Executive Summary

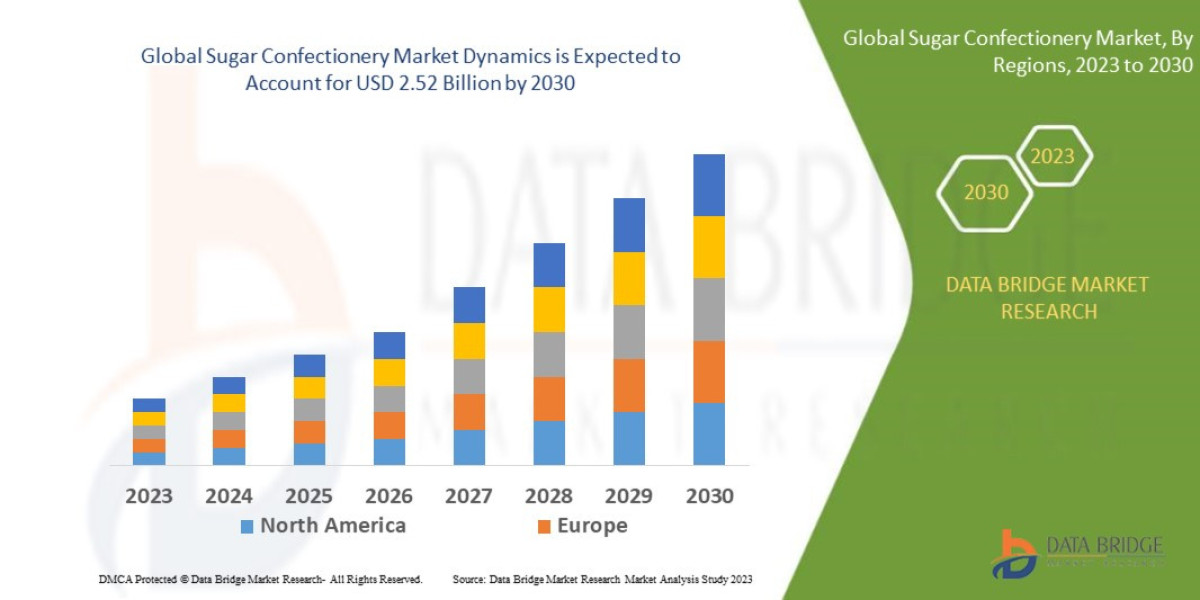

Data Bridge Market Research analyses that the global sugar confectionery market which was growing at a value of USD 1.89 billion in 2022 is expected to reach the value of USD 2.52 billion by 2030, at a CAGR of 3.7% during the forecast period of 2023-2030.

Market Overview

The Sugar Confectionery Market is defined by products whose primary functional and structural ingredient is sugar (sucrose, glucose, fructose, etc.), differentiating it from the Chocolate Confectionery Market, though many players operate across both. It is inherently an impulse-driven market, highly sensitive to retail placement and promotional activities.

Key Segments and Product Types

The market is typically segmented by product type, each with distinct manufacturing processes, shelf lives, and consumer targets:

Hard-Boiled Candies: The most traditional segment, offering long shelf stability and simple ingredient lists.

Gummies and Jellies (Highest Growth): Driven by texture preference and the rise of functional, fortified products (vitamins, probiotics).

Caramels and Toffees: Highly popular in seasonal and gifting contexts, often associated with premium positioning.

Chewing Gum: A highly specialized segment focused on oral health benefits and innovative flavor release systems.

Lollipops and Mints: Impulse categories focused on immediate, low-cost consumption.

Drivers and Current Dynamics

Core Market Drivers:

Rising Disposable Incomes: Particularly in the Asia-Pacific (APAC) and Latin American regions, enabling broader access to non-essential goods.

Seasonal and Celebratory Consumption: Confectionery remains intrinsically linked to holidays, festivals, and gifting traditions globally, providing reliable sales peaks.

Low Barrier to Entry (Local Markets): Regional players can easily enter the market with localized flavor profiles and affordable pricing.

Current Dynamics: The market is currently undergoing a value-versus-volume split. While traditional, high-volume products drive tonnage, the higher margins are increasingly found in the premium and specialty segments that cater to diet-conscious and health-aware consumers. This dynamic is shifting R&D focus from cost optimization to ingredient innovation.

Market Size & Forecast

Data Bridge Market Research analyses that the global sugar confectionery market which was growing at a value of USD 1.89 billion in 2022 is expected to reach the value of USD 2.52 billion by 2030, at a CAGR of 3.7% during the forecast period of 2023-2030.

For More Information Visit https://www.databridgemarketresearch.com/reports/global-sugar-confectionery-market

Key Trends & Innovations

Innovation is the lifeline of the confectionery market, responding directly to consumer demand for guilt-free indulgence, transparency, and personalization.

1. Functional Confectionery and Nutraceuticals

This is arguably the most impactful trend. Confectionery is transforming into a delivery vehicle for active ingredients. Gummies are the primary format for this, incorporating vitamins (D, C, B12), supplements (melatonin, collagen), and digestive aids (probiotics, fiber). This strategy allows brands to position their products in the health aisle, justifying a significant price premium.

2. The Sugar Reduction Revolution

Reformulation is paramount. Manufacturers are investing heavily in technologies to seamlessly replace high-fructose corn syrup and sucrose. Key alternative sweeteners include:

Natural High-Intensity Sweeteners: Stevia and Monk Fruit (Luo Han Guo) are highly favored due to their natural origin and clean-label appeal.

Sugar Alcohols: Erythritol and Xylitol are used for bulk, texture, and mouthfeel, particularly in hard candies, though regulatory limits on consumption are a consideration.

Allulose: Gaining traction as a low-calorie sugar that behaves chemically like traditional sugar, aiding in texture development.

3. Clean Labeling and Transparency

Consumers, particularly Millennials and Gen Z, demand ingredient transparency. This trend is eliminating artificial colors (e.g., replacement of FD&C dyes with colors derived from fruit and vegetable concentrates like beetroot, turmeric, and spirulina) and artificial flavors. Products with short, recognizable ingredient lists are preferred.

4. Flavor Innovation and Adult-Focused Offerings

While classic flavors persist, innovation targets sophisticated, adult palates. This includes complex, multi-layered profiles (e.g., spiced caramel, exotic fruits, botanical infusions) and incorporating heat or savory notes (chili, sea salt). The goal is to elevate the confectionery experience from a simple treat to a premium, curated moment of indulgence.

Competitive Landscape

The global market structure is oligopolistic at the top, highly fragmented at the bottom, and intensely competitive in the middle segment of regional specialty brands.

Major Players and Strategic Imperatives

Global Leaders (e.g., Mars, Inc., Mondelez International, Nestlé, Ferrara Candy Company): These players dominate market share through immense distribution power, strong brand equity, and massive marketing budgets. Their strategy is dual-faceted:

Defense: Protecting core high-volume brands (e.g., Skittles, Sour Patch Kids) through slight reformulations and aggressive promotional pricing.

Offense: Acquiring niche, innovative brands (M&A activity is high) and rapidly launching internal low-sugar or functional lines to capture premium revenue growth.

Mid-Sized and Regional Players (e.g., Haribo, Perfetti Van Melle, local gum companies): Compete by focusing on specific geographic or product strengths. Their advantage lies in deep local market penetration and flavor relevance.

Startups and Niche Brands: Focus almost exclusively on the premium segments (e.g., keto-friendly, functional gummies, organic certification). They rely on direct-to-consumer (D2C) channels and strong social media branding to drive early traction before potentially becoming acquisition targets.

Competitive success increasingly hinges on supply chain efficiency to manage the complexity of sourcing both high-volume sugar and specialized, expensive alternative ingredients.

Regional Insights

Market dynamics vary significantly by region, primarily influenced by regulatory environment, economic development, and cultural food traditions.

North America and Western Europe (Value Drivers)

These regions are the largest in terms of market value due to high per-capita spending and a mature demand for premium products.

Focus: Dominated by the Health & Wellness trend. Growth is driven by the low/no-sugar segments, functional confectionery, and organic/natural certifications. Regulatory pressure (e.g., sugar taxes in some jurisdictions) is high.

Asia-Pacific (APAC) (Volume Drivers)

APAC is the undisputed leader in volume growth, fueled by large populations, rising middle-class disposable incomes, and urbanization.

Focus: The market remains highly receptive to traditional, affordable sugar formats. Key opportunities lie in localized flavor adaptation (e.g., matcha, chili, unique fruits) and developing mass-market price points. India and China are central growth engines.

Latin America (LATAM) and Middle East & Africa (MEA) (Emerging Opportunities)

These markets offer significant long-term potential but are more volatile.

Focus: LATAM is witnessing a rapid regulatory evolution (e.g., clear front-of-pack warning labels for high sugar content in Chile and Mexico), which creates immediate demand for reformulation. MEA growth is driven by rising population and increasing access to international brands.

Challenges & Risks

The inherent nature of the product, combined with external pressures, presents significant operational and strategic risks.

1. Raw Material Price and Supply Volatility

The cost of sugar, corn syrup, and hydrocolloids (like gelatin) is subject to global commodity market volatility, severely impacting manufacturers' margins. Furthermore, the reliance on specialized, natural sweeteners (e.g., Stevia extract) introduces single-source supply chain risk.

2. Regulatory Scrutiny and Taxation

A major and accelerating risk is government intervention aimed at curbing non-essential sugar intake to combat obesity and diabetes. This includes:

Sugar Taxes: Levies on sugar content (implemented in the UK, Mexico, etc.) directly raising retail prices and reducing demand elasticity.

Marketing Restrictions: Bans on advertising high-sugar products to children.

Mandatory Front-of-Pack (FOP) Warning Labels: These labels (e.g., 'High in Sugar' icons) negatively influence consumer choice.

3. Product Reformulation Challenges

Creating a low/no-sugar product that maintains the necessary texture, mouthfeel, shelf stability, and flavor profile of its full-sugar counterpart is technically complex and expensive. Sugar is not just a sweetener; it is a critical structural and preservative agent. Failures in reformulation lead to poor consumer acceptance and brand damage.

4. Intellectual Property and Clean-Label Sourcing

As the market shifts to natural ingredients, the challenge of consistently sourcing certified organic, non-GMO, and fair-trade ingredients at scale—while verifying the authenticity of natural colorants—becomes a critical logistical bottleneck.

Opportunities & Strategic Recommendations

Despite the challenges, the Sugar Confectionery Market offers substantial opportunities for stakeholders willing to invest in technology and adapt their portfolios.

Strategic Recommendations for Manufacturers and Stakeholders

Prioritize Portfolio Decoupling (The 80/20 Rule):

Action: Dedicate 80% of R&D budget to the premium, low-sugar, and functional segments (e.g., functional gummies, premium natural hard candies), as these drive value and margin growth.

Rationale: Hedge against future sugar tax regimes and capture high-spending, health-conscious consumers.

Invest in Proprietary Sweetening IP:

Action: Form strategic partnerships with or acquire companies specializing in the extraction and application of next-generation sweeteners (e.g., fermentation-derived non-caloric sweeteners, specific rare sugars).

Rationale: Gain a technological moat, allowing for superior flavor and texture in low-sugar products that competitors cannot replicate easily.

Optimize the D2C and Gifting Channel:

Action: Leverage e-commerce platforms to offer highly curated, premium gifting options and personalized packaging. Use digital channels to communicate the functional benefits and natural ingredient sourcing stories, which often resonate best in a D2C context.

Rationale: D2C bypasses crowded retail shelves, allows for higher margins, and targets the consumer desire for personalization and premium experience.

Embrace Transparent Sourcing and Certification:

Action: Seek high-level certifications (e.g., Non-GMO Project Verified, specific ethical sourcing labels) and use blockchain or similar technologies to verify and communicate the source of natural ingredients and colors directly to the consumer via QR codes.

Rationale: Build brand trust and justify the premium price points required for the new generation of clean-label confectionery.

Browse More Reports:

Global Transcritical CO2 Systems Market

Asia-Pacific Bio Preservation Market

Global Orthopedic Navigation Systems Market

Europe Electric Enclosure Market

Middle East and Africa Sludge Treatment Chemicals Market

Global Antimicrobial Drugs Market

Global Ballistic Composites Market

Global IoT Gateways Market

Global Mini Truck Market

Global Sustainable Toys Market

Global Empty Capsules Market

Global All Wheel Drive (AWD) Systems Market

Global Unmanned Ground Vehicle Market

Global Green Tea Market

Global Panniculitis Market

Asia-Pacific pH sensors Market

Global Facial Tracking Solutions Market

Global Skid Steer Loaders For Construction Market

Global Geographic Information System (GIS) Software Market

Asia-Pacific Plastic Compounding Market

Asia-Pacific Data Integration Market

Middle East and Africa Infection Surveillance Solution Systems Market

Global Candy Coated Chocolate Market

Global Water-Based High-Performance Coatings Market

Global Abscisic Acid (ABA) Market

Global Flake Ice Machine Market

Global Text-To-Speech Market

Middle East and Africa Acute Lymphocytic/Lymphoblastic Leukemia (ALL) Diagnostics Market

Global Toaster Market

Global Haematococcus Market

Global Bio-Based Hot Melt Adhesive (HMA) Market

About Data Bridge Market Research:

An absolute way to forecast what the future holds is to comprehend the trend today!

Data Bridge Market Research set forth itself as an unconventional and neoteric market research and consulting firm with an unparalleled level of resilience and integrated approaches. We are determined to unearth the best market opportunities and foster efficient information for your business to thrive in the market. Data Bridge endeavors to provide appropriate solutions to the complex business challenges and initiates an effortless decision-making process. Data Bridge is an aftermath of sheer wisdom and experience which was formulated and framed in the year 2015 in Pune.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email:- corporatesales@databridgemarketresearch.com