Executive Summary

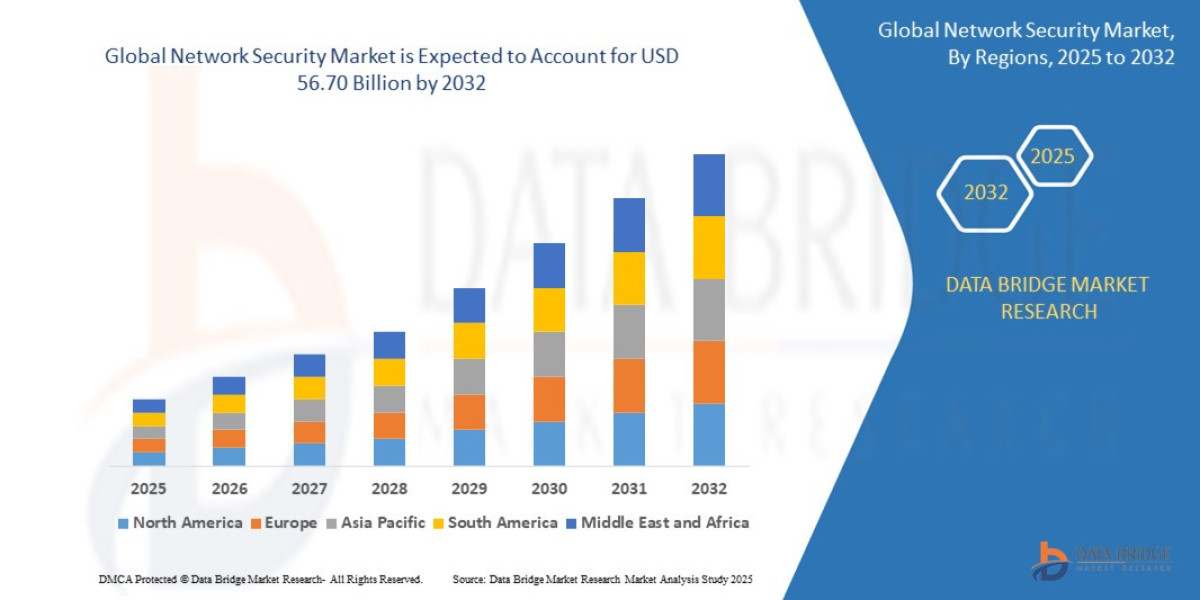

- The global Network Security market was valued at USD 22.90 billion in 2024 and is expected to reach USD 56.70 billion by 2032

- During the forecast period of 2025 to 2032 the market is such as to grow at a CAGR of 12%,

Market Overview

The Network Security Market encompasses the hardware, software, and services designed to protect the integrity, confidentiality, and accessibility of computer networks and data. Historically focused on traditional firewalls and Intrusion Prevention Systems (IPS) defending a clear corporate boundary, the modern market has expanded to secure highly distributed environments, including multi-cloud, remote workforces, and vast IoT landscapes.

Key Segments

The market can be segmented across several critical dimensions:

By Component:

Solutions (Dominant Share): Includes core technologies like Firewalls (Next-Generation Firewalls, NGFW), Antivirus/Anti-Malware, Network Access Control (NAC), Data Loss Prevention (DLP), IDS/IPS, and Unified Threat Management (UTM). The Firewall segment remains the primary defense mechanism, accounting for over 55.6% of the market share.

Services (Fastest Growth): Encompasses professional services (consulting, implementation) and, most importantly, Managed Security Service Providers (MSSPs). Services are projected to see the fastest growth, driven by the talent shortage and the complexity of 24/7 threat monitoring.

By Deployment:

Cloud (Highest CAGR): Cloud-based solutions (including Security-as-a-Service) offer scalability, flexibility, and cost efficiency, leading to the highest projected CAGR. This segment is displacing legacy on-premise solutions.

On-Premise: Solutions hosted locally, still preferred by large enterprises in heavily regulated sectors (like certain government and financial operations) requiring maximum control over data residency.

By Enterprise Type: Large Enterprises currently hold the largest market share due to larger budgets and higher regulatory burdens, but Small and Medium Enterprises (SMEs) are expected to show the fastest CAGR (around 14.4%), fueled by accessible subscription-based, cloud-delivered security models.

By Industry Vertical: The Banking, Financial Services, and Insurance (BFSI) sector holds the largest revenue share (over 20.0%) due to stringent regulatory compliance (e.g., PCI-DSS), while the Healthcare vertical is projected to log the highest CAGR (around 15.8%) as clinical digitization and telemedicine rapidly expand the attack surface.

Key Market Drivers and Current Dynamics

Escalating Threat Sophistication: The rise of Ransomware-as-a-Service (RaaS) and the weaponization of Artificial Intelligence (AI) by threat actors necessitate faster, automated, and more predictive defense mechanisms.

Rapid Cloud Migration and Hybrid Work: The shift to cloud infrastructure and the persistence of hybrid work models have rendered traditional perimeter security obsolete, fueling the demand for ZTA and cloud-native protection.

IoT and OT Proliferation: Billions of connected Industrial IoT (IIoT) devices in smart manufacturing and critical infrastructure introduce massive, difficult-to-patch attack surfaces, requiring advanced network segmentation and micro-segmentation capabilities.

Stricter Regulatory Compliance: Global mandates like the GDPR, CCPA, and industry-specific rules (e.g., HIPAA) impose heavy fines for data breaches, compelling businesses to invest continuously in robust DLP and network monitoring.

Market Size & Forecast

- The global Network Security market was valued at USD 22.90 billion in 2024 and is expected to reach USD 56.70 billion by 2032

- During the forecast period of 2025 to 2032 the market is such as to grow at a CAGR of 12%.

For More Information Visit https://www.databridgemarketresearch.com/reports/global-network-security-market

Key Trends & Innovations

The current market is defined by a shift from reactive defense to proactive, platform-based security enforcement.

1. The Ascent of Zero Trust Architecture (ZTA)

ZTA, based on the principle of “never trust, always verify,” is the foundational security model for the modern enterprise. Its adoption is no longer optional but mandatory in hybrid environments. Key ZTA implementations involve:

Micro-segmentation: Isolating workloads and applications across the network to prevent lateral movement of threats.

Continuous Verification: Utilizing Multi-Factor Authentication (MFA) and behavioral analytics to constantly re-verify the identity and integrity of users and devices, regardless of their location.

2. SASE and Security Service Edge (SSE) Convergence

The convergence of network connectivity (SD-WAN) and network security services into a single, cloud-delivered platform is known as Secure Access Service Edge (SASE). The security component, SSE, comprises key services like Zero Trust Network Access (ZTNA), Cloud Access Security Broker (CASB), Secure Web Gateway (SWG), and Firewall-as-a-Service (FWaaS). SSE provides simplified, centralized policy enforcement for the remote workforce, positioning it as one of the most critical trends for vendors and purchasers alike.

3. AI-Driven Automation and Threat Intelligence

AI is a double-edged sword. While attackers use AI to craft sophisticated, personalized phishing campaigns and polymorphic malware, defenders are leveraging it for:

AI-SIEM/SOAR: Automating security operations (SecOps) tasks, correlating vast datasets, and orchestrating rapid incident response—a vital function given the global cybersecurity skills shortage.

Predictive Analytics: Identifying anomalous behaviors (user, device, or network) in real-time to predict and neutralize threats before they execute a payload.

4. Post-Quantum Cryptography (PQC) Preparation

Though quantum computing is not yet mainstream, the threat it poses to current encryption standards (like RSA) is real, especially for sensitive, long-term data (i.e., "Harvest Now, Decrypt Later" attacks). Preparation for quantum-resistant cryptographic standards is moving from academic discussion to an enterprise risk mitigation task.

Competitive Landscape

The network security market is competitive and moderately concentrated, characterized by a mix of established infrastructure giants and agile, cloud-native specialists. Competition is increasingly focused on platform integration and cloud capabilities rather than point products.

Major Players and Strategic Focus

Company | Primary Market Focus | Strategic Moves |

|---|---|---|

Palo Alto Networks | Next-Generation Firewalls (NGFW), Cloud Security (Prisma), Security Operations (Cortex). | Strong focus on unified, platform-based security across all three pillars: Network, Cloud, and SOC. |

Cisco Systems | Integrated Network and Security (NDR), Managed Services. | Leveraging its massive networking infrastructure footprint to embed security solutions deeply into the network fabric (e.g., folding Splunk analytics into its portfolio). |

Fortinet | Unified Threat Management (UTM), Security Fabric, SD-WAN, and SASE. | Highly focused on its integrated security fabric, which spans the entire IT infrastructure, and achieving market leadership in NGFW and SD-WAN. |

Zscaler | Pure-play Cloud Security, Zero Trust Exchange, SSE. | Leading the shift away from network-centric security toward user and application access, emphasizing a cloud-native, zero-trust approach. |

CrowdStrike | Endpoint Detection and Response (EDR) and Cloud Workload Protection (CWPP), expanding into network visibility. | Growing ecosystem focus, using its powerful threat intelligence platform to expand into network and cloud security markets. |

Competitive Strategies

The current competitive environment revolves around consolidation and integration. Vendors are actively pursuing mergers and acquisitions to transition from offering single-function tools to providing comprehensive, unified security platforms (e.g., extended detection and response, XDR). The key battleground is the cloud, where vendors compete to offer seamless security, management, and visibility across multi-cloud and hybrid environments. Price erosion on commodity products like basic firewalls is forcing players to shift revenue toward high-margin, subscription-based cloud services and professional management.

Regional Insights

Market growth is uneven, with specific geographies demonstrating distinct priorities and market maturity.

North America (Dominant Market)

North America, particularly the U.S., commands the largest market share (approximately 37.69%). This dominance is due to:

High IT Maturity: Early and widespread adoption of cloud, mobile, and IoT technologies.

Stringent Regulation: High compliance pressure in BFSI and Government sectors.

Innovation Hub: Home to most major solution providers, leading to rapid adoption of ZTA, SASE, and AI-driven defense mechanisms.

Asia-Pacific (Fastest Growing Market)

The APAC region is projected to be the fastest-growing market, exhibiting a CAGR of over 15.2%.

Digital Transformation: Rapid digital adoption and investment across countries like India, China, and Southeast Asia.

SME Growth: High growth in SMEs, driving demand for scalable, subscription-based cloud security and managed services.

5G Deployment: Mass-scale 5G rollout is accelerating the need for network segmentation and edge security solutions.

Europe (Mature Market with High Compliance)

Europe is characterized by a mature market heavily influenced by the GDPR. Growth is steady, driven primarily by the need for advanced data protection, compliance technology, and the implementation of ZTA to secure geographically dispersed workforces.

Challenges & Risks

Despite its robust growth trajectory, the network security market faces several significant headwinds:

Cybersecurity Skills Shortage: The most critical challenge is the profound global shortage of skilled security professionals. This forces enterprises to rely on expensive external managed services and complex, highly automated AI/ML tools, raising operational costs.

Complexity of Integration: The need to secure hybrid and multi-cloud environments, often involving legacy on-premise infrastructure, results in complex, multi-vendor security stacks that are difficult to manage and often leave dangerous security gaps. Vendor API lock-in further complicates the integration of "best-of-breed" solutions.

High Cost of Next-Gen Infrastructure: The capital expenditure (CapEx) required for next-generation hardware appliances and the specialized expertise needed to deploy advanced platforms can be prohibitive, especially for mid-market and small enterprises.

Evolving AI-Powered Threats: The speed at which AI enables new attack vectors (deepfake phishing, adaptive malware) outpaces the ability of traditional defenses to respond, requiring constant, costly R&D investment from vendors.

Opportunities & Strategic Recommendations

The dynamic nature of the market presents clear opportunities for innovation and investment across the ecosystem.

Opportunities for Growth

Unified Cloud Security (SASE/SSE): The dominant long-term growth opportunity lies in building consolidated SASE platforms that seamlessly integrate ZTNA, CASB, and FWaaS into a single, simple-to-manage cloud service.

OT/IIoT Security: Specialized network security solutions tailored for industrial control systems (ICS) and Operational Technology (OT) are critical. This is a niche, high-value area with less competition from traditional IT security players.

Security Automation and AI-SIEM: Developing automated Security Orchestration, Automation, and Response (SOAR) tools powered by Machine Learning (ML) that can perform triage, threat hunting, and response without human intervention directly addresses the talent gap challenge.

SME Subscription Models: Providing affordable, highly managed, and easily deployable cloud-based security bundles aimed specifically at the fast-growing SME segment, simplifying complex security decisions into cost-effective subscriptions.

Strategic Recommendations for Stakeholders

For Established Vendors: Prioritize the sunsetting of siloed, appliance-based products in favor of a platform-centric, cloud-native architecture. Strategic M&A should focus on acquiring specialized AI/ML and identity management capabilities to enhance XDR offerings.

For Investors/Venture Capital: Focus investment on pure-play SSE vendors and companies specializing in OT security and Post-Quantum Cryptography preparation. Look for solutions that promise genuine simplicity and low operational overhead.

For Enterprise Buyers: Adopt a phased Zero Trust implementation roadmap. Prioritize vendor consolidation around platforms that offer unified policy enforcement across all three domains: network, cloud, and identity. Leverage Managed Security Services (MSS) to manage the operational burden created by the skills shortage.

Browse More Reports:

Global Lentil Protein Market

Global Plastic Bags & Sacks Market

Middle East and Africa Network Test Lab Automation Market

Global Tricalcium Citrate Market

Global Dough Concentrates Market

Global Fusion Splicer Market

Europe Polyimide Films Market

Global Gorlin Syndrome Market

Europe Hand Holes Market

Global Trichoderma Viride Biofungicides Market

Asia-Pacific Digital Farming Software Market

North America Intensive Care Unit (ICU) Ventilators Market

Asia-Pacific Plant-Based Milk Market

Global Robotic Vision Market

Middle East and Africa Specialty Gas Market

Global Footwear Market

Global Chaple Syndrome Market

Global Topical Corticosteroids Market

Global Vitamin E for Food Application Market

Global Consumer Appliances Market

Global Enterprise Information Archiving Market

Global Aircraft Nacelle Market

Global Wind Turbine Casting Market

Asia-Pacific Flight Data Recorder Market

Global Broadband Services Market

Global Underwater Acoustic Communication Market

Global Fragrance Fixatives Market

Global Vitamin Nutritional Analysis Market

Global Lipid Profile Market

Global Automotive Light-Vehicle Sensors Market

Global Cumene Hydroperoxide Market

Europe Biological Buffers Market

About Data Bridge Market Research:

An absolute way to forecast what the future holds is to comprehend the trend today!

Data Bridge Market Research set forth itself as an unconventional and neoteric market research and consulting firm with an unparalleled level of resilience and integrated approaches. We are determined to unearth the best market opportunities and foster efficient information for your business to thrive in the market. Data Bridge endeavors to provide appropriate solutions to the complex business challenges and initiates an effortless decision-making process. Data Bridge is an aftermath of sheer wisdom and experience which was formulated and framed in the year 2015 in Pune.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email:- corporatesales@databridgemarketresearch.com