Executive Summary

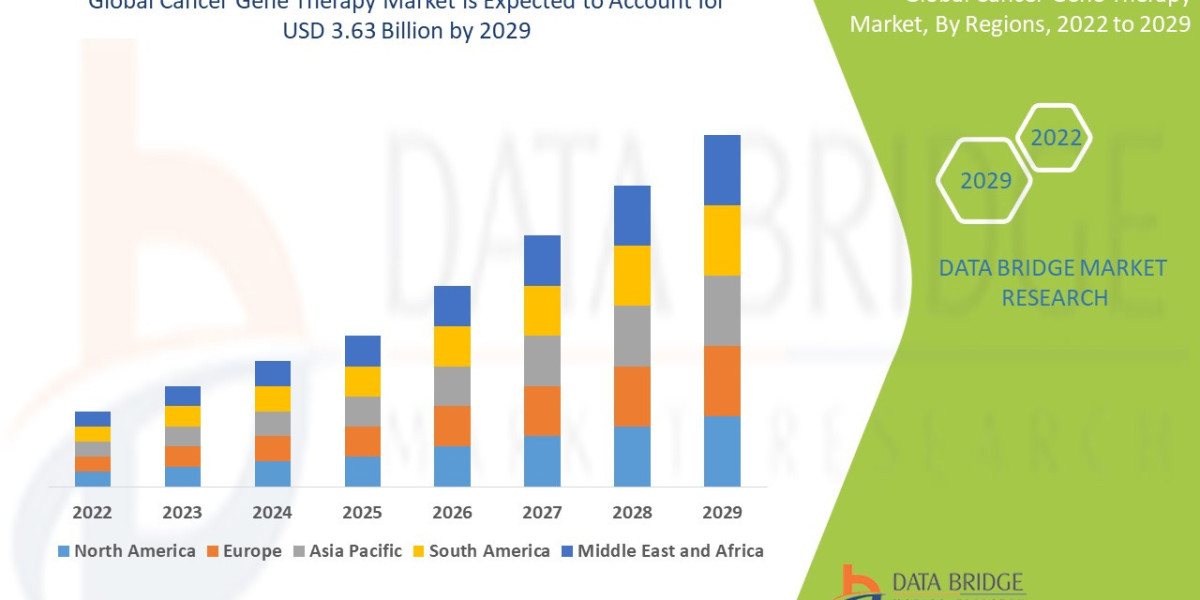

Global cancer gene therapy market size was valued at USD 2.28 billion in 2024 and is projected to reach USD 4.79 billion by 2032, with a CAGR of 9.70% during the forecast period of 2025 to 2032.

Market Overview

The Cancer Gene Therapy Market is defined by therapeutic approaches that introduce, remove, or modify genetic material (DNA or RNA) within cancer cells or immune cells to fight the disease. It sits at the intersection of biotechnology, genomics, and oncology.

Key Segments and Modalities

The market is primarily segmented by the type of therapeutic approach:

Cell Therapy (Dominant Segment): Primarily comprising CAR T-cell therapies (e.g., Kymriah, Yescarta, Tecartus) which involve modifying a patient's T-cells to target specific cancer antigens (like CD19). This is currently the largest and most established segment.

Oncolytic Virotherapy: Utilizing genetically modified viruses (like adenoviruses or herpes simplex viruses) that selectively replicate in and destroy cancer cells while leaving healthy cells untouched (e.g., Imlygic).

Gene Editing/Replacement: Approaches that use tools like CRISPR/Cas9 or traditional viral vectors (AAV, retrovirus) to correct a defective gene or introduce a gene that makes cancer cells susceptible to destruction.

Vector Type: Segmented by the delivery vehicle used to transport the genetic material, with viral vectors (Lentivirus, Adenovirus, AAV) dominating due to high transduction efficiency, though non-viral alternatives are growing.

Drivers and Current Dynamics

Core Market Drivers:

Clinical Success in Hematologic Malignancies: The demonstrated durable responses and curative potential of CAR T-cell therapy in refractory lymphomas and leukemias established the commercial viability and regulatory precedent for gene therapy.

Robust Pipeline Investment: A massive influx of private and public investment, fueling R&D in next-generation targets, novel vectors, and allogeneic platforms.

Advancements in Gene Editing Technologies: The therapeutic use of CRISPR and base editing is rapidly accelerating the development of safer and more precise ex vivo and in vivo therapies.

Increasing Cancer Incidence Globally: The rising prevalence of cancer worldwide creates a continuous, high-unmet-need patient pool for advanced therapies.

Current Dynamics: The primary dynamic is the aggressive race to crack solid tumors and overcome the limitations of autologous therapy (high cost, long turnaround time, logistical complexity) through the development of Allogeneic (Off-the-Shelf) CAR-T.

Market Size & Forecast

Global cancer gene therapy market size was valued at USD 2.28 billion in 2024 and is projected to reach USD 4.79 billion by 2032, with a CAGR of 9.70% during the forecast period of 2025 to 2032.

For More Information Visit https://www.databridgemarketresearch.com/reports/global-cancer-gene-therapy-market

Key Trends & Innovations

Innovation in gene therapy is focused on making treatments safer, faster, and more effective against a broader range of cancers.

1. The Shift to Allogeneic (Off-the-Shelf) Therapies

The biggest paradigm shift is the move from autologous (patient's own cells) to allogeneic (donor cells). Allogeneic therapies promise:

Reduced Turnaround Time: Immediate availability from stock, eliminating the 3–6 week patient wait.

Scalability: Allows for large-scale production runs, lowering per-dose COGS.

Consistency: Consistent product quality derived from healthy donor cells.

Technology: These therapies rely heavily on advanced gene editing (e.g., TALENs, CRISPR) to mitigate the risk of GvHD (Graft-versus-host disease) and improve T-cell persistence.

2. Targeting the Solid Tumor Microenvironment (TME)

The primary challenge in solid tumors is the hostile TME, which physically blocks T-cells and contains immunosuppressive signals. Key innovations to overcome this include:

Armored CAR T-cells: Engineering CAR T-cells to secrete immune-boosting molecules (e.g., IL-12) to break down the TME.

Dual Targeting: Using CAR T-cells engineered to target two or more antigens simultaneously to prevent antigen escape (the tumor losing its target to evade detection).

3. In Vivo Gene Therapy

Moving beyond ex vivo manipulation (cells modified outside the body), in vivo approaches deliver the therapeutic gene directly to the patient’s cells inside the body. This simplifies logistics dramatically. Advances in Adeno-Associated Virus (AAV) vector engineering are critical here, focusing on making the vectors more specific to tumor cells and less visible to the patient’s immune system.

4. Regulatory Harmonization and Accelerated Approval

Regulatory bodies (FDA, EMA) continue to establish clear, adaptive frameworks for these breakthrough therapies. The use of designations like RMAT (Regenerative Medicine Advanced Therapy) and PRIME (Priority Medicines) allows developers to accelerate clinical trials and market entry, provided they meet strict safety and efficacy endpoints.

Competitive Landscape

The market is currently dominated by a few large pharmaceutical companies that acquired or partnered with early biotech pioneers, alongside a vibrant ecosystem of specialized startups.

Major Players and Strategic Strategies

Pharmaceutical Giants (e.g., Novartis, Gilead Sciences/Kite, Bristol Myers Squibb/Celgene): These firms lead the current commercial landscape, holding approvals for first-generation CAR-T products. Their strategy involves global expansion, label expansion into earlier lines of therapy, and aggressive licensing/M&A to acquire allogeneic or solid tumor platforms.

Biotech Innovators (e.g., CRISPR Therapeutics, Allogene Therapeutics, bluebird bio): These firms focus on platform technologies—specifically advanced gene editing (CRISPR) and allogeneic manufacturing—to disrupt the current market leaders by delivering scalable and potentially cheaper products. Their strategy centers on clinical execution and establishing intellectual property dominance in novel targeting mechanisms.

Contract Development and Manufacturing Organizations (CDMOs): Companies like Catalent and Lonza are crucial strategic players. They compete by offering specialized expertise and scalable, compliant manufacturing capacity, serving as the essential backbone for smaller companies without internal capabilities.

Competition is shifting from clinical efficacy (proven) to manufacturing efficiency, supply chain robustness, and cost containment.

Regional Insights

Market maturity and growth are heavily influenced by the speed of regulatory approval, healthcare funding mechanisms, and R&D infrastructure.

North America (Technology Leader and Primary Revenue Driver)

Performance: The largest market globally, characterized by the highest number of approved centers, rapid reimbursement decisions, and massive R&D expenditure. US academic institutions and biotech clusters drive early innovation.

Opportunity: Continued growth in specialized treatment centers and expansion of coverage for second and third-generation therapies.

Europe (Strong Clinical Base, Price Sensitivity)

Performance: A mature clinical landscape with high patient demand, but growth is tempered by complex, country-by-country Health Technology Assessment (HTA) processes, which exert significant pressure on pricing.

Opportunity: Harmonization efforts (EU HTA Regulation) promise to streamline market access, opening significant opportunities for companies that can demonstrate strong Pharmacoeconomic value.

Asia-Pacific (APAC) (Future Growth Engine)

Performance: While currently smaller, the region is rapidly accelerating, driven by government investment in domestic biotech (particularly China), an increasing number of clinical trials, and a large patient population.

Opportunity: Localized manufacturing and CDMO partnerships will be critical for success, bypassing logistical hurdles associated with importing temperature-sensitive products.

Challenges & Risks

Despite its promise, the cancer gene therapy market faces unique operational, clinical, and economic hurdles.

1. High Cost and Reimbursement Barriers

Current autologous CAR T-cell therapies carry a list price exceeding $400,000, creating profound access and reimbursement challenges for healthcare systems globally. Payers are increasingly demanding value-based and outcome-based pricing models (e.g., payment only if the patient responds), increasing financial risk for manufacturers.

2. Manufacturing and Logistics Complexity

The vein-to-vein supply chain for autologous therapy is highly complex, involving apheresis, cryopreservation, shipping, centralized manufacturing, quality control, and re-infusion. This fragile, bespoke process is highly prone to errors, which can be fatal to the patient. Scalability remains the chief technical constraint.

3. Safety Concerns and Long-Term Unknowns

Acute toxicities, primarily Cytokine Release Syndrome (CRS) and Immune Effector Cell-Associated Neurotoxicity Syndrome (ICANS), require specialized clinical management. Additionally, the long-term safety of integrating new genetic material, particularly the theoretical risk of secondary malignancies, necessitates multi-decade patient follow-up.

4. Limited Efficacy in Solid Tumors

The majority of successes remain confined to liquid tumors. The clinical failure rate in solid tumors due to TME hostility and the lack of truly tumor-specific surface antigens remains the most significant technical risk to the market's long-term volumetric potential.

Opportunities & Strategic Recommendations

Success in this market demands integrated expertise across biology, logistics, and digital manufacturing.

Strategic Recommendations for Stakeholders

Prioritize Allogeneic Manufacturing Scale: Investors and developers should focus capital aggressively on platforms that expedite allogeneic product development. The first company to deliver a safe, highly efficacious, and globally scalable off-the-shelf CAR-T for a major solid tumor will capture enormous market share.

Vertical Integration of Supply Chain: Companies should vertically integrate or establish robust, exclusive partnerships with CDMOs to secure manufacturing slots and control quality. Investment in automated, closed-system manufacturing equipment is non-negotiable to reduce COGS and limit human error.

Develop Value-Based Pricing Models: Manufacturers must proactively develop sophisticated data-gathering mechanisms to prove the long-term, curative value of their therapies to justify premium pricing. Propose risk-sharing agreements or indication-specific tiered pricing to accelerate global adoption and minimize payer resistance.

Target and Penetrate Early-Stage Cancer: The ultimate opportunity lies in moving gene therapies from last-line rescue treatments to first-line therapy immediately following diagnosis. Strategic focus on this high-value, high-volume segment requires developing therapies with superior safety profiles and easier administration (potentially in vivo).

Browse More Reports:

Global Capacitive Sensor Market

Middle East and Africa Genetic Testing Market

Asia-Pacific Heavy Metals Testing Market

Global Hydrographic Survey Equipment Market

Global Aquaculture Feed Carotenoids Market

Global Toxic Epidermal Necrolysis Market

Global Asherman’s Syndrome Market

Global Fibers and Specialty Carbohydrates Market

Global Potassium Tetrafluoroborate Market

Global Biomedical Refrigerators and Freezers Market

Global Sjögren’s Syndrome Market

Global Portable Density Meter Market

Asia-Pacific Potato Processing Market

Europe Healthcare Logistics Market

Global TRIAC Market

Asia-Pacific Infection Surveillance Solution System Market

Global Torque Converter Market

Global Biotinidase Deficiency Market

Global Healthcare Logistics Market

Global Oil and Fuel Filter Market

Global Surface Protection Films Market

Asia-Pacific Xylose Market

Global GaN and SiC Power Semiconductor Market

Global Screw-On Caps Market

Global Mineral Wool Market

Global Bancassurance Market

Global Light Gauge Steel Framing Market

Global Crude Sulfate Turpentine Market

Europe Digital Farming Software Market

Asia-Pacific q-PCR Reagents Market

Middle East and Africa Heavy Metals Testing Market

About Data Bridge Market Research:

An absolute way to forecast what the future holds is to comprehend the trend today!

Data Bridge Market Research set forth itself as an unconventional and neoteric market research and consulting firm with an unparalleled level of resilience and integrated approaches. We are determined to unearth the best market opportunities and foster efficient information for your business to thrive in the market. Data Bridge endeavors to provide appropriate solutions to the complex business challenges and initiates an effortless decision-making process. Data Bridge is an aftermath of sheer wisdom and experience which was formulated and framed in the year 2015 in Pune.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975