Executive Summary

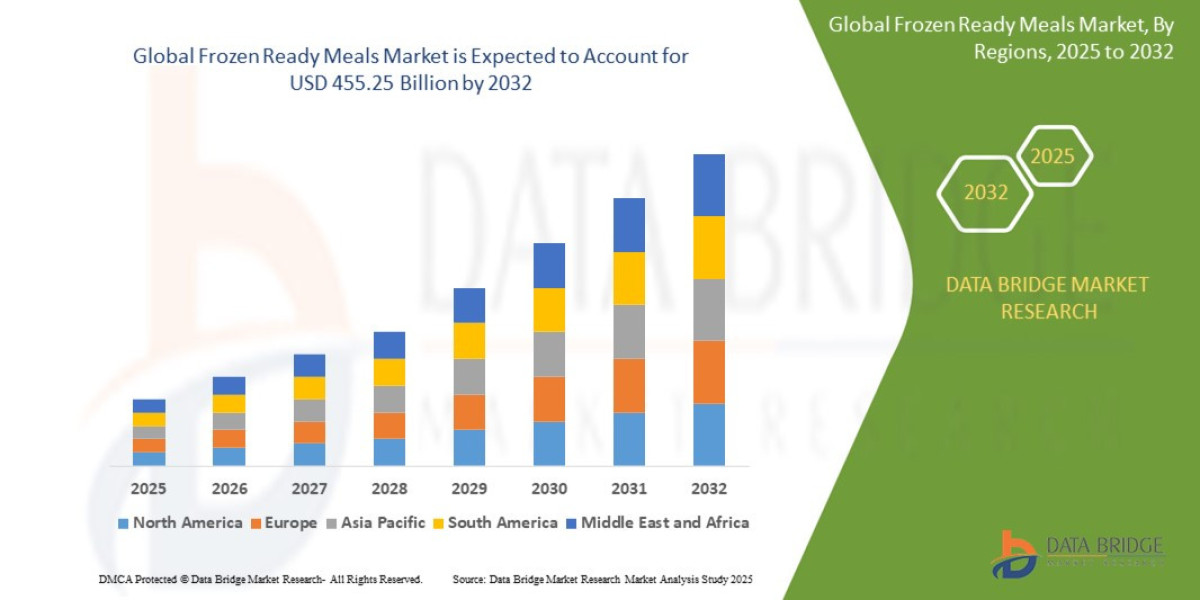

- The global frozen ready meals market size was valued at USD 298.9 billion in 2024 and is expected to reach USD 455.25 billion by 2032, at a CAGR of 5.40% during the forecast period

Market Overview

The Frozen Ready Meals Market encompasses pre-cooked, complete, or semi-prepared meals that require only reheating before consumption, preserved primarily through flash-freezing techniques.

Key Segments by Product Type

Frozen Entrees (Dominant Segment): Includes single-serve and multi-serve full meals (e.g., pasta dishes, ethnic curries, meat and vegetable combinations). This segment generates the highest revenue due to its convenience.

Frozen Appetizers and Sides: Smaller, supplementary items (e.g., spring rolls, potato skins, vegetable mixes) that complement the main meal or serve as snacks.

Frozen Breakfast Meals (Fastest Growing): Driven by the rise of convenient options like frozen breakfast burritos, pancakes, and smoothie kits, catering to fast-paced morning routines.

Frozen Desserts: Although often tracked separately, pre-portioned frozen dessert items frequently cross-sell with ready meals.

Key Segments by Distribution Channel

Supermarkets/Hypermarkets (Core Channel): Dominant due to large freezer aisles, bulk purchasing, and impulse buying.

Online Retail/E-commerce: Rapidly growing, especially for specialty, direct-to-consumer (DTC) brands focusing on subscription boxes and niche dietary categories (e.g., paleo, keto).

Drivers and Current Dynamics

Core Market Drivers:

Time Poverty and Convenience: The single most critical driver; increasing dual-income households and busy lifestyles make speed and minimal preparation essential.

Product Premiumization: Consumers are increasingly willing to pay a premium for high-quality, recognizable ingredients, and complex ethnic flavor profiles that replicate restaurant experiences.

Cold Chain Infrastructure Improvement: Enhanced global cold chain logistics reduce spoilage risk and allow for the efficient distribution of frozen goods even in emerging markets.

Current Dynamics: The market is in a phase of "health remix," where manufacturers are actively reformulating classic dishes to reduce sodium, saturated fats, and artificial additives. This is creating a competitive split between traditional comfort food brands and agile startups focused purely on the functional, clean-label niche.

Market Size & Forecast

- The global frozen ready meals market size was valued at USD 298.9 billion in 2024 and is expected to reach USD 455.25 billion by 2032, at a CAGR of 5.40% during the forecast period

For More Information Visit https://www.databridgemarketresearch.com/reports/global-frozen-ready-meals-market

Key Trends & Innovations

Innovation is focused on preserving nutritional quality, improving texture, and enhancing the consumer experience through technology.

1. Advanced Freezing Technologies

Manufacturers are moving beyond traditional air blast freezers to techniques that minimize ice crystal formation and preserve cellular structure, thus maintaining flavor and texture closer to fresh:

Cryogenic Freezing: Using liquid nitrogen or carbon dioxide to achieve rapid freezing, critical for seafood and complex sauces.

High-Pressure Processing ($\text{HPP}$): While primarily used for non-frozen goods, $\text{HPP}$ is being studied for its potential to improve the shelf life and sensory quality of certain pre-cooked components before freezing.

2. Clean Label and Ingredient Transparency

The push for clean labels necessitates removing ingredients like monosodium glutamate ($\text{MSG}$), artificial colors, and unnecessary stabilizers.

Focus on Whole Ingredients: Marketing emphasizes recognizable ingredients and simple cooking methods (e.g., "oven-roasted chicken," "hand-chopped vegetables") to build trust.

Allergen and Dietary Specialization: Dedicated lines for gluten-free, dairy-free, and nut-free meals, often validated by third-party certification bodies.

3. Smart and Sustainable Packaging

Packaging innovation aims to improve cook quality and reduce environmental impact:

Dual-Ovenable and Self-Venting Trays: Designing containers that manage steam and heat distribution in the microwave to prevent uneven cooking or 'hot spots.'

Recyclable and Compostable Trays: The transition from black $\text{CPET}$ (often undetectable by waste sorting machines) to recyclable white/clear $\text{CPET}$ or fiber-based, compostable trays to meet consumer sustainability demands.

Competitive Landscape

The market is characterized by intense competition between entrenched CPG giants, private label brands, and innovative startups carving out specialized niches.

Major Players and Strategic Strategies

Global $\text{CPG}$ Leaders (e.g., Nestlé, Conagra Brands, Nomad Foods): Strategy is Portfolio Dominance and Scale. They leverage vast manufacturing footprints and established cold chains to maintain high volume, and they continuously acquire smaller, trend-setting brands (e.g., ethnic or plant-based) to integrate innovation quickly.

Private Label Brands (Retailer-Owned): Strategy is Price and Value. Private label growth is significant, offering lower-priced alternatives to national brands, often focusing on core, simple entrees to gain market share in price-sensitive demographics.

DTC/Specialty Startups (e.g., Territory Foods, Factor): Strategy is Niche Focus and Customization. They bypass traditional retail to focus on specific, high-end demographics (e.g., diet delivery for athletes, personalized meal plans), utilizing sophisticated subscription models and direct customer feedback for agile product development.

The key competitive battleground is the freezer door real estate in supermarkets, where visual appeal and brand trust are paramount.

Regional Insights

Consumption patterns and growth drivers vary significantly based on cultural meal habits and the maturity of the cold chain.

North America (Premiumization and Functional Focus)

Performance: A massive, high-consumption market driven by convenience. It leads the world in adopting functional, health-focused, and specialized meals (e.g., keto, diabetic-friendly).

Opportunity: The rise of single-person households and the lunch occasion (replacing restaurant lunch) drive demand for premium single-serve options.

Europe (High Quality and Sustainability)

Performance: A mature market with strong preferences for quality, natural ingredients, and low-waste packaging. The UK, France, and Germany are key markets.

Opportunity: Strong regulatory and consumer push for sustainable sourcing and transparent supply chains offers an advantage to brands that invest in local, traceable ingredients.

Asia-Pacific (APAC) (Infrastructure-Driven Growth)

Performance: Traditionally low per-capita consumption, but experiencing explosive growth due to rapid urbanization, increasing female labor participation, and the development of modern retail infrastructure (including the cold chain).

Opportunity: Huge potential for localization, adapting frozen formats to popular regional dishes and using rice-based or noodle-based entrees to target mass-market consumers.

Challenges & Risks

The frozen ready meals sector faces technological and perceptual hurdles that threaten its expansion, particularly concerning quality and environmental impact.

1. Perceptual Barriers: Taste and Nutrition

Despite technological advancements, many consumers still perceive frozen meals as inferior in taste and nutritional value compared to fresh or scratch-cooked meals. Overcoming the "high sodium, bland food" stereotype requires continuous and visible $\text{R \& D}$ investment.

2. Cold Chain Reliance and Energy Costs

The market is entirely dependent on an unbroken cold chain from production to the consumer's freezer. Any lapse risks food safety and product quality. Furthermore, the high energy consumption of freezing, storage, and transport increases operational costs and the overall carbon footprint, making sustainability targets challenging.

3. High Barrier to Entry for Production

Manufacturing requires significant capital investment in $\text{IQF}$ (Individual Quick Freezing) tunnels, specialized packaging equipment, and large-scale refrigerated warehousing, making rapid scaling difficult for small, innovative startups.

4. Regulatory Scrutiny on $\text{FOP}$ Labeling

Increasing global pressure for Front-of-Pack ($\text{FOP}$) warning labels (like Nutri-Score in Europe) targets high-salt or high-fat prepared meals, forcing mass-market brands to undertake costly, widespread ingredient reformulation.

Opportunities & Strategic Recommendations

Success requires aggressive investment in technology that simultaneously improves convenience, health, and flavor authenticity.

Strategic Recommendations for Stakeholders

Prioritize $\text{IQF}$ and Sensory R&D (Manufacturers): Invest heavily in advanced freezing methods and high-quality ingredients that retain texture and color after freezing and reheating (e.g., flash-frozen vegetables, par-cooked grains). This is the only way to genuinely justify the premium price point in the health-conscious segments.

Acquire or Incubate DTC Health Brands (CPG Leaders): Instead of slowly reformulating legacy brands, $\text{CPG}$ giants should aggressively acquire successful, digitally native $\text{DTC}$ brands (like those focusing on vegan or fitness meals). This provides instant credibility, access to higher-margin consumers, and agile product development cycles.

Invest in Regional Cold Chain Partnerships (Global Expansion): In high-growth APAC and Latin American markets, partner with specialized third-party logistics (3PL) providers to ensure last-mile delivery integrity, rather than relying solely on in-house cold chain networks, mitigating risk and capital outlay.

Embrace Transparency and Storytelling (Marketing): Use $\text{QR}$ codes on packaging to provide consumers with video content showing the meal being prepared (the "scratch-cooked" process), the origin of key ingredients, and the nutritional breakdown, directly combating the perceptual barrier of 'processed' food.

Browse More Reports:

Europe Flotation Reagents Market

Global Wearable Fitness Trackers Market

Global Industrial Hearable Market

Global Micro Tube Box Market

Global Perimeter Defence System Market

Global Printed Textile Market

Italy Dental Practice Management Software Market

Global Smart Factory Market

India Food Ingredients Market

Europe q-PCR Reagents Market

Global NAND Flash Memory Market

Europe Food Bags Market

Global Wax and Wax Esters Market

Global Micro-Electromechanical Systems (MEMS) Gyroscopes Market

Middle East and Africa Probe Card Market

Global Injection Trays Market

Global Cord Blood and Cell Banking Market

Europe Protein Hydrolysates Market

Global Laminated Veneer Lumber Market

Middle East and Africa Wind Turbine Pitch System Market

Global Commercial Cleaning Equipment Market

North America Protein Hydrolysates Market

Middle East and Africa Rotomolding Market

Global (GPS) Global Positioning Systems Market

Global Sever’s Disease Treatment Market

Australia Specialty Gas Market

Global Below Grade Waterproofing Membrane Market

Middle East and Africa Intensive Care Unit (ICU) Ventilators Market

Global Beeswax Market

Europe Commercial Cleaning Equipment Market

Global Flooring and Carpets Market

About Data Bridge Market Research:

An absolute way to forecast what the future holds is to comprehend the trend today!

Data Bridge Market Research set forth itself as an unconventional and neoteric market research and consulting firm with an unparalleled level of resilience and integrated approaches. We are determined to unearth the best market opportunities and foster efficient information for your business to thrive in the market. Data Bridge endeavors to provide appropriate solutions to the complex business challenges and initiates an effortless decision-making process. Data Bridge is an aftermath of sheer wisdom and experience which was formulated and framed in the year 2015 in Pune.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email:- corporatesales@databridgemarketresearch.com