Executive Summary

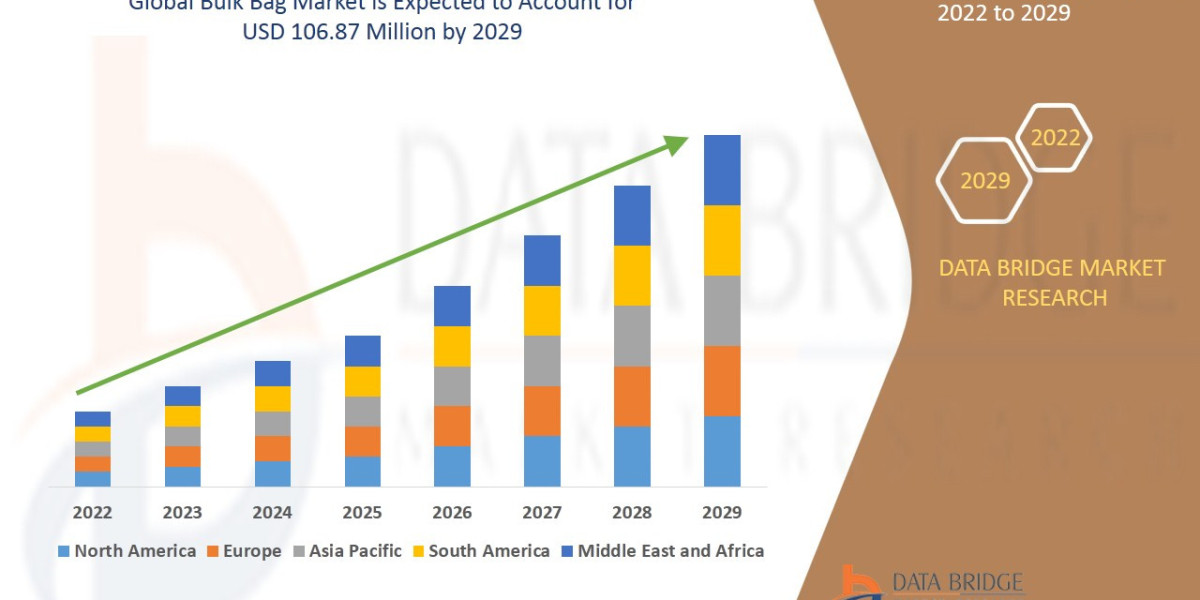

Data Bridge Market Research analyses that the bulk bag market will project a CAGR of 6.20% for the forecast period of 2022-2029 and is expected to reach the USD 106.87 million by 2029.

Market Overview

Defining Flexible Intermediate Bulk Containers (FIBCs)

Bulk bags, or FIBCs, are large, woven polypropylene containers designed for storing and transporting dry, flowable materials in bulk, typically ranging in capacity from 500 to 4,000 pounds (approximately 250 to 1,800 kilograms). Their fundamental appeal lies in their cost-efficiency, lightweight nature, and versatility, allowing for easy handling by forklifts without the need for traditional pallets, which significantly reduces logistics costs and storage footprint.

Key Market Segmentation

The FIBC market is highly segmented based on performance, design, and application:

Segmentation Category | Leading Segments | Application Insight |

|---|---|---|

Fabric Type (Safety) | Type C (Conductive) and Type D (Static Dissipative) | Critical for handling flammable powders and operating in explosive environments (chemicals, pharmaceuticals). Type A (standard) dominates general use. |

Design | U-Panel, Baffle Bags (Q-Bags) | Baffle bags are the best solution for retaining a square shape when filled, optimizing container space, and minimizing shipping costs. |

Capacity | Medium (0.75-1.5 cu. m) and Large (Above 1.5 cu. m) | Large bags are dominant in construction and mining; medium bags are preferred for general-purpose chemical and agricultural products. |

End-Use Industry | Chemicals & Fertilizers, Construction, Agriculture | These three sectors account for the majority of global FIBC consumption due to the high volume of bulk materials handled. |

Market Drivers and Current Dynamics

Expansion of Global Trade and Logistics: The continuous growth in international trade volumes, particularly across Asia Pacific and emerging economies, necessitates cost-effective and efficient containerization solutions, driving demand for FIBCs.

Robust Growth in End-Use Sectors: Rapid urbanization and infrastructure projects fuel the demand for bulk bags to transport cement, sand, gravel, and other building materials. Simultaneously, modern agricultural practices rely on FIBCs for efficient handling of seeds, grains, and high-volume fertilizers.

Cost-Efficiency: Bulk bags offer lower packaging costs per unit weight compared to alternative rigid containers, making them a budget-friendly option for high-volume producers.

Technological Advancements in Manufacturing: Innovations in weaving and coating technologies have led to the production of stronger, lighter, and more specialized bags with enhanced barrier properties against moisture and contamination.

Market Size & Forecast

Data Bridge Market Research analyses that the bulk bag market will project a CAGR of 6.20% for the forecast period of 2022-2029 and is expected to reach the USD 106.87 million by 2029.

For More information visit https://www.databridgemarketresearch.com/reports/global-bulk-bag-market

Key Trends & Innovations

The future of the Bulk Bag Market is defined by convergence of material science, digital integration, and circular economy principles.

1. The Sustainability Imperative

The most significant trend is the shift toward environmentally friendly packaging, driven by consumer preference and stringent regulatory bodies (such as the EU Green Deal).

Recycled Materials (rPET): Manufacturers are increasingly integrating recycled polyethylene terephthalate (rPET) and post-consumer recycled (PCR) polypropylene into bag construction. This innovation allows companies to meet sustainability mandates without compromising the structural integrity or performance required for heavy-duty applications.

Multi-Trip and Reusable Designs: Programs promoting multi-trip bulk bags are gaining traction, moving away from single-use models. These bags are manufactured to higher safety factors (e.g., $6:1$ SF) and come with tracking systems to monitor their lifecycle and compliance, drastically reducing waste.

Biodegradable Polymers: Although currently a niche segment, research into biodegradable and compostable polymers for FIBC manufacturing presents a long-term opportunity to address the market’s reliance on conventional plastics.

2. Smart Packaging and Digital Integration

Adoption of Industry 4.0 principles is making bulk bags "smart," transforming them from simple containers into data carriers.

RFID and IoT Sensors: Embedding Radio-Frequency Identification (RFID) tags and Internet of Things (IoT) sensors is becoming standard in high-value logistics chains, particularly in North America and Europe. These devices enable real-time tracking of location, internal temperature, humidity, and shock exposure. This enhances supply chain visibility, improves inventory management, and ensures product integrity for sensitive goods like pharmaceuticals and specialty chemicals.

Tamper-Proof and Anti-Counterfeiting: Innovations in sealing, advanced labels, and secure tracking mechanisms are being developed to prevent product adulteration and counterfeiting, particularly crucial in the food and pharmaceutical segments.

3. Enhanced Safety and Compliance

Safety standards for FIBCs continue to rise, particularly concerning electrostatic hazards.

Advanced Static Protection: Type C (conductive) and Type D (dissipative) bags are seeing accelerated adoption. Type D bags, which safely dissipate static charge without the need for physical grounding, are highly valued in automated and high-throughput production environments where human error in grounding is a risk.

Anti-Microbial and Food-Grade Liners: Growing demand for sterile packaging in the food, beverage, and pharmaceutical industries is pushing the development of advanced liners with anti-microbial coatings and high-barrier films that comply with FDA and HACCP standards.

Competitive Landscape

The Bulk Bag Market is characterized by the presence of a few global giants and numerous regional specialists, leading to a moderately competitive environment.

Major Global Players

Leading the market are established multinational corporations with extensive manufacturing footprints and diversified packaging portfolios. Key global players include:

Greif, Inc.

Berry Global Group, Inc.

Mondi Group

Conitex Sonoco

LC Packaging International BV

Competitive Strategies and Recent Developments

Competition revolves around three core strategic pillars:

Capacity and Global Reach: Major players are continuously expanding capacity, often through mergers and acquisitions or greenfield expansions in high-growth regions like Asia and Eastern Europe. For instance, recent developments show companies expanding manufacturing in Vietnam and India to diversify supply chains and capture local demand.

Sustainability Investment: Companies are differentiating themselves by launching new product lines, such as Mondi Group’s EcoAdvantage series, which utilizes high percentages of recycled material. This focus is a necessary competitive response to market demand.

Specialty Product Innovation: Focusing on high-margin, specialized FIBCs—like pharma-grade clean room bags, explosion-proof Type D bags, or custom bulk bag discharger systems (e.g., Flexicon and Spiroflow advancements)—allows companies to capture niche markets and command premium pricing.

The market remains dynamic, with regional manufacturers leveraging cost-competitive production and localized supply chains to challenge the global leaders.

Regional Insights

Asia Pacific (APAC): The Growth Engine

The APAC region is the undisputed leader in the Bulk Bag Market, accounting for an estimated 40-45% of the global revenue share.

Drivers: Rapid industrialization, massive infrastructure investment (especially in China and India), and the region's status as a global manufacturing and chemical production hub fuel colossal demand. The agriculture sector also plays a vital role.

Opportunity: The increasing adoption of higher safety standards (Type C and Type D) in emerging APAC markets presents a significant upselling opportunity for specialized manufacturers.

North America: Automation and High Standards

North America holds a substantial market share and is expected to exhibit strong growth, driven by advanced logistics and stringent safety regulations.

Drivers: High demand from the chemical, food, and pharmaceutical industries, coupled with a focus on automation in warehousing and material handling.

Trends: North America leads in the adoption of smart packaging (RFID) and high-performance safety bags, reflecting a willingness to invest in technology to improve operational efficiency and compliance.

Europe: Sustainability and Regulation

Europe’s market growth is moderate but heavily influenced by environmental policy.

Drivers: Strong manufacturing base, particularly in specialty chemicals. The market is primarily driven by regulatory compliance, particularly the EU Green Deal and the Circular Economy Action Plan.

Focus: European demand is heavily skewed toward multi-trip bags and those manufactured with high recycled content, making it a critical proving ground for sustainable packaging innovations.

Challenges & Risks

While the market outlook is positive, several structural and external risks require careful management.

1. Raw Material Price Volatility

The primary raw material for bulk bags is polypropylene (PP), a petroleum derivative. Fluctuations in crude oil prices directly impact the production cost of woven PP fabric. This volatility makes long-term pricing and inventory management challenging for manufacturers and increases instability across the supply chain.

2. Environmental Scrutiny and Single-Use Plastics

Despite advances in recyclability, a large portion of bulk bags are still used as single-use containers. Increasing public and regulatory pressure on single-use plastics poses a systemic risk. While multi-trip bags offer a solution, end-users must invest in dedicated washing, inspection, and tracking programs, which can be an operational barrier to adoption.

3. Competition from Alternatives

In certain applications, FIBCs face competition from traditional or specialized alternatives, including:

Drums and Rigid IBCs (Intermediate Bulk Containers): Preferred in liquid-handling and specialized chemical/pharmaceutical contexts where absolute product integrity or pressure resistance is necessary.

Paper-Based Sacks: Still used for smaller volumes of materials like cement or powdered ingredients, often preferred for their ease of disposal in certain regions.

4. Handling and Safety Limitations

Bulk bags are susceptible to handling errors, including potential tearing during lifting or puncture if handled roughly. Improper storage can lead to moisture intrusion, while incorrect usage of the anti-static bag types can result in catastrophic static discharge events, especially when handling flammable materials. Mitigating these risks requires continuous end-user training and strict regulatory adherence.

Opportunities & Strategic Recommendations

Opportunities

High-Barrier Food and Pharma Segments: The fastest-growing niche is in the production of high-specification, contamination-free bulk bags for the food (food-grade FIBCs, BRC certified) and pharmaceutical sectors (clean-room manufacturing). These segments offer higher margins and greater stability than commodity-grade bags.

Service and Digitalization: Offering end-to-end services, such as specialized bulk bag filling/discharging systems, automated washing and refurbishment programs for reusable bags, and integrated IoT/tracking data services, can transform manufacturers into full-service logistics partners, creating recurring revenue streams.

Nearshoring and Supply Chain Resiliency: Geopolitical risks and the desire for shorter lead times are encouraging end-users in North America and Europe to seek more resilient supply chains. Investing in localized or near-shored production facilities can capture premium contracts from companies seeking to reduce reliance on distant manufacturing hubs.

Strategic Recommendations

Stakeholder | Strategic Guidance |

|---|---|

Manufacturers | Prioritize R&D in Materials: Invest heavily in developing and commercializing rPET-based FIBCs and next-generation barrier coatings to meet impending sustainability mandates. Secure long-term supply agreements for recycled PP resin. |

Investors | Target Niche Innovators: Focus on companies specializing in Type D, conductive, or food-grade bags, which offer higher value than commodity bags. Look for firms with proven, scalable technology in smart packaging (RFID/IoT integration). |

Logistics Providers | Standardize on Baffle Bags: Promote the adoption of baffle bags (Q-Bags) to clients to maximize shipping container utilization (up to 25% better space efficiency), leading to lower shipping costs and a competitive advantage. |

Startups/New Entrants | Focus on Software/Service: Instead of competing on commodity bag production, develop software platforms for managing the lifecycle, tracking, and certification of multi-trip bulk bags, creating an indispensable service layer. |

Browse More Reports:

Global Transcritical CO2 Systems Market

Asia-Pacific Bio Preservation Market

Global Orthopedic Navigation Systems Market

Europe Electric Enclosure Market

Middle East and Africa Sludge Treatment Chemicals Market

Global Antimicrobial Drugs Market

Global Ballistic Composites Market

Global IoT Gateways Market

Global Mini Truck Market

Global Sustainable Toys Market

Global Empty Capsules Market

Global All Wheel Drive (AWD) Systems Market

Global Unmanned Ground Vehicle Market

Global Green Tea Market

Global Panniculitis Market

Asia-Pacific pH sensors Market

Global Facial Tracking Solutions Market

Global Skid Steer Loaders For Construction Market

Global Geographic Information System (GIS) Software Market

Asia-Pacific Plastic Compounding Market

Asia-Pacific Data Integration Market

Middle East and Africa Infection Surveillance Solution Systems Market

Global Candy Coated Chocolate Market

Global Water-Based High-Performance Coatings Market

Global Abscisic Acid (ABA) Market

Global Flake Ice Machine Market

Global Text-To-Speech Market

Middle East and Africa Acute Lymphocytic/Lymphoblastic Leukemia (ALL) Diagnostics Market

Global Toaster Market

Global Haematococcus Market

Global Bio-Based Hot Melt Adhesive (HMA) Market

Global Metacarpal Joint Implants Market

About Data Bridge Market Research:

An absolute way to forecast what the future holds is to comprehend the trend today!

Data Bridge Market Research set forth itself as an unconventional and neoteric market research and consulting firm with an unparalleled level of resilience and integrated approaches. We are determined to unearth the best market opportunities and foster efficient information for your business to thrive in the market. Data Bridge endeavors to provide appropriate solutions to the complex business challenges and initiates an effortless decision-making process. Data Bridge is an aftermath of sheer wisdom and experience which was formulated and framed in the year 2015 in Pune.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email:- corporatesales@databridgemarketresearch.com