for healthier fat alternatives, and the massive scale-up of HVO for energy production. Asia-Pacific currently dominates the revenue share, owing to its vast food processing infrastructure and high consumption of processed and ready-to-eat foods.

Market Size & Forecast

- The global hydrogenated oils market was valued at USD 85.20 billion in 2024 and is expected to reach USD 119.32 billion by 2032

- During the forecast period of 2025 to 2032 the market is likely to grow at a CAGR of 4.30%,

For More Information visit https://www.databridgemarketresearch.com/reports/global-hydrogenated-oils-market

Key Trends & Innovations

The market is defined by several converging trends, requiring manufacturers to rapidly shift production paradigms:

The Shift to Zero Trans-Fat Formulations

The most significant trend is the global regulatory elimination of PHOs, forcing manufacturers to adopt non-PHO hydrogenation methods. The industry has largely pivoted to Fully Hydrogenated Oils (FHOs), which are solid fats (saturated) containing virtually no trans fats. FHOs are then frequently combined with other processes:

Interesterification: This enzymatic or chemical process rearranges the fatty acid structure of the FHO and a liquid oil, producing a structured fat with desirable texture and plasticity, crucial for margarines and shortenings, without the creation of trans fats. This is now the default method for producing high-functionality, trans-fat-free solid fats.

Fractionation: This physical separation process of oils (often palm oil) yields fractions with specific melting points, reducing the reliance on extensive chemical modification. The fast-growing demand for high-purity fractionated HVO in the specialty chemical and cosmetic sectors underscores its importance.

Renewable Diesel & Sustainable Aviation Fuel (SAF)

The industrial application of hydrogenated oils, specifically Hydrotreated Vegetable Oil (HVO), has become the single largest growth driver. HVO, often derived from used cooking oil (UCO), animal fats, or dedicated oil crops, is chemically identical to petroleum diesel (renewable diesel) but significantly reduces carbon emissions (up to 90%).

Drop-in Fuel Capability: HVO is a "drop-in" fuel, meaning it requires no modification to existing diesel engines or distribution infrastructure, accelerating its adoption by the automotive, marine, and aviation sectors.

Regulatory Backing: Government policies, such as the EU Green Deal and the U.S. Renewable Fuel Standard and Low Carbon Fuel Standards, provide powerful financial incentives and mandates that guarantee long-term demand for HVO feedstock.

Sustainable and Traceable Sourcing

Consumer and corporate focus on Environmental, Social, and Governance (ESG) standards is pushing the market toward certified sustainable palm oil and increased utilization of waste feedstocks, such as UCO and tallow. Manufacturers are investing heavily in supply chain transparency to meet demands for eco-friendly and ethically sourced ingredients.

Competitive Landscape

The hydrogenated oils market is highly consolidated yet diverse, featuring multinational agricultural and food processing giants, alongside specialized oleochemical and energy companies.

Major Global Players: The competitive environment is dominated by major integrated agricultural commodity traders and processors who control the upstream supply of crude vegetable oils. Key players include:

Cargill Incorporated: A global leader in food ingredients, focusing on low-trans and non-hydrogenated shortening and functional fats for the food service and food manufacturing sectors.

Bunge Limited: A key supplier of edible oils, actively investing in trans-fat-free solutions and renewable energy feedstocks.

Wilmar International Ltd: Dominant in the Asia-Pacific region, with vast capacities in palm oil processing and hydrogenation for both edible and industrial applications.

AAK AB: A specialty oil and fat supplier known for tailored solutions, focusing on high-value fractionated products for confectionery and cosmetics.

Archer Daniels Midland (ADM): Leveraging its extensive crop processing capabilities to supply diverse HO products and move into the biofuel feedstock market.

Emerging Industrial Competitors (HVO/Biofuels): The high-growth industrial sector features energy giants and specialized biofuel producers:

Neste: A global leader in renewable diesel (HVO), focusing on securing diverse waste and residue feedstocks (UCO, animal fat).

TotalEnergies and Shell: Investing heavily in co-processing facilities to blend vegetable oils with fossil fuels to meet energy mandates.

Competitive Strategies: The primary competitive strategies revolve around vertical integration (controlling the supply chain from farm to finished product), technological differentiation (mastering interesterification and fractionation for trans-fat-free solutions), and geographic expansion, particularly targeting the burgeoning markets of Asia-Pacific. Furthermore, long-term supply agreements in the industrial sector, such as those made by biofuel producers to secure UCO feedstock, are crucial for competitive advantage.

Regional Insights

Market performance and growth drivers vary significantly across global regions, reflecting diverse regulatory frameworks and consumption patterns.

Asia-Pacific (APAC): The Growth Engine

APAC commands the largest market share (over 38%), driven by its massive, rapidly expanding food processing sector and accelerating urbanization. Countries like China, India, and Indonesia are experiencing a sustained increase in the consumption of packaged snacks, ready-to-eat meals, and confectionery, which heavily utilize hydrogenated fats for cost-effectiveness and stability.

Opportunity: While enforcement of trans-fat restrictions (like India's mandate to limit trans fats to 2% in fats and oils) is challenging, the sheer volume of consumption provides immense opportunities for suppliers of trans-fat-compliant FHOs and shortening. The region is also becoming a critical hub for the sourcing and export of UCO, a primary HVO feedstock.

North America & Europe: Regulatory Compliance and Premiumization

These regions are characterized by mature markets, strict regulatory adherence (PHOs are essentially banned), and a strong consumer demand for health-conscious and sustainable products.

Trend: The market here is focused on premium, specialty fats tailored for specific functional needs (e.g., high-stability frying oils, non-dairy creamers). Growth is driven almost entirely by the industrial sector, as European nations, in particular, lead global adoption of HVO for transport and marine fuel. Europe accounted for a dominant share of the Hydrotreated Vegetable Oil market in 2024.

Latin America, Middle East & Africa (LAMEA): Emerging Adoption

LAMEA represents a high-potential market. While regulatory enforcement is inconsistent, rising disposable incomes and shifts toward modern retailing and processed foods are fueling demand.

Focus: Manufacturers are targeting this region for the adoption of basic, cost-effective FHOs in food production while laying the groundwork for future industrial HVO projects tied to regional energy goals.

Challenges & Risks

The hydrogenated oils market faces several complex risks that require continuous management and technological agility.

Regulatory Constraint and Reputation Risk

The most persistent challenge is the global ban on industrially produced trans fat derived from PHOs. Although most major producers have reformulated, the residual association of hydrogenated fats with poor health outcomes creates a significant reputational risk. Any perceived failure in compliance or labeling can lead to consumer boycotts and regulatory penalties. The challenge lies not only in reformulation but in ensuring compliance among smaller, regional food manufacturers, particularly in developing nations.

Feedstock Volatility and Sustainability

Hydrogenated oil production is reliant on high-volume vegetable oils (palm, soybean, rapeseed). Price volatility in these commodities, driven by geopolitical events, climate change impacts on crop yields, and evolving trade policies, directly affects production costs and margins. Furthermore, the increasing use of these oils in the highly subsidized biofuel sector creates a fierce "food vs. fuel" dynamic, driving up feedstock prices for food and cosmetic manufacturers. Sourcing palm oil sustainably also remains a significant environmental and public relations challenge.

Competition from Novel Fats

The market faces intense competition from innovative, non-hydrogenated alternatives, including:

Non-Hydrogenated Shortenings: Using advanced blending and crystallization techniques to achieve desirable textures.

Algae-Based Oils and Single-Cell Oils: Next-generation fats that offer superior nutritional profiles and functional properties without chemical modification.

Structured Triglycerides (STG): Custom-designed fats for highly specific applications, often preferred in premium food segments.

Opportunities & Strategic Recommendations

The transformation of the hydrogenated oils market presents lucrative opportunities for stakeholders who pivot strategically toward innovation and industrial integration.

1. Capitalize on the Biofuel/Industrial Mega-Trend

Recommendation: Manufacturers should aggressively pursue vertical integration and strategic partnerships to secure and diversify their industrial HVO feedstock. Investment should focus on:

Waste Stream Processing: Establishing robust, geographically distributed supply chains for used cooking oil (UCO) and animal fats, which are highly valued feedstocks with strong regulatory support.

Advanced Biorefinery Development: Shifting capital expenditure toward facilities that can hydrotreat oils for renewable diesel, offering higher margins and insulated demand compared to the volatile food ingredients sector.

2. Master Trans-Fat-Free Functional Fats

Recommendation: For the food segment, competitive advantage hinges on mastering enzymatic interesterification and advanced fractionation. Companies must invest in R&D to create customizable, trans-fat-free structured fats that precisely mimic the functionality of traditional shortenings, focusing on:

Specialty Bakery Fats: Developing non-PHO shortenings with specific crystallization profiles for laminated dough, high-ratio cakes, and stable icings.

Clean Label Solutions: Offering fractionated, minimal-processing oils for the personal care and cosmetic sectors, leveraging the Fractionated segment’s 7%+ CAGR.

3. Expand in High-Growth APAC and Emerging Markets

Recommendation: Focus market expansion on the burgeoning Asia-Pacific region. While the regulatory environment is complex, the sheer scale of the food processing industry guarantees high volume.

Local Compliance Models: Develop region-specific product lines (e.g., affordable, high-stability FHOs for the Indian and Southeast Asian markets) that meet local 2% trans-fat limits while providing cost-effective alternatives to traditional vanaspati and shortenings.

4. Leverage Sustainable and Traceable Sourcing

Recommendation: Implement blockchain or similar digital ledger technologies for end-to-end transparency of feedstock origin, moving beyond basic certification.

Product Differentiation: Market products not just on functional attributes but on their carbon footprint reduction (for HVO) or their adherence to zero-deforestation policies (for palm oil). This acts as a powerful differentiator for B2B customers facing their own ESG pressures.

Browse More Reports:

Middle East and Africa Digital Farming Software Market

Global Specialty Lancets Market

Asia-Pacific Medical Imaging (3D and 4D) Software Market

Global Flat Panel Detector (FPD)-Based X-Ray for Cone Beam Computed Tomography (CBCT) Market

Global Soy Protein Market

Asia-Pacific Botanical Extract Market

Europe Laminated Busbar Market

Global Moisture Analyser Market

Asia-Pacific Indium Market

Global Feather Meal Market

Global Protein Hydrolysates Market

Global X Linked Hypophosphatemia (XLH) Treatment Market

Global Musculoskeletal Disorders Drugs Market

Global Spinal Stenosis Treatment Market

Asia-Pacific Flotation Reagents Market

France Artificial Turf Market

Global Cardiovascular Genetic Testing Market

Global Brass Solenoid Valves Market

North America Medical Imaging (3D and 4D) Software Market

Global Flexible Insulation Market

Global Drug Eluting Stents (DES) Market

Middle East and Africa Ostomy Devices Market

Global Specialty Yeast Market

Global Automotive Blind Spot Detection System Market

Global Textile Fabric Market

Global Chemical Market

Global 3D Printed Jewelry Market

Global Jamestown Canyon Virus Treatment Market

Europe Botanical Extract Market

Global Cloud Applications Market

Global Plant Based Protein Market

Global Prosthetic Disc Nucleus Market

About Data Bridge Market Research:

An absolute way to forecast what the future holds is to comprehend the trend today!

Data Bridge Market Research set forth itself as an unconventional and neoteric market research and consulting firm with an unparalleled level of resilience and integrated approaches. We are determined to unearth the best market opportunities and foster efficient information for your business to thrive in the market. Data Bridge endeavors to provide appropriate solutions to the complex business challenges and initiates an effortless decision-making process. Data Bridge is an aftermath of sheer wisdom and experience which was formulated and framed in the year 2015 in Pune.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email:- corporatesales@databridgemarketresearch.com