Executive Summary

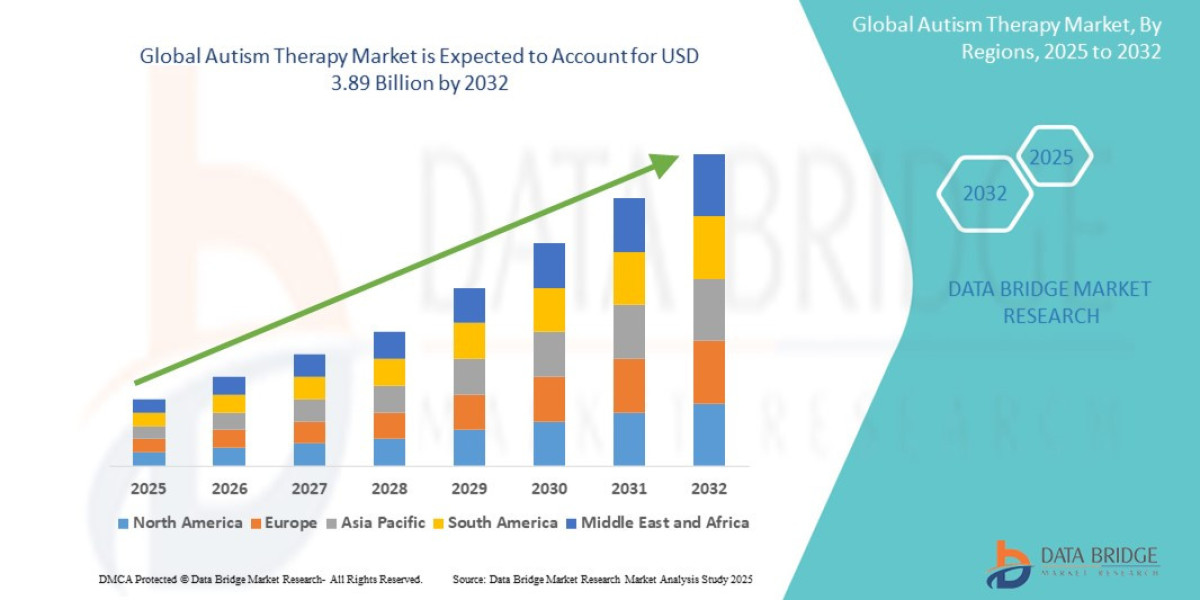

- The global autism therapy market size was valued at USD 2.33 billion in 2024 and is expected to reach USD 3.89 billion by 2032, at a CAGR of 6.60% during the forecast period

Market Overview

The Autism Therapy Market encompasses the full range of interventions, treatments, and supportive services designed to address the core characteristics of ASD, including challenges in social interaction, communication, and restricted/repetitive behaviors. The market focuses primarily on pediatric populations but is increasingly extending services to adolescents and adults.

Key Market Segments by Therapy Type:

Applied Behavior Analysis (ABA) Therapy: The gold standard and largest segment. ABA includes various techniques (e.g., Discrete Trial Training, Pivotal Response Training) and focuses on skill acquisition and behavior modification. It accounts for the majority of market revenue due to its robust evidence base and widespread insurance coverage.

Pharmacological Interventions: Covers prescription medications used to manage co-occurring conditions, such as irritability, aggression, anxiety, and Attention Deficit Hyperactivity Disorder (ADHD), which frequently complicate ASD. This includes antipsychotics (like risperidone and aripiprazole) and various off-label medications.

Adjunctive Therapies: A diverse segment including Speech-Language Pathology (SLP), Occupational Therapy (OT), Physical Therapy (PT), and Developmental, Individual Difference, Relationship-based (DIR/Floortime) approaches. These therapies often address specific motor, sensory, or communication deficits.

Key Market Drivers:

Rising Global Prevalence: The estimated prevalence of ASD continues to climb, with recent data in the U.S. suggesting rates of 1 in 36 children. This heightened incidence globally forms the fundamental demand driver.

Early and Universal Screening: Increased awareness, mandatory early childhood screening (e.g., using M-CHAT tools), and refined diagnostic criteria are leading to earlier intervention, which maximizes long-term positive outcomes and increases the total addressable market.

Insurance Coverage Mandates: In the U.S., state-level mandates requiring commercial insurance plans to cover ABA therapy have been crucial. Similar, though less unified, coverage improvements are emerging in other mature economies (e.g., select European countries and Australia).

Current Market Dynamics:

The market is undergoing a professionalization phase. Historically dominated by small, local clinics, the industry is now seeing aggressive capital investment from private equity, leading to the formation of large, multi-state or national therapy providers. This consolidation aims to standardize treatment quality, centralize administrative functions, and improve operational efficiency across disparate geographic regions.

Market Size & Forecast

- The global autism therapy market size was valued at USD 2.33 billion in 2024 and is expected to reach USD 3.89 billion by 2032, at a CAGR of 6.60% during the forecast period

For More Information Visit https://www.databridgemarketresearch.com/reports/global-autism-therapy-market

Key Trends & Innovations

The convergence of behavioral science and digital technology is rapidly reshaping how autism therapy is delivered, monitored, and optimized.

1. Telehealth and Remote Supervision: The most significant recent trend is the permanent integration of telehealth. Initially accelerated by the pandemic, telehealth now enables Board Certified Behavior Analysts (BCBAs) to supervise Registered Behavior Technicians (RBTs) remotely, particularly in rural or underserviced areas. It also facilitates parent training and consultation, improving family engagement and adherence to treatment protocols.

2. Digital Data Collection and EMR Platforms: Therapy providers are moving away from manual data collection. Specialized Electronic Medical Record (EMR) and practice management software (PMS) platforms are essential. These tools not only handle scheduling and billing but also automate data collection (e.g., measuring prompt dependency, behavior frequency), offering therapists immediate, objective data to adjust treatment plans dynamically.

3. Gamification and Virtual Reality (VR): Technology is being leveraged to improve engagement and generalization of skills. Virtual Reality (VR) is emerging as a powerful tool, providing safe, controllable environments for teaching complex social skills (e.g., job interviews, public speaking, navigating public transport) that are difficult to practice in real-world settings. Gamified therapy apps are also increasing motivation in younger children.

4. Personalized Intervention Planning (P-EBP): There is a regulatory and clinical push towards moving beyond one-size-fits-all ABA. The trend, known as Personalized Evidence-Based Practices (P-EBP), uses machine learning and detailed patient data analytics to identify which specific intervention methods are most effective for an individual patient based on their co-occurring conditions, genetic profile, and response history.

Competitive Landscape

The Autism Therapy Market presents a highly competitive, yet fragmented, structure dominated by the sheer number of local providers, while a few large platforms rapidly consolidate market share.

Major Competitive Segments:

Large, Private Equity-Backed Platforms: Companies like Centria Healthcare, Butterfly Effects, and others (often branded as national chains) are leading consolidation. Their strategy relies on centralized billing, standardized training, and aggressive expansion across state lines to maximize payer relationships and referral networks.

Regional Clinic Chains: Mid-sized providers that dominate specific metropolitan areas or smaller states. Their competitive edge is deep local community integration, strong relationships with pediatricians, and local school districts.

Adjunctive Therapy Specialists: Highly specialized clinics focusing solely on SLP or OT, which often partner with or operate adjacent to ABA centers to offer integrated, holistic care.

Technology/SaaS Vendors: Firms providing the EMR/PMS systems and specialized therapy content (e.g., data collection apps, gamified skill modules). These companies are critical enablers for the scaled growth of the major therapy platforms.

Competitive Strategies:

Acquisition and Consolidation: The primary strategy of large players is horizontal integration, acquiring smaller, well-regarded local clinics to immediately gain accredited staff, physical locations, and established patient panels.

Workforce Development: Given the severe labor shortage, competitive differentiation is increasingly based on superior clinical training programs, effective RBT recruitment/retention strategies, and creating clear professional development pathways for BCBAs.

Payer Contracting Expertise: Success is tied to the ability to secure favorable, long-term contracts with major commercial and governmental payers (e.g., Medicaid/Medicare). Large platforms leverage their scale to negotiate better reimbursement rates.

Regional Insights

Market maturity and growth dynamics are heavily dependent on local healthcare policy and funding mechanisms.

North America (U.S. and Canada)

Market Maturity: The U.S. is the most mature and largest market globally, almost entirely driven by state-level insurance mandates covering ABA. High average treatment costs and high availability of trained professionals (relative to other regions) define this market.

Opportunity: Focus on value-based care pilots, shifting from fee-for-service to outcome-based payment models to prove the long-term clinical and economic efficacy of intensive early intervention.

Canada: The market is more centralized, with provincial funding models leading to long waitlists and greater reliance on public services, creating opportunities for private, specialized clinics in major provinces.

Europe

Fragmentation: The European market is highly fragmented, with coverage varying dramatically. Countries like the UK (NHS) and Netherlands have established public funding pathways, while others, particularly in Southern and Eastern Europe, rely heavily on self-pay or non-mandated private insurance.

Key Focus: Strong growth potential in adjunctive and school-based therapies. ABA has lower penetration, but awareness and adoption are increasing.

Opportunity: Establishing multi-national platforms that can successfully navigate the diverse public health systems and insurance structures of different EU member states.

Asia Pacific (Australia, Japan)

Australia: Features robust government funding (National Disability Insurance Scheme - NDIS), creating a stable, high-growth environment focused on multidisciplinary support. This offers high opportunity for new providers and innovative service delivery models.

Japan: Characterized by established public support systems but conservative adoption of Western-style intensive ABA, focusing more on developmental and educational approaches. Opportunities exist for technology-enabled training and standardization.

Challenges & Risks

The explosive growth of the market is constrained by several structural barriers and risks.

1. Severe Labor Shortages: The single greatest challenge is the gap between demand for therapy hours and the available supply of qualified clinicians, especially RBTs (the front-line therapists) and BCBAs (the supervisors). This shortage drives up labor costs, restricts patient access, and limits the ability of clinics to expand.

2. Quality Control and Standardization: Rapid expansion through acquisition risks diluting clinical quality. Ensuring fidelity to evidence-based practice across a large, distributed workforce remains a persistent challenge, particularly in the face of pressure to meet high utilization targets set by financial sponsors.

3. Payer Scrutiny and Fraud Risk: As costs rise, payers (insurance companies) are increasing scrutiny on authorization processes, utilization review, and treatment documentation to prevent fraud, waste, and abuse. This necessitates major compliance and administrative investment by therapy providers.

4. Ethical Concerns and Evolving Practice: The ABA field is undergoing internal review regarding historical practices and ethical guidelines. Providers must continuously adapt their clinical models to emphasize client assent, trauma-informed care, and neurodiversity-affirming approaches to ensure ethical, patient-centric delivery.

Opportunities & Strategic Recommendations

Successfully navigating the market requires focusing on efficiency, quality, and expanding access through innovation.

For Therapy Providers (M&A Targets/PE Investors):

Invest in Scalable Workforce Infrastructure (The "Therapy Pipeline"): Develop accredited, in-house RBT training academies and apprenticeship programs. Use technology to automate RBT supervision and data analysis, maximizing the capacity of scarce BCBAs to handle more clients efficiently.

Integrated Telehealth Model: Move beyond simple virtual sessions. Implement a hybrid model where initial assessment and high-intensity direct care are in-person, but parent training, BCBA supervision, and certain adjunctive services (like SLP) are delivered remotely, increasing geographical reach and reducing overhead.

For Technology and SaaS Vendors:

Develop AI-Powered Documentation Tools: Create AI assistants that can listen to or transcribe therapy sessions and automatically draft progress notes and regulatory documentation (ICD-10/CPT coding suggestions). This directly addresses the BCBA administrative burden, which can consume up to 30% of their time.

Focus on Adult Transition Services: Develop platforms and curricula (e.g., VR simulations) specifically aimed at teaching high-functioning adolescents and young adults job readiness, financial literacy, and social navigation skills, addressing the massive unmet need in the post-school transition phase.

For Pharmaceutical and Biotech Firms:

Target Core Symptom Mechanisms: Invest heavily in R&D aimed at pharmacological treatments that address the core deficits of ASD (e.g., social communication) rather than just co-occurring conditions. Precision medicine approaches leveraging genetic and biomarker data are key to unlocking this opportunity.

Integrate Digital Therapeutics (DTx): Partner with or acquire DTx companies that provide software-based interventions (e.g., cognitive training apps) that can be prescribed alongside medication or behavioral therapy, offering novel revenue streams and enhancing treatment efficacy.

Browse More Reports:

Global 3D Printing Construction Market

North America Rowing Boats and Kayaks Market

Middle East and Africa pH Sensors Market

Global Food Bags Market

Global Gasification Clean Coal Market

Global Immuno-Oncology Clinical Trials Market

Global Industrial Plastic Market

Global Gas Fire Table Market

Europe Plant Based Protein Market

Europe Bridge Bearings Market

Global Rail Public Transport Market

Global Sensor Data Analytics Market

Saudi Arabia Building Thermal Insulation Market

Global Low Profile Additives Market

Kenya, Uganda, Tanzania, and Rwanda Potato Processing Market

Global Endovascular Stent Grafts Market

Global Honeycomb Packaging Market

Global De Quervain's Tenosynovitis Treatment Market

Global Concrete Admixture Market

North America Microgrid Market

Global Organic Personal Care Products Market

Global IoT Security Market

North America Infection Surveillance Solution Systems Market

Global Hydrogen Sensor Market

East and Africa Unmanned Ground Vehicle Market

Global Soil Monitoring System Market

Middle East and Africa (MEA) Sludge Treatment Chemicals Market

Global Polycaprolactone (PCL) Market

Global Prenatal Genetic Counselling Market

Global Remote Sensing Infrared Light Emitting Diode (LED) Market

North America Plant-Based Milk Market

About Data Bridge Market Research:

An absolute way to forecast what the future holds is to comprehend the trend today!

Data Bridge Market Research set forth itself as an unconventional and neoteric market research and consulting firm with an unparalleled level of resilience and integrated approaches. We are determined to unearth the best market opportunities and foster efficient information for your business to thrive in the market. Data Bridge endeavors to provide appropriate solutions to the complex business challenges and initiates an effortless decision-making process. Data Bridge is an aftermath of sheer wisdom and experience which was formulated and framed in the year 2015 in Pune.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email:- corporatesales@databridgemarketresearch.com