Executive Summary

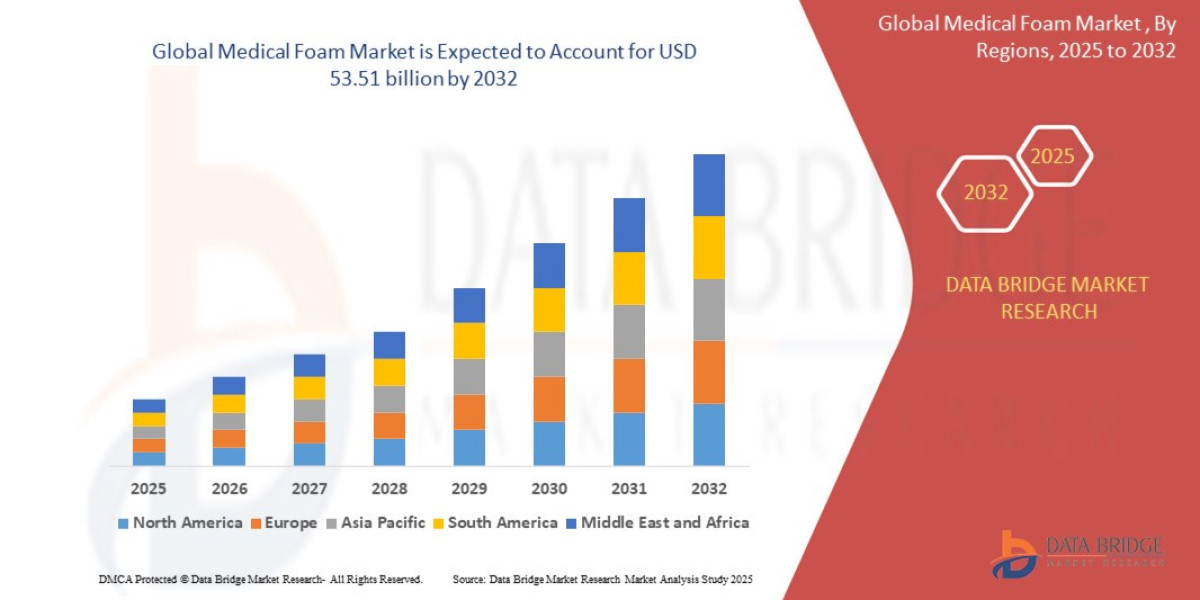

- The global medical foam market was valued at USD 32.33 Billion in 2024 and is expected to reach USD 53.51 Billion by 2032

- During the forecast period of 2025 to 2032 the market is likely to grow at a CAGR of 6.50%,

Market Overview

Definition and Scope

Medical foam refers to specialized polymeric materials, typically with an open-cell or closed-cell structure, manufactured under stringent quality and cleanliness controls (often ISO 13485 certified). These foams must exhibit essential properties, including biocompatibility, low toxicity, chemical stability, and customizable porosity/absorption rates.

Key Market Segmentation

By Material Type (Core Revenue Drivers):

Polyurethane (PU) Foam: The largest segment by volume. Used extensively in basic wound dressings, surgical sponges, and positioning pads due to its cost-effectiveness and high absorption capacity.

Silicone Foam: The fastest-growing segment by value. Preferred for advanced wound care due to its softness, superior conformity, and gentle adhesive properties, minimizing trauma upon removal.

Polyolefin Foams (e.g., Polyethylene): Primarily used in orthopedic bracing, splinting, and cushioning due to firmness and stability.

Others: Includes hydrocolloid and specialized polymer foams used in niche applications.

By Application:

Wound Care & Dressings (Dominant): Includes absorption dressings, foam wound fillers, and specialized Negative Pressure Wound Therapy (NPWT) foams.

Patient Positioning & Cushioning: Used in operating rooms, wheelchairs, and bedding to prevent pressure ulcers (bedsores).

Medical Device Components: Includes gaskets, seals, filters (e.g., in ventilators), and acoustic dampening materials in complex machinery.

Prosthetics & Orthopedics: Used in liners and interfaces for comfortable patient contact.

By End-User:

Hospitals and Clinics (Primary purchasing segment).

Ambulatory Surgical Centers (ASCs).

Home Healthcare Settings (Driving growth in simple dressings).

Market Drivers

Aging Population and Chronic Disease: The significant increase in the global geriatric population, coupled with rising incidence of diabetes, leads directly to higher rates of chronic conditions like venous ulcers, pressure ulcers, and diabetic foot ulcers, necessitating advanced foam dressings.

Adoption of Advanced Wound Care (AWC): Healthcare systems are shifting from basic gauze to AWC products (including foam dressings) to achieve better patient outcomes, faster healing times, and reduced risk of infection.

Infection Control Requirements: The demand for single-use, disposable foam products (e.g., surgical drapes, filters) is rising in hospitals to mitigate the risk of Hospital-Acquired Infections (HAIs).

Technological Advancements in Material Science: Continuous development of foams with enhanced properties, such as antimicrobial integration, controlled release of active ingredients, and superior adhesion with minimal pain.

Current Dynamics

The market is experiencing a value migration from standard, low-cost PU foams toward premium, high-efficacy silicone foam dressings. Key players are vertically integrating foam manufacturing capabilities to ensure a reliable supply of custom materials, while specialized foam converters are focusing on niche, high-regulatory-barrier segments like controlled drug-release foams.

Market Size & Forecast

- The global medical foam market was valued at USD 32.33 Billion in 2024 and is expected to reach USD 53.51 Billion by 2032

- During the forecast period of 2025 to 2032 the market is likely to grow at a CAGR of 6.50%,

For More Information visit https://www.databridgemarketresearch.com/reports/global-medical-foam-market

Key Trends & Innovations

1. The Silicone Superiority Trend

Silicone foam is rapidly dominating the advanced wound care segment. Its non-sensitizing, high-conformability, and pain-free removal characteristics make it ideal for fragile skin, particularly in elderly and pediatric populations. Manufacturers are innovating with silicone foam structures to control porosity, maximize vertical absorption, and integrate border adhesion into a single product.

2. Antimicrobial Integration

A major innovation trend involves embedding or coating medical foams with antimicrobial agents (such as silver ions, chlorhexidine, or polyhexamethylene biguanide - PHMB). This is particularly critical in chronic wound care, where bioburden control is necessary to initiate healing. This feature transforms the foam from a passive barrier to an active therapeutic device.

3. Smart Foams and Sensor Integration

Emerging research focuses on "smart" or functionalized foams that change properties or provide diagnostic feedback. Examples include:

Pressure-Sensing Foams: Materials embedded with sensors that map pressure distribution, alerting clinicians to high-risk areas for ulcer formation (critical for patient positioning).

pH-Responsive Foams: Materials that change color based on the pH level of the wound exudate, indicating infection status or healing progression.

4. Customization via 3D Printing

While not yet mainstream, 3D printing of medical-grade elastomers and foams is an emerging capability. This allows for the creation of perfectly customized cushioning and orthotics, or complex, multi-layered dressings with predefined zones of absorption and release, moving the market toward true personalized medicine accessories.

5. Drug Delivery Systems (DDS)

Foams are increasingly utilized as scaffolds for localized drug delivery. By impregnating the porous structure with active pharmaceutical ingredients (APIs)—ranging from antibiotics and analgesics to growth factors—manufacturers can create sustained, controlled-release systems applied directly to the site of action, improving compliance and therapeutic efficacy.

Competitive Landscape

The Medical Foam Market features a balanced mix of global diversified healthcare companies, specialized wound care manufacturers, and dedicated foam material science firms.

Tier 1: Diversified Healthcare Giants (Wound Care Dominance):

3M Co.: A leader in adhesive and material science, supplying foams for dressings and device components.

Smith & Nephew, Coloplast, Mölnlycke Health Care: Major players that utilize proprietary foam technology (often silicone or PU-based) as the core material for their advanced wound care product lines (e.g., ALLEVYN, Mepilex). Their strategy is driven by brand reputation and clinical efficacy data.

Tier 2: Specialized Material Producers & Converters:

Rogers Corporation, Trelleborg AB: Provide specialized, high-performance foam materials and components (gaskets, seals, acoustic foams) that are integrated into medical equipment and complex devices by OEMs (Original Equipment Manufacturers).

Sekisui Chemical Co. Ltd., Recticel NV: Core material producers who convert large volumes of polymer into medical-grade sheets and blocks.

Competitive Strategies Emphasized:

Vertical Integration: Core wound care players increasingly seek to control the entire supply chain, from raw foam polymerization to final dressing assembly, to ensure quality and cost control.

Clinical Efficacy Studies: Competition revolves around producing clinical data that proves superior outcomes (faster healing, lower pain scores) for premium foam dressings versus competitors or commodity products.

Partnerships with OEMs: Material suppliers actively partner with medical device OEMs (e.g., in diagnostics or surgical equipment) to secure long-term, high-volume contracts for custom foam components.

Regional Insights

North America (High Value and NPWT Adoption)

North America holds the largest market share by value, driven by high per-capita healthcare spending, favorable reimbursement policies for advanced wound care products (including NPWT foam kits), and the rapid adoption of premium silicone foam technology. The U.S. market sets global price and innovation trends.

Europe (Regulatory Compliance and Geriatric Demand)

Europe is a mature market with high demand, particularly due to its established geriatric population. Market dynamics are strongly influenced by national tenders and regulatory frameworks (MDR), which emphasize product safety and clinical performance. Biosynthetic and sustainable foam materials are often prioritized here.

Asia-Pacific (Infrastructure Build-out and Volume Growth)

The APAC region is the fastest-growing market globally. Growth is fueled by increasing disposable income, expanding healthcare access in countries like China and India, and the rising awareness and acceptance of advanced wound care products. This region represents a massive opportunity for PU foam volume sales and a future target for silicone foam penetration.

Challenges & Risks

1. Regulatory Hurdles for Novel Materials

Introducing new foam compositions (especially those with integrated APIs or diagnostics) faces complex and lengthy regulatory approval processes (e.g., FDA Class II/III designation) due to requirements for demonstrating biocompatibility, leaching profiles, and long-term stability.

2. Raw Material Price Volatility

The market is exposed to the price volatility of key petrochemical feedstocks used to manufacture polyurethane, silicone, and other polymers. Supply chain disruptions can significantly impact manufacturing costs and product profitability.

3. Waste Management and Sustainability

The vast majority of medical foams are single-use and disposable, contributing significantly to medical waste. There is increasing pressure from hospitals and regulators for manufacturers to develop biodegradable, sustainable, or environmentally responsible foam materials and packaging solutions.

4. Commoditization of Standard PU Foam

The polyurethane segment faces intense downward pricing pressure, particularly in basic dressings and cushioning, due to the entry of low-cost manufacturers, primarily from APAC. Manufacturers must constantly innovate to justify a premium price point.

Opportunities & Strategic Recommendations

For Manufacturers and Material Scientists

Prioritize Sustainability R&D: Invest in developing polymer formulations that are biocompatible and biodegradable or easily recyclable. Achieving a "green" medical foam product will be a major differentiator in securing large European and institutional contracts.

Focus on Drug Delivery Scaffolds: Dedicate resources to R&D of foam matrices that enable precise, controlled-release kinetics for pain management (local anesthetics) or infection treatment (antibiotics) directly into the wound bed.

Expand Component Services: For material converters, strategically target the high-growth med-tech device market (e.g., ventilators, dialysis equipment) by offering ultra-high-performance specialty foams for filtering, sealing, and acoustic management.

For Investors and Private Equity

Target Silicone & Specialty Converters: Invest in companies that specialize exclusively in converting high-grade silicone and advanced polymeric foams, as they capture the highest value-add in the supply chain and are less exposed to PU commoditization.

Focus on Chronic Wound Management: Back firms whose foam product portfolios are heavily weighted toward managing complex, chronic wounds (e.g., diabetic ulcers), a segment with inelastic demand and high reimbursement rates.

Acquire NPWT Suppliers: Seek acquisition targets that provide proprietary foam components specifically for Negative Pressure Wound Therapy systems, capitalizing on the high utilization rates of this therapeutic modality in hospitals and ASCs.

Browse More Reports:

Global Transcritical CO2 Systems Market

Asia-Pacific Bio Preservation Market

Global Orthopedic Navigation Systems Market

Europe Electric Enclosure Market

Middle East and Africa Sludge Treatment Chemicals Market

Global Antimicrobial Drugs Market

Global Ballistic Composites Market

Global IoT Gateways Market

Global Mini Truck Market

Global Sustainable Toys Market

Global Empty Capsules Market

Global All Wheel Drive (AWD) Systems Market

Global Unmanned Ground Vehicle Market

Global Green Tea Market

Global Panniculitis Market

Asia-Pacific pH sensors Market

Global Facial Tracking Solutions Market

Global Skid Steer Loaders For Construction Market

Global Geographic Information System (GIS) Software Market

Asia-Pacific Plastic Compounding Market

Asia-Pacific Data Integration Market

Middle East and Africa Infection Surveillance Solution Systems Market

Global Candy Coated Chocolate Market

Global Water-Based High-Performance Coatings Market

Global Abscisic Acid (ABA) Market

Global Flake Ice Machine Market

Global Text-To-Speech Market

Middle East and Africa Acute Lymphocytic/Lymphoblastic Leukemia (ALL) Diagnostics Market

Global Toaster Market

Global Haematococcus Market

Global Bio-Based Hot Melt Adhesive (HMA) Market

About Data Bridge Market Research:

An absolute way to forecast what the future holds is to comprehend the trend today!

Data Bridge Market Research set forth itself as an unconventional and neoteric market research and consulting firm with an unparalleled level of resilience and integrated approaches. We are determined to unearth the best market opportunities and foster efficient information for your business to thrive in the market. Data Bridge endeavors to provide appropriate solutions to the complex business challenges and initiates an effortless decision-making process. Data Bridge is an aftermath of sheer wisdom and experience which was formulated and framed in the year 2015 in Pune.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email:- corporatesales@databridgemarketresearch.com