Executive Summary

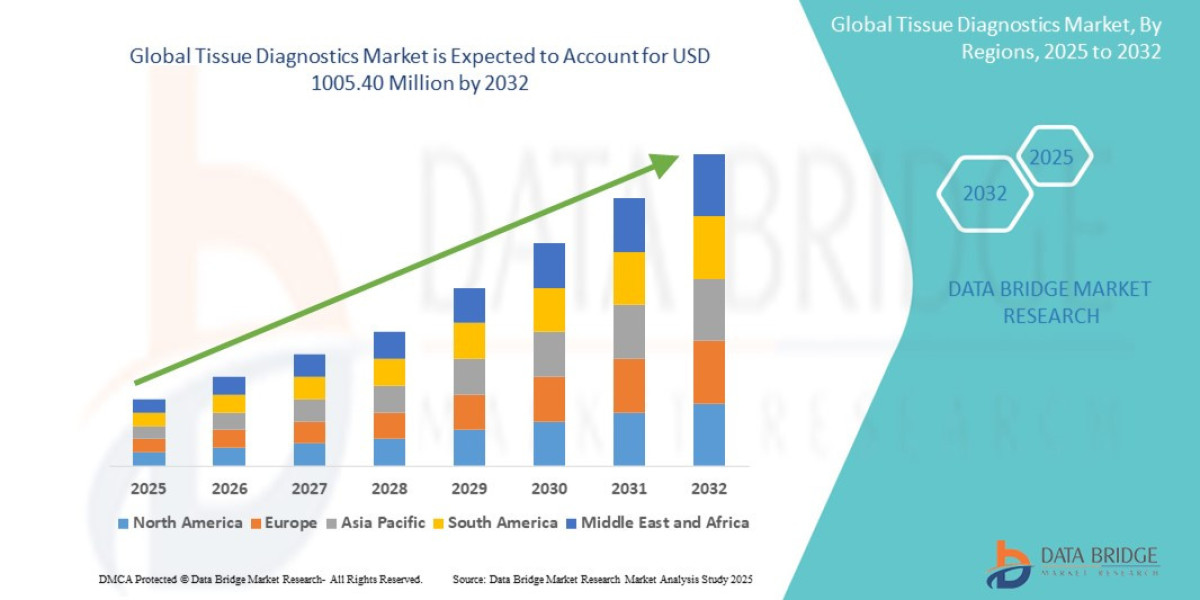

- The global tissue diagnostics market size was valued at USD 602.95 Million in 2024 and is expected to reach USD 1,005.40 Million by 2032, at a CAGR of 6.60% during the forecast period

Market Overview

Tissue diagnostics involves the preparation and analysis of solid tissue samples, providing morphological and molecular information essential for clinical decision-making. The market spans the entire workflow, from sample preparation in the laboratory to final pathological review.

Key Segments by Product

Consumables and Reagents (Dominant Segment): Includes primary and secondary antibodies, special stains, paraffin wax, and fixation chemicals. This is the highest revenue segment due to its high volume and recurring demand.

Instruments: Encompasses tissue processors, automated strainers, slide scanners (for digital pathology), and microtomes. Automation in this segment is a major growth driver.

Software and Services (Fastest Growing Segment): Comprises image management systems (IMS), analysis algorithms powered by Artificial Intelligence (AI), and digital storage solutions.

Key Segments by Technology

Immunohistochemistry (IHC) (Largest Sub-segment): Uses antibodies to detect specific protein antigens in tissue. IHC is essential for classifying tumors (e.g., breast cancer receptors) and validating therapeutic targets.

In Situ Hybridization (ISH): Used to detect specific DNA or RNA sequences within the tissue, crucial for identifying gene amplifications (e.g., HER2) or chromosomal anomalies.

Digital Pathology and Image Analysis: The integration of whole slide imaging (WSI) and computational analysis tools.

Special Staining and Histopathology: Traditional chemical staining techniques (e.g., H&E) providing structural morphology.

Drivers and Current Dynamics

Core Market Drivers:

Rising Global Cancer Incidence: The most significant driver, increasing the volume of diagnostic biopsies required worldwide.

Increased Demand for Personalized Medicine: The need to precisely characterize tumors (biomarker testing) to match patients with targeted therapies necessitates advanced IHC and ISH techniques.

Technological Advancements in Automation: Automation of staining and slide preparation reduces human error, improves throughput, and ensures consistency in high-volume labs.

Growth in Biopharma R&D: Pharmaceutical companies rely on tissue analysis to validate drug targets and select appropriate patient cohorts for clinical trials.

Current Dynamics: The market is undergoing a fundamental transformation driven by digitalization. Pathology labs are transitioning from glass slides to digital images, creating new demand for WSI scanners, massive data storage, and AI tools for automated analysis and quality control.

Market Size & Forecast

- The global tissue diagnostics market size was valued at USD 602.95 Million in 2024 and is expected to reach USD 1,005.40 Million by 2032, at a CAGR of 6.60% during the forecast period

For More information visit https://www.databridgemarketresearch.com/reports/global-tissue-diagnostics-market

Key Trends & Innovations

Innovation is focused on improving speed, accuracy, and providing multimodal data from a single tissue sample.

1. The Digital Pathology Revolution and AI Integration

The shift to Digital Pathology is the single most critical trend. Whole Slide Imaging (WSI) allows for remote consultation and centralized analysis. The integration of AI and Deep Learning algorithms enhances this by:

Automating image review and counting (e.g., Ki-67 scoring).

Predicting prognosis or treatment response from subtle morphological patterns (Morphometric Analysis).

Flagging critical areas for the pathologist, acting as a "second eye."

2. Multi-Omics Spatial Biology

A key frontier is Spatial Transcriptomics and Proteomics, where technologies (e.g., multiplex IHC, high-plex fluorescent staining) allow researchers to map the expression of multiple proteins or genes while preserving their precise location within the tissue architecture. This is vital for understanding the tumor microenvironment (TME) and complex cellular interactions.

3. Advancements in Automated Staining Platforms

Manufacturers are developing advanced, fully integrated staining instruments capable of running both IHC and ISH simultaneously with minimal human intervention. These systems emphasize traceability and laboratory information system (LIS) connectivity for compliance and workflow management.

4. Liquid Biopsy Integration

While not strictly tissue diagnostics, the market is influenced by the rise of liquid biopsy. Strategic efforts are underway to combine molecular data from liquid biopsies (circulating tumor DNA/cells) with traditional tissue morphology to provide a comprehensive, multi-layered diagnostic view.

Competitive Landscape

The market is highly consolidated, with major global players dominating the instrument and high-value reagent segments, while smaller companies drive innovation in the rapidly evolving software and AI space.

Major Players and Strategic Strategies

Integrated Diagnostics Leaders (e.g., Roche [Ventana], Danaher [Leica Biosystems]): These giants dominate the core IHC and Histology instrument market. Their strategy is Platform Lock-in and Consolidation, offering proprietary closed systems (instruments + reagents) to secure high, recurring consumable revenue and acquire key digital pathology/AI startups to complete their workflow offering.

Specialized Reagent Providers (e.g., Agilent [Dako]): Focus on developing, validating, and marketing highly specific primary antibodies and companion diagnostic tests. Their strategy is Clinical Validation, ensuring their assays are integral to approved drug protocols.

Digital and AI Innovators (e.g., Paige, various startups): Pure-play software companies. Their competitive edge is Algorithmic Superiority and Regulatory Agility, seeking FDA clearance for AI tools that directly assist in primary diagnosis, a major barrier to entry for incumbents.

The current competitive focus is shifting from a hardware/reagent battle to a data and algorithm race for digital pathology dominance.

Regional Insights

Adoption rates for advanced tissue diagnostics correlate strongly with established healthcare infrastructure, cancer screening programs, and reimbursement policies.

North America (Technology Leadership and High Spend)

Performance: The largest revenue generator, driven by high cancer incidence, significant R&D spending, favorable reimbursement for advanced molecular diagnostics, and early regulatory approval for AI and digital pathology systems.

Opportunity: High demand for sophisticated companion diagnostic testing and accelerated adoption of automated workflow solutions.

Europe (Regulatory Harmonization and Quality Focus)

Performance: A mature, high-volume market with stringent quality control standards. The implementation of the IVDR (In Vitro Diagnostic Regulation) is driving a major effort to standardize and certify assays, creating demand for validated and automated systems.

Opportunity: High potential for Digital Pathology adoption as centralized health systems realize the workflow efficiency benefits of remote review and consultation.

Asia-Pacific (APAC) (High Growth Potential)

Performance: The fastest-growing region, fueled by massive, unmet clinical demand due to a large and aging population, improving healthcare infrastructure, and rising investment in localized oncology research (especially in China and India).

Opportunity: Strong demand for high-throughput, cost-effective automated IHC systems. China's rapidly developing domestic diagnostics industry presents both an opportunity for partnership and a threat from local low-cost competitors.

Challenges & Risks

The transition to advanced, data-driven pathology introduces complexity and regulatory barriers.

1. Data Interoperability and Storage Costs

Digital pathology generates massive Whole Slide Images (WSI) files (often gigabytes per slide). Managing, storing, and transferring this data requires substantial IT investment and a robust, secure infrastructure. A lack of standardized file formats and vendor lock-in create interoperability challenges between different scanners and analysis software.

2. Standardization and Consistency

Reproducibility remains a challenge, particularly in IHC, where variations in tissue fixation, processing, and staining protocols can lead to inconsistent results across different laboratories. This inconsistency poses a significant risk to clinical trial validation and diagnostic accuracy.

3. Regulatory Hurdles for AI

Gaining regulatory clearance (e.g., FDA or CE Mark) for Artificial Intelligence algorithms used in primary diagnosis is complex and costly. Algorithms must demonstrate robust performance across diverse tissue types, staining variability, and patient populations, which requires vast, high-quality, annotated datasets.

4. Pathologist Shortage and Digital Proficiency

Globally, there is a shortage of skilled pathologists. While digital tools aim to mitigate this, they also require pathologists to adopt new digital workflows and gain proficiency in image analysis and software interfaces, a significant change management challenge.

Opportunities & Strategic Recommendations

Success in the tissue diagnostics market requires embracing digitalization, focusing on the patient-centric journey, and creating integrated solutions.

Strategic Recommendations for Stakeholders

Lead the Digital Transition: Manufacturers should shift from selling standalone scanners to offering comprehensive, integrated Digital Pathology Ecosystems (Scanner + Cloud/Storage + AI Analysis Platform). Subscriptions or pay-per-use models for software can lower the entry barrier for smaller labs.

Focus on Multimodal Diagnostics: Invest in technologies that allow for combined morphological, proteomic, and genomic information from the same slide. The future lies in Spatial Biology, providing a more complete picture of disease from a single sample.

Develop Regulatory-Ready AI: Prioritize the development and validation of AI algorithms for high-volume, repetitive tasks (e.g., PD-L1 scoring, mitosis counting) where regulatory approval provides the fastest return on investment and offers clear, quantifiable efficiency improvements to the user.

Strengthen Companion Diagnostics (CDx) Partnerships: For reagent manufacturers, securing exclusive partnerships with pharmaceutical companies during the early stages of drug development guarantees market share for the resulting CDx test, locking in future consumable revenue and maintaining high margins.

Browse More Reports:

Global Intelligent Power Distribution Unit (PDU) Market

North America Surgical Power Tools Market

Global Non-Invasive Cancer Diagnostics Market

Global Cerebral Vasospasm Market

Middle East and Africa Diet and Nutrition Apps Market

Asia-Pacific Polyimide Films Market

Global Offshore Drilling Market

Global Paragonimiasis Treatment Market

Middle East and Africa Surgical Power tools Market

Europe Sustainable Aviation Fuel Market

Global Cardiovascular Ultrasound System Market

Global Uterine Polyps Drug Market

Global Dental Consumables Market

Global Amusement Parks Market

Global Polyurethane Additives Market

Global Bottled Cocktail Market

Global Self-Adhesive Tear Tape Market

Global Nursing and Residential Care Market

Global Titanium Dioxide Market

Europe Biopreservation Market

Asia-Pacific Personal Care Ingredients Market

Global Yeast Infection Market

Asia-Pacific Unmanned Ground Vehicle Market

Global Shale Gas Processing Equipment Market

Global Veterinary Blood Lactate Test Meter Equipment Market

Asia-Pacific Commercial Cleaning Equipment Market

Asia-Pacific Retail Analytics Market

Europe Weight Loss and Obesity Management Market

North America Biopreservation Market

Global Automotive Emission Test Equipment Market

North America Hydrographic Survey Equipment Market

About Data Bridge Market Research:

An absolute way to forecast what the future holds is to comprehend the trend today!

Data Bridge Market Research set forth itself as an unconventional and neoteric market research and consulting firm with an unparalleled level of resilience and integrated approaches. We are determined to unearth the best market opportunities and foster efficient information for your business to thrive in the market. Data Bridge endeavors to provide appropriate solutions to the complex business challenges and initiates an effortless decision-making process. Data Bridge is an aftermath of sheer wisdom and experience which was formulated and framed in the year 2015 in Pune.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email:- corporatesales@databridgemarketresearch.com