Executive Summary

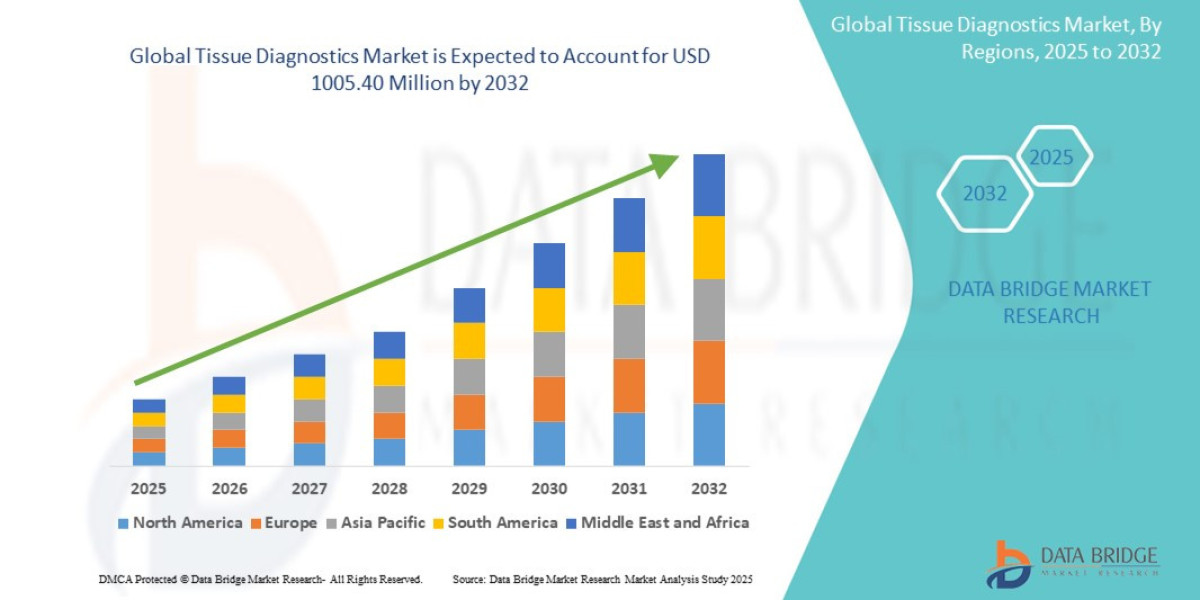

- The global tissue diagnostics market size was valued at USD 602.95 Million in 2024 and is expected to reach USD 1,005.40 Million by 2032, at a CAGR of 6.60% during the forecast period

Market Overview

Definition and Scope

Tissue Diagnostics encompasses the tools, technologies, and services used to prepare, stain, visualize, and analyze biological tissue samples. The process typically begins with tissue fixation and embedding, followed by microtomy, staining, and final examination by a pathologist.

Key Market Segmentation

By Product Type:

Consumables (Largest Segment): Includes primary antibodies, detection kits, special stains (H&E, PAS), and In Situ Hybridization (ISH) probes. This generates the bulk of recurring revenue.

Instruments: Comprises automated slide stainers (IHC/ISH), tissue processors, microtomes, and Whole Slide Imaging (WSI) scanners (the core component of Digital Pathology).

Software & Services (Fastest Growing): Includes Laboratory Information Systems (LIS), Image Analysis software, and AI algorithms for automated quantification and detection.

By Technology:

Immunohistochemistry (IHC): The most common technique, using antibodies to detect specific protein biomarkers (e.g., HER2, PD-L1).

In Situ Hybridization (ISH): Used to detect specific nucleic acid sequences (DNA or RNA) directly in the tissue section.

Digital Pathology (WSI & AI): The modern imaging and computational platform.

By Application:

Oncology (Dominant): Diagnosis, grading, and predictive biomarker testing (over 80% of market activity).

Neurology, Infectious Disease, and Autoimmune Disorders: Diagnosis and characterization in other disease areas.

Market Drivers

Explosion of Companion Diagnostics (CDx): Nearly all new oncology drugs require a specific CDx test (often IHC or ISH) to identify eligible patients. This directly links drug approval and prescribing volumes to diagnostics demand.

Rising Cancer Incidence: The aging global population and lifestyle factors continue to drive up cancer cases, directly increasing the volume of necessary biopsy and tissue testing procedures.

Pathologist Workflow Efficiency: Digital pathology offers significant efficiency gains (remote review, load balancing, collaboration) necessary to manage increasing case volumes amid a shortage of pathologists globally.

Standardization and Automation: Healthcare systems require standardized, reproducible testing. Automated stainers and AI software reduce inter-observer variability and human error, improving quality control.

Current Market Dynamics

The market is currently defined by a race for digital adoption. While the Instrument segment for automated stainers (IHC/ISH) is mature, the investment is rapidly accelerating in WSI scanners and, crucially, validated AI algorithms. Competition is fierce between established instrument manufacturers seeking to control the entire "glass-to-answer" ecosystem and nimble software start-ups specializing in AI image analysis.

Market Size & Forecast

- The global tissue diagnostics market size was valued at USD 602.95 Million in 2024 and is expected to reach USD 1,005.40 Million by 2032, at a CAGR of 6.60% during the forecast period

For More Information Visit https://www.databridgemarketresearch.com/reports/global-tissue-diagnostics-market

Key Trends & Innovations

1. Digital Pathology (DP) and Whole Slide Imaging (WSI)

The cornerstone of the market's transformation. WSI scanners digitize entire glass slides at high resolution, creating virtual slides. This enables:

Remote Consultation: Pathologists can review cases from anywhere, improving global consultation and resource management.

Archiving: Digital files replace cumbersome glass slide storage.

AI Readiness: The digital image is the necessary input for all advanced computational analysis.

2. Artificial Intelligence (AI) and Machine Learning (ML)

AI is moving from research curiosity to clinical tool. Key applications include:

Quantitative Scoring: Automating tasks like counting positive cells (e.g., Ki-67 scoring) or calculating tumor proportion scores (e.g., PD-L1), significantly reducing turnaround time and inter-observer variability.

Quality Control: Identifying poor-quality tissue sections or staining artifacts before they reach the pathologist.

Triage and Prioritization: Algorithms can flag complex cases or slides with high probability of malignancy for immediate pathologist review.

3. Multiplexing and Spatial Biology

As immuno-oncology requires deeper insight into the Tumor Microenvironment (TME), labs are moving beyond single-target IHC. Multiplex IHC (simultaneously staining for 3 to 10+ biomarkers on a single slide) is emerging. This is essential for understanding cell-to-cell interactions and spatial relationships of different immune cell types within the tumor, requiring specialized high-throughput instruments and advanced image analysis.

4. Integration of Liquid Biopsy

While not a tissue-based method, the liquid biopsy market (analyzing circulating tumor DNA/RNA) is highly complementary. The trend is toward an integrated diagnostic pathway where a non-invasive liquid biopsy screens for gross mutations, and tissue diagnostics (IHC/ISH) provide the definitive diagnosis and protein expression profile needed for treatment selection.

5. Automation and Standardization

Manufacturers are developing fully enclosed, automated workflow solutions (from tissue processing to staining and scanning) to reduce hands-on time, minimize cross-contamination risk, and achieve predictable, high-quality results across large hospital networks.

Competitive Landscape

The market is highly concentrated in the instrument and reagent segment, but highly fragmented in the emerging AI and software space.

Tier 1: Ecosystem Controllers (IHC/ISH/CDx)

Roche (Ventana Medical Systems): Dominant in automated IHC and ISH, leveraging a closed-system approach where its instruments are optimized for its high-margin reagents. Focuses heavily on co-developing CDx assays with pharmaceutical partners.

Danaher (Leica Biosystems): Strong in the traditional histology equipment space (microtomes, processors) and automated staining systems (Bond platform). Competing through open systems and flexible workflow solutions.

Agilent Technologies (Dako): A key player in CDx development and high-quality antibodies and reagents.

Tier 2: Digital and AI Specialists

Philips Healthcare, Hamamatsu, Visiopharm, PathAI: Leaders in WSI scanning technology (hardware) and increasingly, in the development of AI algorithms (software). Competition here centers on regulatory clearance (e.g., FDA De Novo clearance) for clinical use and interoperability with diverse pathology LIS systems.

Competitive Strategies Emphasized:

Closed Ecosystem Lock-In: Tier 1 players prioritize locking customers into their reagent supply through proprietary instrument platforms.

Clinical Validation & Regulation: The primary differentiator in AI is not just research performance but achieving regulatory approval for algorithms used in patient care (CDx).

Strategic Partnerships: WSI scanner companies (hardware) partner with AI firms (software) to offer integrated solutions, bridging the digital gap for clinical labs.

Regional Insights

North America (CDx and Early Digital Adopter)

North America accounts for the largest market share by value. This is driven by high cancer incidence, generous reimbursement for advanced molecular diagnostics, and the highest concentration of pharmaceutical companies driving CDx development. DP adoption is accelerating, primarily in large academic medical centers and reference labs.

Europe (Automation and Centralization)

Europe holds the second-largest share, with market growth driven by the need for standardization across centralized national health systems (e.g., NHS). There is high adoption of automated IHC stainers to manage increasing pathology workloads efficiently. Digital adoption is often tied to large regional pathology networks for streamlined cross-site workload balancing.

Asia-Pacific (Infrastructure Investment and Fastest Growth)

The APAC region is the fastest-growing market. This is spurred by massive government investment in modernizing healthcare infrastructure, rising cancer awareness, and increasing utilization of tissue-based diagnostics as healthcare quality improves. The region offers high-volume potential, especially for lower-cost, high-throughput solutions.

Challenges & Risks

1. Interoperability and Data Management

The biggest barrier to DP adoption is the lack of standardized data formats and vendor lock-in. Scanners, LIS systems, and AI algorithms often operate on proprietary platforms, hindering data sharing, archiving, and integration across the pathology workflow. WSI images also create massive data storage challenges.

2. Regulatory Bottleneck for AI

While AI algorithms show promise, the regulatory pathway for clinical-grade diagnostic AI tools is slow and complex, particularly when seeking FDA or CE-IVDR clearance for an algorithm that directly impacts patient treatment decisions (CDx).

3. High Initial Capital Outlay

The cost of converting an analog lab to a digital lab—including WSI scanners, servers, storage arrays, and LIS upgrades—requires significant upfront capital investment, which is a major barrier for smaller or community hospitals.

4. Skilled Personnel Resistance

The transition to digital pathology requires specialized IT expertise and involves a steep learning curve for many experienced pathologists, who must be trained to use WSI software and validate the output of new AI algorithms.

Opportunities & Strategic Recommendations

For Investors and Private Equity

Target AI as a Service (AIaaS): Invest in companies that offer AI algorithms on a subscription model, focused on achieving clinical regulatory clearance for common, high-volume tasks (e.g., PR/ER breast cancer scoring, HER2 counting). This generates predictable, high-margin software revenue.

Back Multiplexing Platforms: Focus on innovative platforms that enable high-plex spatial profiling of the TME, as pharmaceutical companies are increasingly demanding this high-resolution data for next-generation immuno-oncology drug development.

Fund LIS/Data Interoperability: Support firms creating vendor-agnostic cloud platforms or middleware to facilitate seamless data exchange between disparate WSI scanners and LIS systems, solving the industry's most critical non-technical challenge.

For Manufacturers and Service Providers

Develop Hybrid Solutions: Offer integrated solutions that allow labs to transition digitally in phases (e.g., scanning only complex cases initially) to lower the barrier to entry and upfront costs.

Prioritize Open Ecosystems: Instrument manufacturers should strategically move toward more open API architecture to allow third-party AI algorithm integration, increasing the value and longevity of their WSI hardware.

Focus on Point-of-Care Diagnostics (POC): Invest in developing smaller, faster, less complex staining/analysis platforms for use in ASCs and community settings, extending the reach of tissue diagnostics beyond the central hospital lab.

Browse More Reports:

North America Personal Care Ingredients Market

Global FinFET Technology Market

Global Paper Dyes Market

Asia-Pacific Protein Hydrolysates Market

Global Inline Metrology Market

North America Retail Analytics Market

Global Thrombosis Drug Market

Europe Network Test Lab Automation Market

Global Perinatal Infections Market

Global Light-Emitting Diode (LED) Probing and Testing Equipment Market

Global Mobile Campaign Management Platform Market

Global Fruits and Vegetables Processing Equipment Market

Global STD Diagnostics Market

Asia-Pacific Microgrid Market

Global Fluoxetine Market

Global Food Drink Packaging Market

Global Electric Enclosure Market

Asia-Pacific Artificial Turf Market

Global Hand Wash Station Market

Global Prostate Cancer Antigen 3 (PCA3) Test Market

Asia-Pacific Hydrographic Survey Equipment Market

Global Cable Testing and Certification Market

Global Leather Handbags Market

Global Post-Bariatric Hypoglycemia Treatment Market

Europe pH Sensors Market

Global Linear Low-Density Polyethylene Market

Global Ketogenic Diet Food Market

Asia-Pacific Small Molecule Sterile Injectable Drugs Market

Global Prescriptive Analytics Market

Global Viral Transport Media Market

Middle East and Africa Composite Bearings Market

About Data Bridge Market Research:

An absolute way to forecast what the future holds is to comprehend the trend today!

Data Bridge Market Research set forth itself as an unconventional and neoteric market research and consulting firm with an unparalleled level of resilience and integrated approaches. We are determined to unearth the best market opportunities and foster efficient information for your business to thrive in the market. Data Bridge endeavors to provide appropriate solutions to the complex business challenges and initiates an effortless decision-making process. Data Bridge is an aftermath of sheer wisdom and experience which was formulated and framed in the year 2015 in Pune.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email:- corporatesales@databridgemarketresearch.com