Executive Summary

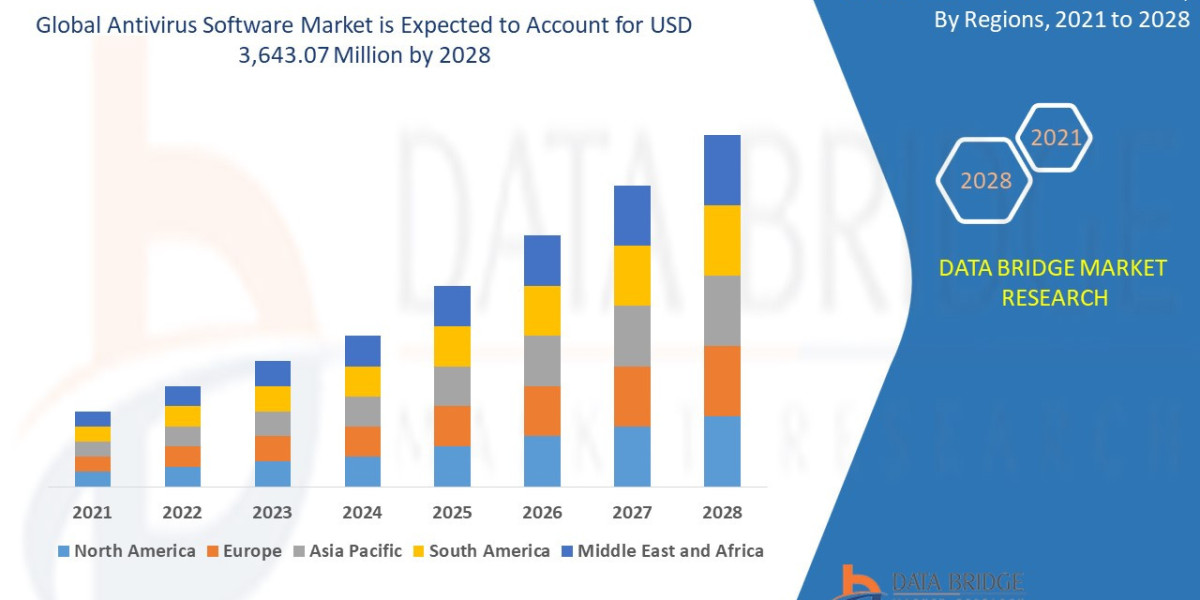

Antivirus software market size is valued at USD 3,643.07 million by 2028 is expected to grow at a compound annual growth rate of 1.6% in the forecast period of 2021 to 2028.

Market Overview

The Antivirus Software Market encompasses solutions designed to detect, prevent, and remove malicious software, including viruses, worms, malware, spyware, and ransomware. The definition has broadened significantly, now primarily referring to Endpoint Protection Platforms (EPP) that offer multi-layered defense beyond simple file scanning.

Key Segments and Functionality

The market is segmented primarily by deployment and user type:

By Deployment:

Cloud-Based (Dominant Growth): Preferred for scalability, lower maintenance costs, and centralized management across geographically dispersed endpoints.

On-Premise (Legacy/Highly Regulated): Still used by sectors with strict data sovereignty requirements (e.g., government, highly regulated finance).

By User Type:

Consumer: Solutions focused on ease of use, parental controls, VPN integration, and basic phishing protection for individuals and small offices.

Enterprise/Business: Advanced EPP and EDR solutions featuring centralized management, behavioral analysis, threat hunting, and deep integration with Security Information and Event Management (SIEM) systems.

Drivers and Current Dynamics

Core Market Drivers:

Ransomware Proliferation: The exponential growth in file-encrypting attacks, which often bypass legacy defenses, forcing organizations and consumers to adopt advanced EDR solutions.

Shift to Remote Work/Hybrid Models: The dissolution of the traditional network perimeter has made every employee device an exposed endpoint, demanding comprehensive, cloud-managed protection.

IoT and Endpoint Explosion: Every new connected device (mobile, tablet, smart device) represents a potential entry point for malware, requiring diverse protection mechanisms.

Maturing AI/ML Capabilities: The ability of security solutions to perform real-time behavioral analysis and predict threats, moving defense from reactive to proactive.

Current Dynamics: The primary dynamic is the consolidation of security features. Customers are moving away from multiple point products to unified platforms offering not just antivirus, but firewalls, web filtering, VPN, password management, and identity theft protection under a single subscription.

Market Size & Forecast

Antivirus software market size is valued at USD 3,643.07 million by 2028 is expected to grow at a compound annual growth rate of 1.6% in the forecast period of 2021 to 2028.

For More Information Visit https://www.databridgemarketresearch.com/reports/global-antivirus-software-market

Key Trends & Innovations

The market is defined by technological leaps that prioritize speed, detection accuracy, and integration across the security ecosystem.

1. AI and Behavioral-Based Detection (Next-Gen AV)

Traditional signature-matching is now considered obsolete against polymorphic malware. Modern solutions use sophisticated machine learning (ML) models to analyze system behavior, network traffic, and file context. This allows them to:

Identify zero-day exploits by flagging anomalous activity before a signature is even known.

Correlate events across devices to detect coordinated attacks (Lateral Movement).

2. Endpoint Detection and Response (EDR)

EDR is rapidly becoming a mandatory feature, extending beyond prevention to provide Visibility and Response. EDR tools continuously record endpoint activity, allowing security teams to:

Threat Hunt: Proactively search for malicious patterns.

Isolate and Remediate: Automatically quarantine affected systems and roll back malicious changes.

Forensics: Provide detailed telemetry for post-incident analysis.

3. Consolidation into Unified Security Stacks

The trend of vendor consolidation means customers prefer platforms that seamlessly integrate various security functions. Leading solutions now offer:

Cloud Access Security Broker (CASB)

Data Loss Prevention (DLP)

Vulnerability Management

Identity Protection (via integration with IAM tools)

This consolidation improves efficiency and reduces the management overhead known as "security sprawl."

4. Regulatory Changes: Emphasis on Reporting and Compliance

Global regulations (e.g., GDPR, CCPA, NIS 2 Directive in the EU) mandate stringent breach notification and require organizations to demonstrate "reasonable and appropriate" security controls. This regulatory pressure directly translates into demand for high-fidelity EDR and compliance reporting features within antivirus platforms.

Competitive Landscape

The Antivirus Software Market is highly segmented, featuring legacy giants, focused EDR pure-plays, and platform innovators.

Major Players and Strategic Strategies

Legacy Leaders (e.g., Broadcom/Symantec, McAfee, Trend Micro): These companies leverage their massive installed base and strong channel partnerships. Their strategy centers on platform transformation, aggressively acquiring EDR/AI startups and migrating their customer base from legacy point products to integrated suites.

Next-Generation EPP/EDR Innovators (e.g., CrowdStrike, SentinelOne): These players disrupted the market by building cloud-native, behavior-based protection from the ground up. Their strategies focus on speed, performance, and API integration with other security tools, emphasizing their superiority in responding to advanced threats.

Platform Integrators (e.g., Microsoft Defender): Microsoft's strategy leverages its deep integration into the operating system (Windows) and the cloud ecosystem (Azure/M365). Its primary advantage is ubiquity and cost-effectiveness for organizations already invested in the Microsoft stack.

Consumer Specialists (e.g., NortonLifeLock, Avast/Gen Digital): Focus on delivering value-added consumer services (VPN, identity theft, parental controls) bundled with core antivirus, maintaining a strong presence in the home user segment.

The key competitive battleground is the mid-market, where the efficacy of cloud-based EDR and the quality of MDR services are the deciding factors.

Regional Insights

The market exhibits differentiated growth patterns based on economic maturity and cybersecurity maturity.

North America (Technological Leader and Highest Value)

Performance: The largest market by value, characterized by early and rapid adoption of cutting-edge technology (EDR, ZTNA, MDR). High concentration of security vendors and aggressive corporate spending drive premium pricing.

Opportunity: Continued migration to cloud-native EDR and strong demand from the rapidly expanding small-to-midsize business (SMB) sector.

Europe (Regulatory Driver)

Performance: A mature market driven heavily by compliance requirements (GDPR, NIS 2). Spending is robust, but vendors must cater to complex data residency laws.

Opportunity: Significant uptake in Managed Security Services (MSSP) offerings due to a shortage of in-house security talent, making MDR/MSSP partnerships a critical channel.

Asia-Pacific (APAC) (Fastest Volume Growth)

Performance: Experiencing the highest volumetric growth due to rapid digital transformation, increasing internet penetration, and a rising threat landscape across manufacturing and financial services.

Opportunity: Entry-level EPP solutions remain high-demand, but countries like Japan, South Korea, and Singapore are rapidly moving to enterprise-grade EDR and ZTA models.

Challenges & Risks

While demand is high, the market faces complex internal and external pressures.

1. The Skill Gap and Alert Fatigue

Advanced EDR systems generate massive volumes of data and alerts. The global shortage of qualified cybersecurity analysts leads to alert fatigue, where legitimate threats are missed amidst the noise. This drives organizations toward expensive MDR services.

2. Performance Overhead and Compatibility

Security software, particularly older, heuristic-heavy EPPs, can consume significant system resources (CPU, memory), impacting device performance. Modern solutions must prove their lightweight footprint to win over users and IT departments. Compatibility across diverse OS and legacy systems remains a challenge.

3. Commoditization of Core Features

Basic signature-based antivirus functionality is increasingly commoditized, often offered for free or included within operating systems (e.g., Microsoft Defender). This pressures vendors to justify subscription costs by continuously bundling and innovating with premium features (VPN, identity protection, EDR).

4. Insider Threats and Social Engineering

No software can fully mitigate threats originating from human error, such as successful phishing or social engineering attacks. This mandates that software providers must integrate more effective user training and phishing simulation tools into their offerings.

Opportunities & Strategic Recommendations

The transition to a cloud-first, AI-driven defense architecture creates clear avenues for strategic growth and investment.

Strategic Recommendations for Stakeholders

Invest in Integrated MDR/XDR Capabilities: For EPP vendors, the future is not selling software, but selling Security-as-a-Service. Invest heavily in building out the Managed Detection and Response (MDR) service layer or forming deep partnerships with MSSPs to translate EDR telemetry into actionable threat mitigation for mid-market clients.

Focus on Platform Unification (XDR): Shift product roadmaps toward Extended Detection and Response (XDR), which integrates data from endpoints, cloud workloads, network firewalls, and email to provide a holistic view of the attack surface, increasing stickiness and average revenue per user (ARPU).

Target the Operational Technology (OT) Sector: Industrial Control Systems (ICS) and OT environments, particularly in manufacturing and critical infrastructure, are highly vulnerable and undergoing digital convergence. Developing low-impact, high-reliability antivirus/EPP solutions for embedded and legacy OT systems represents a massive, high-margin niche opportunity.

Leverage Channel Partnerships in Emerging Markets: Establish aggressive distribution channels, localized pricing models, and educational content in APAC and LATAM, where demand for foundational, paid security software is just beginning to accelerate due to regulation and rapid enterprise growth.

Browse More Reports:

Global Transcritical CO2 Systems Market

Asia-Pacific Bio Preservation Market

Global Orthopedic Navigation Systems Market

Europe Electric Enclosure Market

Middle East and Africa Sludge Treatment Chemicals Market

Global Antimicrobial Drugs Market

Global Ballistic Composites Market

Global IoT Gateways Market

Global Mini Truck Market

Global Sustainable Toys Market

Global Empty Capsules Market

Global All Wheel Drive (AWD) Systems Market

Global Unmanned Ground Vehicle Market

Global Green Tea Market

Global Panniculitis Market

Asia-Pacific pH sensors Market

Global Facial Tracking Solutions Market

Global Skid Steer Loaders For Construction Market

Global Geographic Information System (GIS) Software Market

Asia-Pacific Plastic Compounding Market

Asia-Pacific Data Integration Market

Middle East and Africa Infection Surveillance Solution Systems Market

Global Candy Coated Chocolate Market

Global Water-Based High-Performance Coatings Market

Global Abscisic Acid (ABA) Market

Global Flake Ice Machine Market

Global Text-To-Speech Market

Middle East and Africa Acute Lymphocytic/Lymphoblastic Leukemia (ALL) Diagnostics Market

Global Toaster Market

Global Haematococcus Market

Global Bio-Based Hot Melt Adhesive (HMA) Market

About Data Bridge Market Research:

An absolute way to forecast what the future holds is to comprehend the trend today!

Data Bridge Market Research set forth itself as an unconventional and neoteric market research and consulting firm with an unparalleled level of resilience and integrated approaches. We are determined to unearth the best market opportunities and foster efficient information for your business to thrive in the market. Data Bridge endeavors to provide appropriate solutions to the complex business challenges and initiates an effortless decision-making process. Data Bridge is an aftermath of sheer wisdom and experience which was formulated and framed in the year 2015 in Pune.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email:- corporatesales@databridgemarketresearch.com