Executive Summary

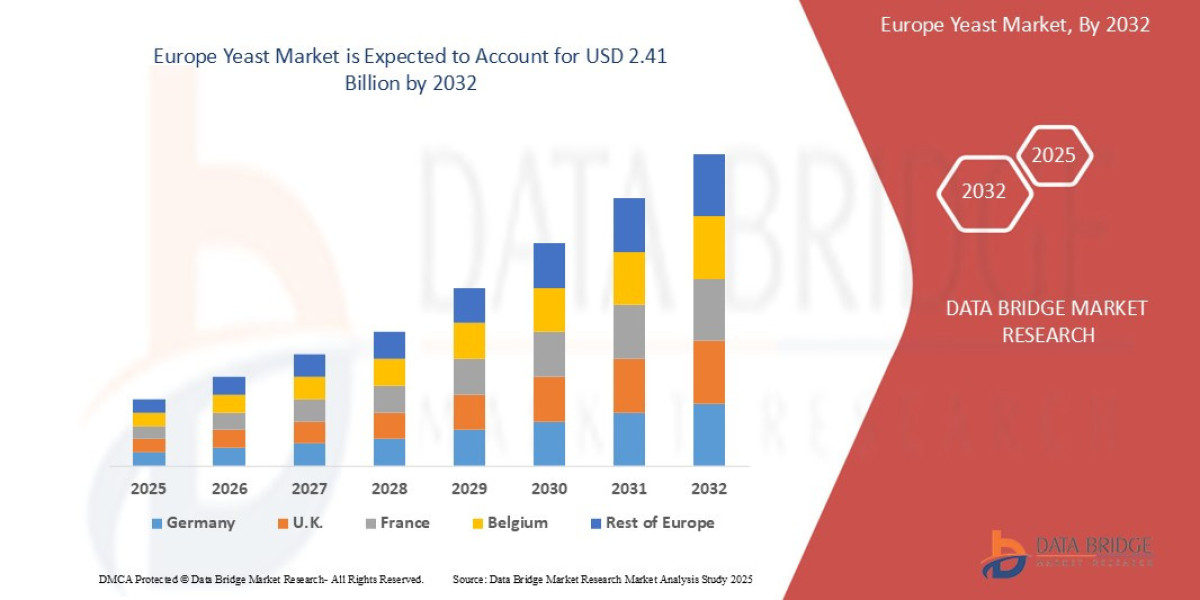

- The Europe Yeast market size was valued at USD 1.67 billion in 2024 and is expected to reach USD 2.41 billion by 2032, at a CAGR of 4.70% during the forecast period

Market Overview

The Europe Yeast Market covers the production, distribution, and application of various strains of the single-celled fungus Saccharomyces cerevisiae and other related species. The market serves as a cornerstone of the European food, feed, and biotech industries, underpinned by strict food safety and production regulations.

Key Market Segments by Type:

Baker’s Yeast: The largest volume segment, including compressed, active dry, and instant yeast. Its demand is stable, tied directly to the consumption of bread and other baked goods, particularly in Mediterranean and Western European nations.

Brewer’s Yeast: Essential for the fermentation of beer. Its growth is influenced by the craft beer movement and the demand for specialized, regional strains.

Feed Yeast: Increasingly vital, used as a protein source and functional ingredient (probiotics, prebiotics, and beta-glucans) to improve animal health, particularly in poultry and swine, reducing the reliance on antibiotics.

Food & Nutritional Yeast: This segment, including yeast extract (a savory, umami-rich flavoring agent) and inactive nutritional yeast (a source of B vitamins and complete protein), is the fastest-growing segment due to its appeal in vegan, vegetarian, and clean-label products.

Key Market Drivers:

Clean Label and Natural Ingredients: European consumers, particularly in Western Europe, demand food products with transparent, recognizable ingredients. Yeast and its extracts are highly favored as natural flavor enhancers over synthetic alternatives (e.g., MSG).

Expansion of Plant-Based Diets: Yeast extracts provide the necessary depth of flavor (umami) to replace meat, making them indispensable in the formulation of plant-based meats, soups, and ready meals. Nutritional yeast is also a staple protein source for vegan consumers.

Sustainable Animal Nutrition: Regulatory pressure to reduce antibiotic usage in livestock farming drives demand for functional feed yeasts that boost animal immunity and gut health.

Current Market Dynamics:

The market is characterized by regional concentration of production, dominated by major global players with deep historical roots in Europe. There is an increasing focus on the vertical integration of the supply chain, from molasses sourcing (the primary fermentation medium) to specialized application research centers, ensuring product consistency and raw material stability.

Market Size & Forecast

- The Europe Yeast market size was valued at USD 1.67 billion in 2024 and is expected to reach USD 2.41 billion by 2032, at a CAGR of 4.70% during the forecast period

For More Information visit https://www.databridgemarketresearch.com/reports/europe-yeast-market

Key Trends & Innovations

Innovation in the European yeast market is moving rapidly beyond traditional fermentation processes, focusing on sustainability, advanced nutrition, and bio-industrial applications.

1. The Rise of Savory Yeast Extracts (Umami): This is arguably the most impactful trend. Yeast extracts (YE) are rapidly replacing traditional flavor enhancers in processed foods. The innovation lies in optimizing fermentation conditions (using specialized nutrient feeds and enzymatic hydrolysis) to maximize the concentration of natural glutamates and nucleotides, resulting in cleaner, more potent umami and kokumi (mouthfeel) profiles for manufacturers of high-end snacks and vegan protein products.

2. Non-Conventional Yeast Strains (Oleaginous Yeasts): The search for sustainable alternatives to traditional oils is driving research into oleaginous yeasts (e.g., Yarrowia lipolytica and Pichia pastoris). These strains can be engineered to convert low-cost substrates (like agricultural waste or methanol) into microbial lipids, which can be used to produce bio-oils, sustainable aviation fuel, or as a source of Omega-3 fatty acids for supplements.

3. Single-Cell Protein (SCP) for Feed: A significant trend in feed applications is the mass production of yeast biomass as Single-Cell Protein. This highly efficient process converts industrial byproducts into high-quality protein, which is then dried and incorporated into aquaculture and livestock feeds, providing a sustainable, non-GMO alternative to soy meal.

4. Advanced Genetic Engineering (Precision Fermentation): European biotech firms are increasingly utilizing CRISPR-Cas9 and other gene editing tools to modify yeast strains. This "precision fermentation" allows manufacturers to program yeast to produce specific, high-value molecules—such as customized enzymes, specialized dietary fibers, or rare cannabinoids—at scale, turning the yeast cell into a tiny, efficient bio-factory.

Competitive Landscape

The European yeast market is moderately consolidated, with strong historical players maintaining dominance through scale, long-standing customer relationships, and continuous technological innovation.

Major Global Players (with strong European Heritage):

Lesaffre (France): The global market leader, Lesaffre holds a commanding presence across all segments (baker’s, nutritional, and health). Its strategy centers on aggressive geographic expansion and diversification into savory flavors and human health ingredients.

Lallemand (Canada/Europe): Strong in specialty segments, particularly wine, brewing, and animal nutrition (probiotics and inoculants). Lallemand maintains a strategy of targeted acquisitions to secure proprietary strains and application expertise.

Angel Yeast (China/Europe): A major global entrant that has established a significant footprint in Europe, focusing heavily on yeast extracts and nutritional yeast, often competing aggressively on price and efficiency.

Associated British Foods (ABF) (UK): A dominant player primarily in the baker’s yeast market through its various subsidiaries (e.g., AB Mauri), leveraging its extensive ties with industrial baking operations.

Competitive Strategies:

M&A and Capacity Expansion: Major firms are actively acquiring smaller, specialized yeast extract and nutritional companies to absorb niche expertise and proprietary fermentation technologies. There is also continuous capital investment to expand cold storage and drying capacity across Central and Eastern Europe.

Application-Specific R&D: Competition is shifting from price wars to differentiation through application support. Leading companies run specialized baking, brewing, and feed research centers to co-develop products with customers, optimizing the yeast strain for the customer's specific process (e.g., high-speed industrial mixing).

Sustainability and Traceability: Companies are differentiating by proving their sustainability credentials, including certified sourcing of raw materials, energy efficiency in fermentation, and waste valorization (turning spent yeast into animal feed or fertilizer).

Regional Insights

Europe is not a monolithic market; performance and opportunities vary significantly across major regional clusters.

Western Europe (France, Germany, UK, Benelux)

Characteristics: This is the most mature segment, characterized by high production capacity and the most sophisticated consumption patterns. It is dominated by premium, specialty, and nutritional yeast products.

Key Focus: High-value segments like yeast extracts for the savory and plant-based food industry, and specialized wine/brewing yeast for premium alcoholic beverages.

Opportunity: Strong regulatory drive toward antibiotic reduction, making this a prime area for high-performance feed yeast and immune-boosting derivatives.

Central and Eastern Europe (Poland, Russia, Ukraine)

Characteristics: This region offers significant growth potential, driven by lower consumption rates but rapidly increasing demand for processed food and improved animal feed. It is a lower cost-of-production zone.

Key Focus: Growth is centered on bulk baker's yeast for industrial bread production and standard feed yeast to support large-scale poultry and swine operations.

Opportunity: Capacity expansion for new production facilities, leveraging the lower operational costs and proximity to major agricultural raw material sources (molasses).

Southern Europe (Italy, Spain)

Characteristics: Highly influential in specialty yeast, particularly in winemaking. Traditional baking practices maintain consistent demand for high-quality, fresh baker's yeast.

Key Focus: Premium oenology (wine) yeasts, where regional terroir demands highly specific strains to achieve desired flavor profiles, and fermentation solutions for traditional food products (e.g., sourdough starters).

Opportunity: Development of stress-resistant yeast strains for winemaking to cope with climate change-induced high temperatures and sugar levels in grapes.

Challenges & Risks

Despite the favorable market outlook, the European yeast industry faces several persistent risks and structural challenges.

1. Raw Material Price Volatility: Molasses, a key byproduct of the sugar industry and the dominant fermentation feedstock, is subject to extreme price volatility influenced by global sugar harvests, biofuel demand, and trade policies. This fluctuation makes consistent cost management difficult for large-volume yeast manufacturers. Finding and utilizing alternative, non-molasses substrates (like wood pulp sugars or starch hydrolysates) remains costly and technologically challenging.

2. High Energy and Utility Costs: The fermentation and downstream processing of yeast (drying, cooling, sterilization) are highly energy-intensive. Europe’s relatively high industrial energy prices significantly pressure operating margins compared to production centers in Asia or North America. This necessitates heavy investment in energy recovery and efficient drying technologies.

3. Regulatory Hurdles for Novel Yeast Products: The use of genetically modified (GM) or genetically engineered (GE) yeast strains, even when used only to produce non-GM final ingredients (precision fermentation), faces slow and complex approval processes under EU novel food regulations. Public perception in Europe remains wary of engineered ingredients, posing a commercialization risk for cutting-edge biotech applications.

4. Competition from Alternative Flavorings: Although yeast extracts are popular, they face increasing competition from other naturally derived umami sources, such as vegetable protein hydrolysates and fermentation-derived savory compounds, forcing yeast manufacturers to continually improve cost-in-use and flavor potency.

Opportunities & Strategic Recommendations

The confluence of consumer demand for natural ingredients and technological breakthroughs offers significant strategic opportunities for stakeholders across the value chain.

For Manufacturers & 3PLs:

Vertical Integration of Molasses Supply: Secure long-term, fixed-price contracts or invest directly in sugar processing facilities to mitigate raw material price risk and ensure a stable supply of high-quality fermentation feedstock.

Focus on the Nutritional/Functional Segment: Shift investment priority away from commodity baker's yeast toward specialized, high-margin functional ingredients like yeast beta-glucans (for immune health supplements) and selenium-enriched yeast (for specialized nutrition), which command premium pricing in the pharma and nutraceutical space.

Digitally Enabled Traceability: Implement blockchain or similar digital ledger systems to provide end-to-end traceability of specialty yeast strains from the fermentation tank to the final consumer product, fulfilling the clean-label promise and enhancing trust.

For Investors & Startups:

Waste-to-Protein Platforms: Target R&D into converting low-cost industrial byproducts (e.g., agricultural waste streams, distillery waste) into yeast-based Single-Cell Protein (SCP). This aligns with the European Union’s circular economy goals and addresses the critical need for sustainable local protein sources.

Precision Fermentation Platforms: Invest in startups focused on developing and scaling up non-conventional yeast fermentation for producing high-value, rare ingredients (e.g., rare sugars, natural pigments, or novel enzymes) as an advanced method of chemical synthesis.

Browse More Reports:

Global Intelligent Power Distribution Unit (PDU) Market

North America Surgical Power Tools Market

Global Non-Invasive Cancer Diagnostics Market

Global Cerebral Vasospasm Market

Middle East and Africa Diet and Nutrition Apps Market

Asia-Pacific Polyimide Films Market

Global Offshore Drilling Market

Global Paragonimiasis Treatment Market

Middle East and Africa Surgical Power tools Market

Europe Sustainable Aviation Fuel Market

Global Cardiovascular Ultrasound System Market

Global Uterine Polyps Drug Market

Global Dental Consumables Market

Global Amusement Parks Market

Global Polyurethane Additives Market

Global Bottled Cocktail Market

Global Self-Adhesive Tear Tape Market

Global Nursing and Residential Care Market

Global Titanium Dioxide Market

Europe Biopreservation Market

Asia-Pacific Personal Care Ingredients Market

Global Yeast Infection Market

Asia-Pacific Unmanned Ground Vehicle Market

Global Shale Gas Processing Equipment Market

Global Veterinary Blood Lactate Test Meter Equipment Market

Asia-Pacific Commercial Cleaning Equipment Market

Asia-Pacific Retail Analytics Market

Europe Weight Loss and Obesity Management Market

North America Biopreservation Market

Global Automotive Emission Test Equipment Market

North America Hydrographic Survey Equipment MarketAbout Data Bridge Market Research:

An absolute way to forecast what the future holds is to comprehend the trend today!

Data Bridge Market Research set forth itself as an unconventional and neoteric market research and consulting firm with an unparalleled level of resilience and integrated approaches. We are determined to unearth the best market opportunities and foster efficient information for your business to thrive in the market. Data Bridge endeavors to provide appropriate solutions to the complex business challenges and initiates an effortless decision-making process. Data Bridge is an aftermath of sheer wisdom and experience which was formulated and framed in the year 2015 in Pune.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email:- corporatesales@databridgemarketresearch.com