Executive Summary

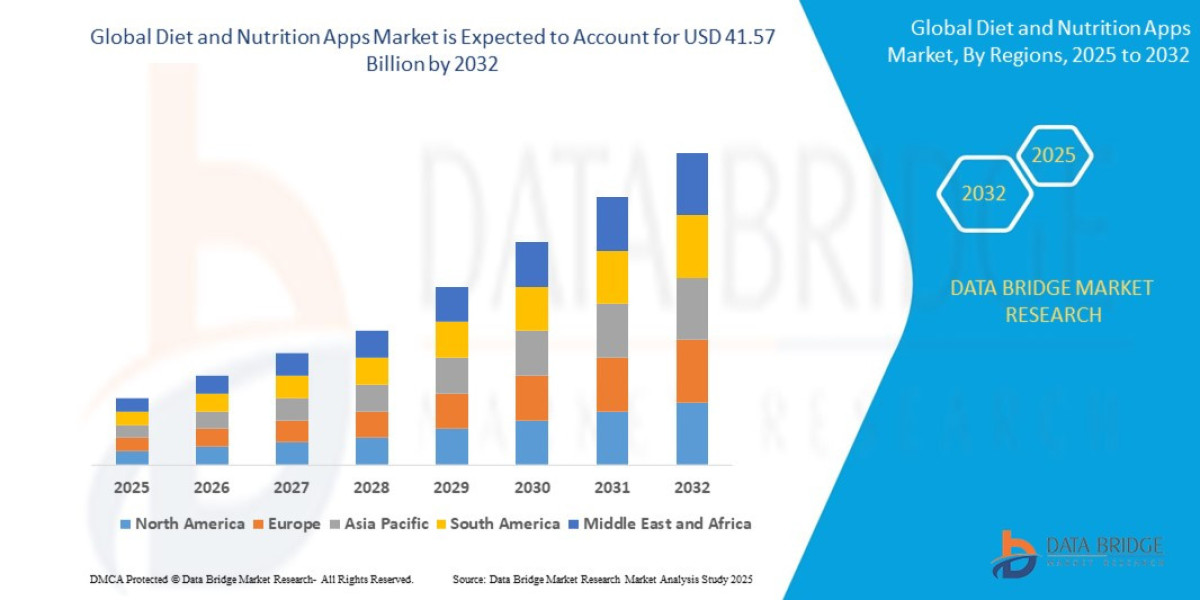

- The global diet and nutrition apps market was valued at USD 11.35 billion in 2024 and is expected to reach USD 41.57 billion by 2032

- During the forecast period of 2025 to 2032 the market is likely to grow at a CAGR of 17.61%

Market Overview

The Diet and Nutrition Apps Market encompasses mobile applications designed to track food intake, calculate calories and macronutrients, provide personalized meal plans, and offer behavioral coaching and professional dietitian support. These applications serve as the primary digital interface for self-monitoring and guided behavioral change related to dietary habits.

Key Market Segments by Application Focus:

Calorie & Macro Tracking Apps: The foundational segment (e.g., MyFitnessPal, Cronometer). Focuses on detailed food databases and historical tracking. Revenue is typically freemium, driven by premium features like advanced analytics or ad-free experiences.

Behavioral & Coaching Platforms: High-value segment (e.g., Noom). Emphasizes psychological and motivational coaching, often integrating human or AI coaches. This segment commands high subscription fees due to its intensive support model.

Meal Planning & Recipe Apps: Focuses on prescriptive action (e.g., PlateJoy, Forks Over Knives). Provides structured recipes and shopping lists tailored to specific dietary needs (e.g., Keto, Paleo, low-FODMAP).

Clinical/Specialized Apps (DiGAs): Emerging segment targeting specific conditions like Type 2 Diabetes, hypertension, or inflammatory bowel disease (IBD). Requires clinical validation and often seeks regulatory approval (e.g., FDA/CE Mark) for prescription use.

Key Market Drivers:

Rising Chronic Disease Burden: The escalating global prevalence of obesity and diabetes necessitates cost-effective, scalable, and personalized dietary interventions that apps are ideally positioned to deliver.

Democratization of Health Information: Apps make professional dietary guidance accessible and affordable, bypassing the high cost and geographical barriers associated with in-person dietitian consultations.

Ubiquity of Wearables: The seamless integration with smartwatches (Apple Watch, Fitbit) and specialized biometric devices (e.g., Continuous Glucose Monitors - CGMs) provides rich, actionable, and real-time data, enhancing personalization.

Digital Health Infrastructure Investment: Increased funding from venture capital and corporate mergers focused on digital health platforms (telehealth, remote monitoring).

Current Market Dynamics:

The market is undergoing rapid vertical integration. Coaching platforms are acquiring or partnering with content providers, and pure tracking apps are racing to integrate AI-powered coaching to avoid becoming commoditized. The most significant dynamic is the transition from a purely Consumer-to-Business (C2B) revenue model to a Business-to-Business (B2B) model, where payers and employers cover subscription costs to manage population health risks.

Market Size & Forecast

- The global diet and nutrition apps market was valued at USD 11.35 billion in 2024 and is expected to reach USD 41.57 billion by 2032

- During the forecast period of 2025 to 2032 the market is likely to grow at a CAGR of 17.61%

For More Information Visit https://www.databridgemarketresearch.com/reports/global-diet-and-nutrition-apps-market

Key Trends & Innovations

Technological advancements are moving apps from passive logging instruments to active, personalized intervention agents.

1. AI-Powered Hyper-Personalization and LLM Coaching: The integration of Large Language Models (LLMs) and advanced AI is revolutionizing coaching. AI now moves beyond simple template responses to provide contextual, empathetic, and personalized behavioral nudges and dietary advice that mimics human interaction. AI is also powering image recognition technology, allowing users to simply take a picture of their meal for immediate calorie and macro estimation, significantly reducing logging friction.

2. Clinical Validation and Digital Therapeutics (DiGAs): The most impactful trend is the formal use of nutrition apps as a medical treatment. In markets like Germany, apps can be approved as a Digital Health Application (DiGA), allowing them to be prescribed by doctors and reimbursed by statutory health insurance. This trend accelerates the market's professionalization, requiring rigorous clinical trial data (Randomized Controlled Trials - RCTs) to prove efficacy.

3. Biometric Integration (CGM, Genomics): Apps are deepening their integration with advanced biometric monitoring:

Continuous Glucose Monitors (CGMs): Non-diabetic users are adopting CGMs for personalized metabolic feedback. Apps ingest this data to provide real-time guidance on which foods cause the most severe glycemic spikes for that individual, leading to truly individualized meal planning.

Nutrigenomics: Integrating genetic testing data to provide diet plans optimized for an individual's unique genetic predispositions (e.g., carbohydrate sensitivity, vitamin absorption efficiency).

4. Ecosystem Development and Chronic Condition Focus: Instead of general weight loss, new entrants are specializing in chronic conditions where nutrition is paramount. Examples include apps tailored for renal diets, managing auto-immune disease flare-ups, or pre- and post-bariatric surgery care. This narrow focus allows for deep expertise and easier B2B penetration into specialized clinical networks.

Competitive Landscape

The market is fiercely competitive, characterized by high barriers to achieving long-term user retention, despite low barriers to initial entry.

Major Competitive Archetypes:

Legacy Trackers (e.g., MyFitnessPal, Lifesum): Competitive advantage is based on massive, proven food databases, large installed user bases, and strong brand awareness. Strategy involves rapid feature integration (AI, wearables) to defend against specialized competitors.

Behavioral Coaches (e.g., Noom, WW Digital): Competitive edge is proprietary behavioral science curricula, high user engagement, and a focus on long-term habit formation. Strategy relies on high-touch coaching and verifiable clinical outcomes to justify high ARPU.

Vertical Specialists (e.g., Levels, January AI): Highly innovative startups focused on specific technologies (like CGM data) or conditions (like metabolic health). Their strategy is to offer superior personalization and target niche, high-value consumer segments willing to pay premium prices for specialized data insights.

Competitive Strategies:

Data Network Effects: Winning players leverage large user data sets not just for personalization, but to improve the accuracy of their core food recognition and logging features, creating a positive feedback loop.

Outcome Validation: The primary battleground is shifting from marketing claims to clinical validation. Platforms that can publish peer-reviewed studies proving efficacy in areas like HbA1c reduction or sustained weight loss will dominate B2B and clinical channels.

Subscription Tier Optimization: Successful competitors use a tiered pricing structure: a free tier for basic logging, a mid-tier for premium features/AI coaching, and a high-tier for guaranteed access to human Registered Dietitians (RDs) or specialized medical services.

Regional Insights

Regional success is contingent upon local healthcare payment models, regulatory structures, and prevailing disease burdens.

North America (U.S. and Canada)

Market Characteristics: Highest revenue per user (ARPU), driven by significant private insurance coverage and a fragmented healthcare system. Corporate Wellness is a major channel, with employers subsidizing apps to reduce health insurance costs.

Strategic Focus: B2B integration (selling to payers and employers) and intense competition in the specialized metabolic health space, leveraging the high adoption rate of CGMs.

Europe (Germany, UK, Nordic Countries)

Market Characteristics: Highly receptive to digital health due to strong public health systems and clear regulatory pathways for DiGAs (especially in Germany and France). Data privacy (GDPR) is a major design constraint and competitive requirement.

Strategic Focus: Focus on clinical integration and achieving regulatory approval as a medical device to gain guaranteed public reimbursement, emphasizing secure, compliant data handling.

Asia Pacific (APAC)

Market Characteristics: Fastest-growing region, driven by massive mobile-first populations and a dramatic increase in Type 2 Diabetes rates (China, India). Lower ARPU necessitates a high-volume, low-cost delivery model.

Strategic Focus: Localization of food databases and language support is critical. Partnerships with local telecom providers and financial institutions are essential for mass distribution and payment processing. High-value opportunity in B2G (Business-to-Government) contracts for large-scale public health initiatives.

Challenges & Risks

Despite the growth potential, the market faces significant structural and user-centric challenges.

1. High User Churn and Lack of Engagement: The vast majority of users drop off within the first 90 days. The "New Year's Resolution" effect makes initial customer acquisition easy but long-term retention extremely difficult, resulting in high Customer Acquisition Costs (CAC) relative to Lifetime Value (LTV) for purely C2B models.

2. Data Accuracy and "Garbage In, Garbage Out": The foundation of these apps is user-logged data, which is often inaccurate due to estimation errors or user fatigue. This flawed input data can undermine the effectiveness of personalization algorithms and compromise clinical trust.

3. Regulatory and Liability Hurdles (DiGAs): Seeking FDA or CE Mark approval to operate as a medical device is costly, time-consuming, and subjects companies to significant liability. This barrier to entry prevents many smaller players from accessing the lucrative clinical B2B channel.

4. Ethical and Data Privacy Concerns: Nutrition apps collect some of the most sensitive personal data (weight, blood glucose, diagnoses). Misuse or inadequate protection of this data, especially when integrated with genetic or biometric profiles, poses severe legal and ethical risks under global privacy laws.

Opportunities & Strategic Recommendations

Success in this market requires a pivot toward clinical credibility, guaranteed outcomes, and deep, affordable behavior change support.

For App Developers and Startups:

Prioritize Clinical Validation (Outcome-Based Models): Design the app around specific, measurable clinical endpoints (e.g., weight reduction maintained for 12 months, lower LDL cholesterol). This shifts the revenue focus from consumer advertising to B2B contracts with payers who demand verifiable Return on Investment (ROI) in health outcomes.

Integrate LLMs for Scalable Coaching: Leverage sophisticated AI/LLM technology to provide 24/7, high-quality, personalized behavioral coaching at a fraction of the cost of human RDs. This is the key to scaling the high-touch service model affordably while maintaining a clear line for human professional escalation.

For Healthcare Providers and Payers:

Strategic M&A and Partnership: Acquire or partner exclusively with specialized nutrition apps that demonstrate efficacy in treating expensive chronic conditions (e.g., kidney failure, IBD). Integrate these apps directly into the payer's clinical pathways and Electronic Health Records (EHRs).

Focus on Hyper-Specialization: Instead of competing in the saturated general weight-loss category, focus on developing or funding apps for high-cost, unmet needs (e.g., personalized nutrition for oncology patients or specialized fertility diets). This targeted approach attracts high-paying, desperate customers and specialized clinical referrals.

For Technology Vendors:

Develop AI Food Recognition APIs: Focus on providing superior, high-accuracy AI food image recognition and logging APIs that third-party apps can license. Solving the "garbage in, garbage out" problem is a massive commercial opportunity.

Wearable Data Standardization: Develop infrastructure that securely and compliantly aggregates and normalizes data from disparate biometric devices (CGMs, smart scales, wearables) into a single, standardized feed that is easily ingestible by both patient-facing apps and clinical EHR systems.

Browse More Reports:

Global Small Molecule Sterile Injectable Drugs Market

Europe IoT Node and Gateway Market

Global Ophthalmic Anesthetic Drugs Market

Global Sustainable Aviation Fuel Market

North America Acute Lymphocytic/Lymphoblastic Leukemia (ALL) Diagnostics Market

Global Polymeric Nanoparticles Market

Global Acrylic Adhesives Market

Global Washing Appliances Market

Global Public Key Infrastructure (PKI) Market

Global GPS (Global Positioning System) Tracking System Market

North America Unmanned Ground Vehicle Market

North America Biometrics in Government Market

Global Gas Turbine Services Market

Global Energy Efficient Motor Market

Global Two Terminal Impact (Impact Ionization Avalanche Transit-Time) Diode Market

Global Antivirus Software Market

Middle East and Africa Polyimide films Market

Global Gene Expression Analysis Market

Global Genetic Testing Market

Global Food Ingredient Market

Global Ultra Soft Exoskeleton Market

Global Supercapacitor Market

Global Industrial Nitrogen Market

Global Mono-Material Packaging Market

Global Hematology Drugs Market

Global Polyethylene Implants Market

Global Dental Devices and Consumables Market

Global Ear Plugs and Bands Market

North America Commercial Cleaning Equipment Market

Global Rice Husk Ash Market

Global Data Integration Market

About Data Bridge Market Research:

An absolute way to forecast what the future holds is to comprehend the trend today!

Data Bridge Market Research set forth itself as an unconventional and neoteric market research and consulting firm with an unparalleled level of resilience and integrated approaches. We are determined to unearth the best market opportunities and foster efficient information for your business to thrive in the market. Data Bridge endeavors to provide appropriate solutions to the complex business challenges and initiates an effortless decision-making process. Data Bridge is an aftermath of sheer wisdom and experience which was formulated and framed in the year 2015 in Pune.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email:- corporatesales@databridgemarketresearch.com